The Canadian banks chalked up significant profits last quarter, as the accountants decided to re-instate provisions for loan losses taken in prior quarters. Approximately half of the increase in the bank profits is accounted for by reversing these earlier accounting charges. Banks have traditionally used this accounting technique as standard business practices as they try to judge the impact of future economic conditions on their customers. It is especially challenging to make those decisions as the coronavirus ripped through the world economy. But it is clear that the Canadian banks are, indeed, in good shape.

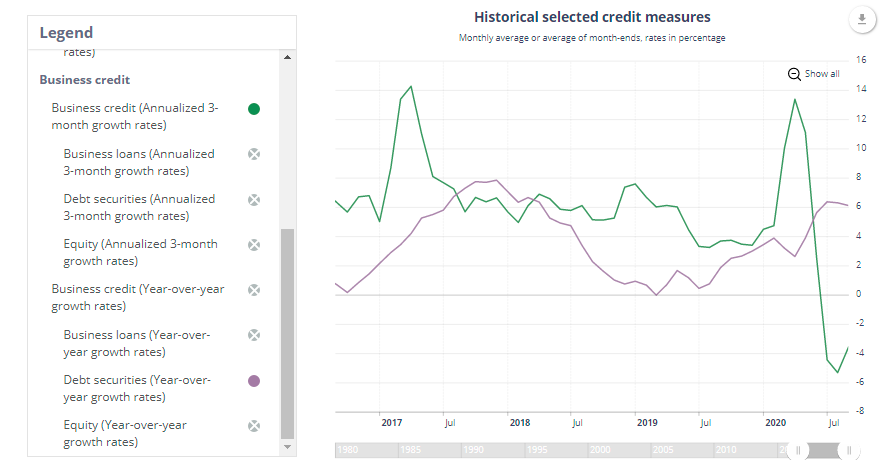

Commenting on his bank’s most recent profit performance, CIBC ‘s CEO, Victor Dodig stated that ‘a healthy banking system helps the economy grow.’ A heathy recovery must include the business sector which relies on capital to expand operations and hire employees. Using that measure the Canadian economic recovery is very far from a return to good health. Rather, it is mired in a business investment recession that will have long term consequences. The COVID-19-induced recession has resulted in thousands of businesses shuttering and 900,000 fewer Canadians in full-time work compared to the months prior to the pandemic restrictions. That is a heavy toll to bear. To rebuild, businesses need bank loans. Just prior to the onset of the pandemic’s shutdown, Canadian business loans were expanding at a very robust rate. By the spring of 2020, bank loans plunged at record rates (Figure 1).

Figure 1 Canadian Business Credit Conditions

(Click on image to enlarge)

The fact that business credit conditions are very poor means that Canada cannot expect any real economic expansion over the medium term. Banks are reluctant to extend business credit in the wake of new evidence that the COVID-19 virus and its variants continue to impede business expansion. For their part, business owners face too uncertainties affecting profitability. The business credit market is in a state of limbo, putting off decisions and operating on a day-to-day basis.

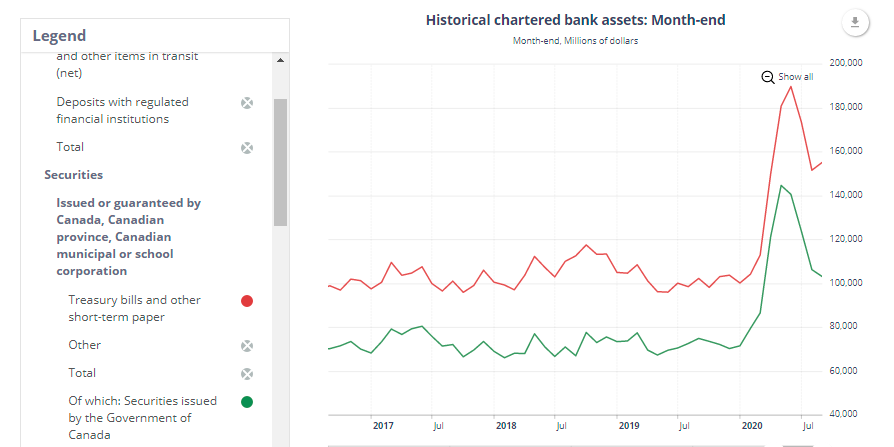

Nonetheless, the Big Six banks have received a huge influx of deposits from both individuals and businesses. The banks have chosen to invest significantly in Canadian federal government debt, starting in early 2020 (Figure 2). A similar situation exists in the US where banks have been purchasing record levels of government debt. (US Banks bulk on Treasuries)

Figure 2 Commercial Bank Holdings of Canadian Govt Debt

(Click on image to enlarge)

For the banks, the government bonds returns are meager, hampering profit growth. Banks are supposed to make loans, not buy government debt to the extent they have so far. So, the banks are healthy, in large measure because they chose to place their excess capital in the safest asset class known. However, the economy and, in particular, the business sector remain far from healthy.

Comments

Log in or sign up to join the conversation.