Image Source: Pixabay

Next week's data calendar features a couple of central bank meetings and the Reserve Bank of Australia minutes.

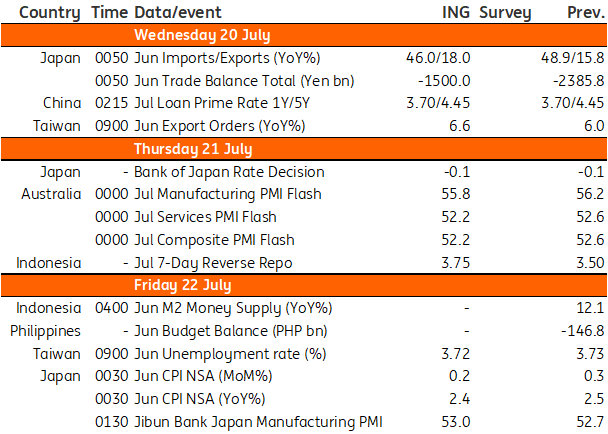

A Bank of Japan pause, a Bank Indonesia surprise, and China’s loan prime rate

The coming week features a relatively light data calendar but we do have some developments on the central bank front. Given the recent pick-up in Covid cases and weaker-than-expected consumption recovery, we expect the Bank of Japan (BoJ) to stand pat at its meeting on 21 July. The BoJ will likely pay more attention to downside risks to growth as inflation remains subdued.

Bank Indonesia (BI) holds a policy meeting next week and we believe we could see a surprise from Governor Perry Warjiyo. Previously, Warjiyo had preached patience in hiking rates, tagging subdued core inflation as a reason to keep rates at 3.5%. Recent developments, however, could convince BI to finally whip out a rate hike with US inflation surging and regional central banks resorting to off-cycle rate tightening in the past few days. Thus we believe BI can move to hike rates by a modest 25bp to help provide additional support for the Indonesian rupiah in the near term.

Lastly, banks in China will announce the 1-Year and 5-Year Loan Prime Rate this coming Wednesday. We expect there would be no change to these rates as loan growth picked up strongly in June, suggesting that the current interest rate level is sufficient to keep loan growth healthy.

Reserve Bank Australia minutes

The Reserve Bank of Australia (RBA) hiked rates by 50bp on 5 July, and the minutes from that meeting may give us some insight into whether we get a 75bp or bigger hike at the August and September meetings. Much will doubtless rest on two data points over the coming months. The first will be the second quarter CPI release on 27 July, shortly before the 2 August RBA meeting. And then the second quarter wage price index on 17 August, ahead of the 6 September RBA meeting.

Other important releases: Taiwan export orders

Not much else is on the data calendar for next week but we note that Taiwan will be releasing data on export orders. Export orders out from Taiwan could show slightly faster growth as consumer demand has begun to recover in Mainland China post-lockdowns.

Asia Economic Calendar

Image Source: Refinitiv, ING

More By This Author:

FX Daily: The 100bp Narrative Is On

Canada Goes All In With 100bp Hike

China’s Import Growth Lagged Behind Exports For A Good Reason

Comments

Log in or sign up to join the conversation.