The most recent quarter may be as good as it gets for Canadian banks, after five Bank of Canada rate hikes since mid-2017. Following a surge in late summer of 2018, Canadian bank stocks stumbled badly in December and then bounced back starting the new year (Figure 1). However, the Bank of Canada has signaled that it is “highly uncertain” with it comes to the path of future rate hikes. Recent economic data confirm that the economy is not expanding sufficiently to warrant continuing rate increases, and many economists are calling for a policy reversal of one or more rate cuts to ward off a recession.

(Click on image to enlarge)

Figure 1 TSX Canadian Bank Index

At the completion of the first quarter, Canadian bank CEOs, in their year-end addresses, voiced concern about the remainder of the year. The Toronto-Dominion Bank warned that “growth will be constrained” for the balance of 2019. Canadian mortgage growth will be flat or in the low single digits for the “foreseeable future,” according to the CIBC which is the largest mortgage lender in the country. The bank’s CEO did not rule out the possibility that mortgage growth could turn negative should home sales continue to fall in the large metropolitan areas. BMO expects Canada’s economy to grow at a moderate pace this year of around 1.5 %, below what is considered its potential. Bank analysts are starting to refer to the end of the credit cycle and are cautioning clients to expect greater loan loss provisions, particularly in the housing sector and energy sectors.

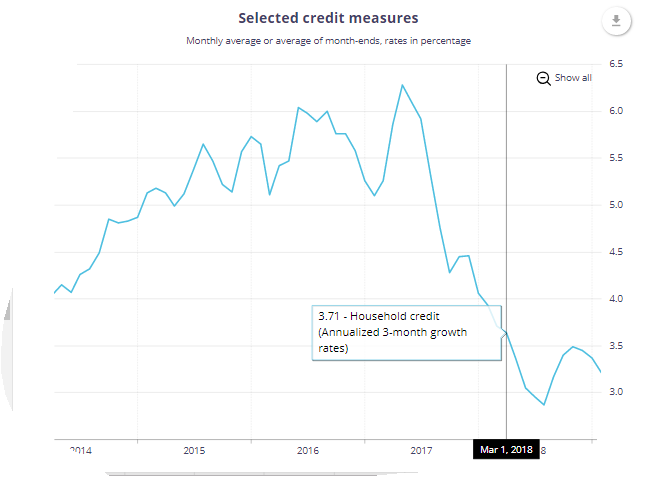

(Click on image to enlarge)

Figure 2 Household Credit

Figure 2 confirms that bank lending to household has slowed dramatically. During 2016-17 credit expanded at6% only to drop down to just over 3% in the latter part of 2018, less than the nominal rate of GDP growth (Figure 2). This restrain on credit could be a self-fulfilling prophecy as banks deny loan requests, causing the economy to weaken even further, giving them more reason to curtail lending.

Canadian investors have long been in love with their banks. Over the long haul, stock values have grown, dividend growth has been solid and investors have drawn comfort from an industry that is competently regulated.

However, not is all well in the Canadian economy. Loan losses are starting to appear in the oil sector as exports and prices remain weak. As mentioned earlier, homes sales are sagging, retail sales have been underwhelming and business capital expenditures have also disappointed. Internationally, Canada continues to run a trade deficit and the United States trade tariffs on steel and aluminum remain in effect. Recent decisions by the Chinese to forego some Canadian oil exports and selective agricultural products have added to the trade woes.

Finally, the banks are facing challenges from the rise in fintech as new technologies cut into the cost of banking services. In the mortgage sector, although the banks dominate the industry, alternative near- bank and non-bank lenders are gaining market share.

Comments

Log in or sign up to join the conversation.