Image Source: Unsplash

It is wildly unpopular to say this, but Canadian home prices need to move much lower. And yes, I, too, stand to lose net worth as they do.

Immigration is unlikely to prevent mean reversion here. Immigrants need places to live, to be sure, but historically, it took an average of 7 years before immigrants were able to buy a home in Canada. And that was when prices were more affordable than today.

At the moment, home affordability is at its worst since mortgage rates were north of 18% in 1981. The driver of unaffordability today is not interest rates (historically average); today, unaffordability is driven by prices being impossible multiples of household income (i.e., 5 to 12 times the average household income versus long-term norms of 2 to 4x).

Where I live, one hour north of Toronto, new listings are up about 66% since the end of February. Properties are sitting on the market, and would-be sellers are still asking prices paid when mortgage rates were under two percent compared to the 5% range today.

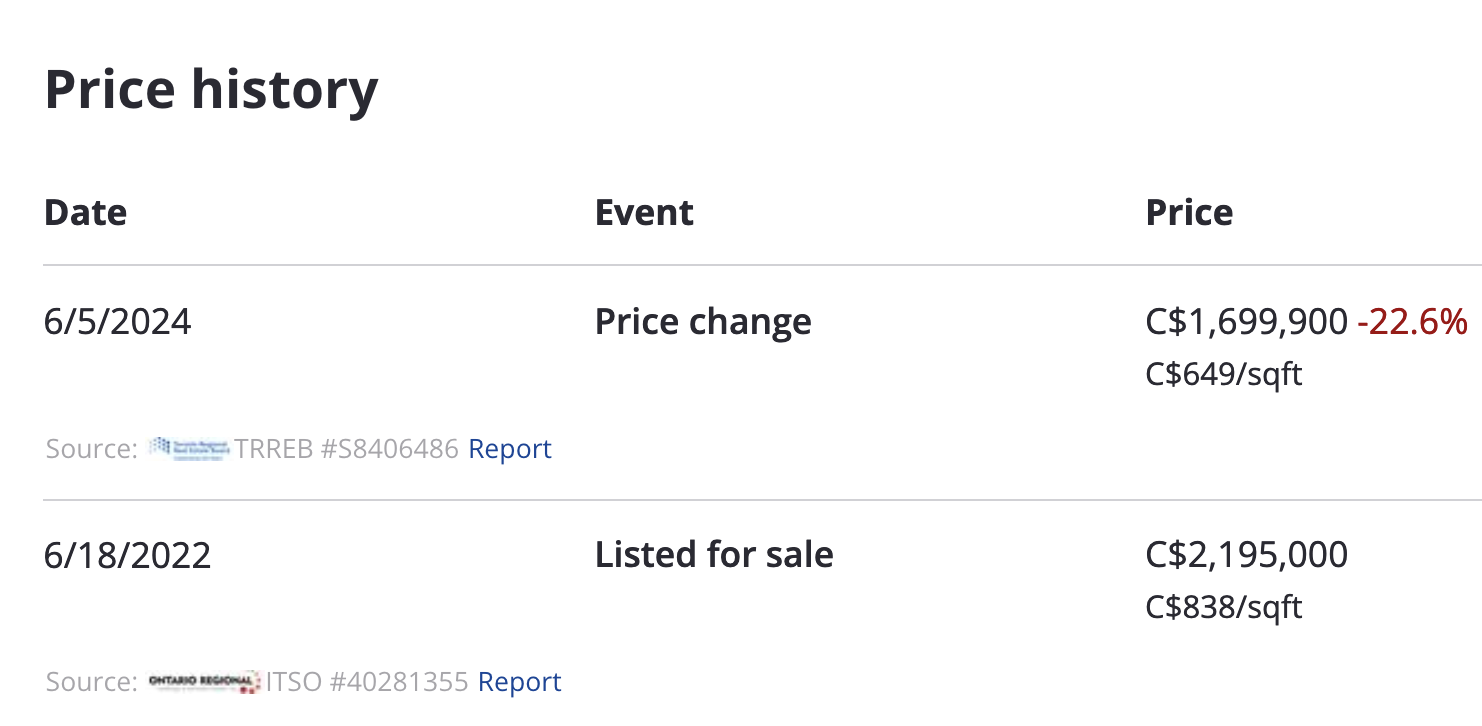

Recently, “reduced” and “new price” listings have been popping up. This lovely custom home on my walking circuit in a premium area across from the lake was built on spec during the pandemic. So far, as shown below, the price has been reduced by 22% to $1.69m from $2.195m two years ago.

