Canada’s Stringent Stress Test Rules Slowed Residential Mortgage Growth And Also Reduced Some Of The Risks In The Financial Sector

“Since mid-2016, provincial governments, the Office of the Superintendent of Financial Institutions, and the Bank of Canada have successively intervened to slow housing demand with interest rate hikes, mortgage borrower stress tests, and taxes on purchases by foreign non-residents. British Columbia and Ontario have also passed supply-side measures, including taxes on vacant apartment homes and reduced restrictions on urban construction.” (Moody’s Analytics, October 2018)

“Let’s say since interest rates are rising, you’re planning to choose a five-year fixed rate mortgage. Under the old mortgage rules (Pre-Jan. 2018), you’d only have to qualify at your mortgage rate at your lender. So, if your mortgage rate is 3.15 percent, then that’s the rate you’d qualify at. Simple enough. However, under the new mortgage stress test rules, you must pass a more onerous stress test. Now you’ll need to pass a higher hurdle: the greater of your mortgage rate plus two percentage points and the Bank of Canada’s five-year benchmark rate. In the above example, if the Bank of Canada’s five-year benchmark rate is 4.99 percent, then you’d have to qualify at 5.15 percent, since it’s the higher of the two.” (Mortgage pay Web Site, What the B-20 Mortgage Stress Test Means for Home Buyers)

Canada’s stress test rules were introduced by the Federal Government (and were also encouraged by the Bank of Canada) because of the concern that Canadians had accumulated too much debt in the long period of unusually low interest rates. The public policy concern particularly centred on too much mortgage debt.

Related Partner Article: Chinese Real Estate Investors in Canada: Is Their Ownership Now Less than 4%?

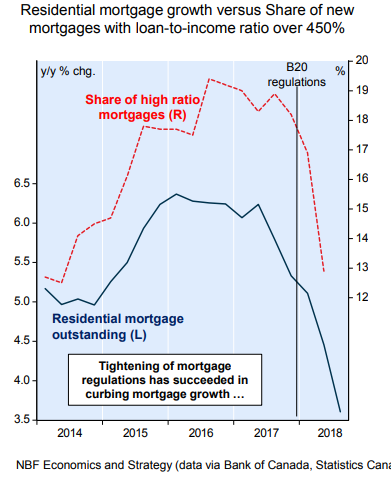

At the start of 2017, the Canadian government introduced its B-20 mortgage regulations which were designed to reduce housing demand and deflate housing prices which were soaring in many urban centers of the country.

As the second quotation indicates, the B-20 rules forced lending institutions to ensure that the borrower could handle higher mortgage rates when they arrive. The new condition required Canadian purchasers of real estate to qualify for a loan at a mortgage rate two percentage points higher than the market. This new qualifier is quite onerous, and not surprisingly, this has cut into Canadian mortgage demand.

As the following chart illustrates, the tougher regulations have succeeded in lowering the percentage share of high ratio mortgages (i.e. those with a loan-to-income ratio of over 450%).

Not surprisingly, the relative reduction of risky mortgages in the financial system has come at the expense of overall slower mortgage growth.

CMHC data also indicate that the share of mortgage borrowers with high credit scores has increased from an average of 65% between 2002 and 2008 to 88% as of the third quarter of 2018. According to Statistics Canada, residential mortgage loan growth fell to a 3.6% year-on-year pace in the third quarter of 2018, the slowest mortgage growth rate since 2001.

At the same time, the number of borrowers with lower credit quality has also declined.

In closing Canada’s new mortgage credit and accessibility rules not only slowed the growth of mortgage credit but also deflated resale home prices. The latter effect was also widely expected.

Comments

Log in or sign up to join the conversation.