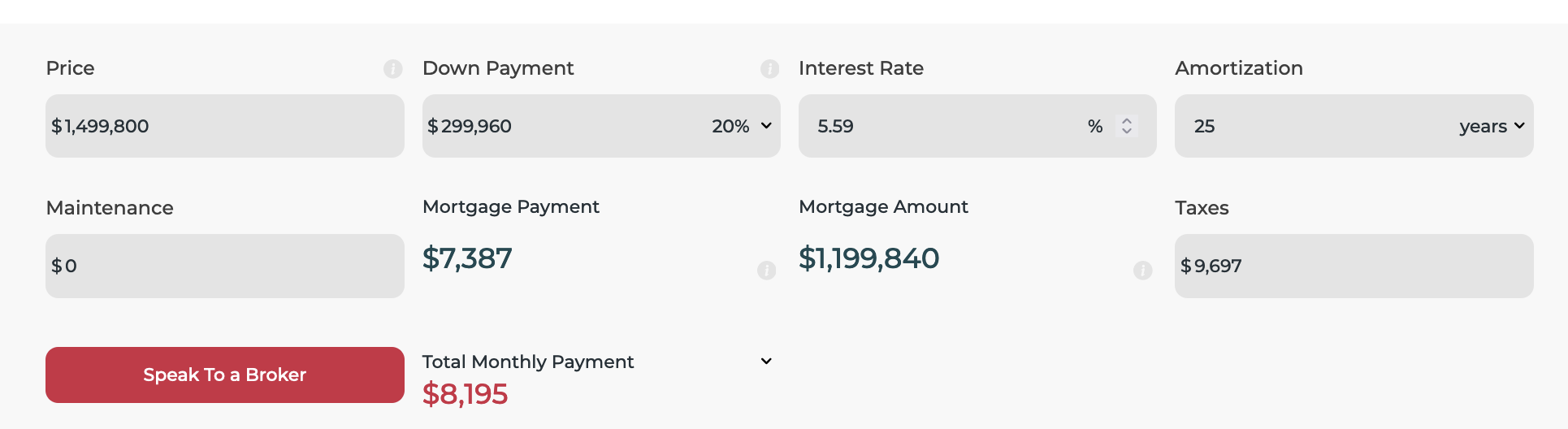

A vacant lot around the corner has been marked down 58% to an ask of $495K from $1.195m three years ago (see listing history here). This lovely home in the same neighbourhood sold for $1.8m in February 2022 and is now listed 17% lower at $1.49m after months on the market (see price history here).

The trouble is that even at the $1.49m asking price, with a 20% (299k) downpayment, the mortgage payment would be $7,387 a month, $8,195 a month, including property taxes. That requires $98,340 a year in after-tax income to cover the mortgage and property taxes (as shown below), let alone all life’s other expenses.

(Click on image to enlarge)

Less than 10% of Canadian households earn more than $100k a year before tax, never mind after (see Is a $100k salary enough for a comfortable life anymore?).

The reality is that most homeowners today would be hard-pressed to qualify for a conventional mortgage at current asking prices and interest rates to buy their current homes.

Yes, the Bank of Canada has started easing base rates in the banking system and is likely to respond to a weak economy and rising unemployment with more cuts in the months ahead. But that’s not all that’s needed here.

More By This Author:

Eyes Wide Open As Bank Of Canada Blinks

Easing Begins As Unemployment Rises

Buying High And Selling Low, Rinse And Repeat

Comments

Log in or sign up to join the conversation.