Concerns about the depth and breadth of price pressures in an economy experiencing significant excess demand has prompted the Bank of Canada to "front load" with a 100bp rate hike. The evident concern at the BoC implies upside risk to our forecast of a further 125bp of rate hikes before the end of the year.

The Bank of Canada hiked rates by 100bp in July with more expected by year-end

Surprise 100bp hike puts pressure on the Fed to follow suit

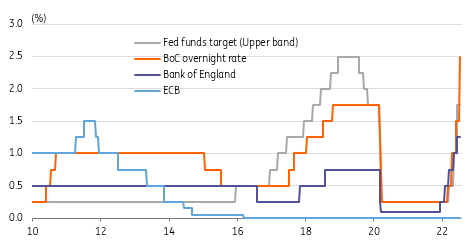

A surprise 100bp move from the Bank of Canada versus the 75bp hike expected. This takes the policy rate up to 2.5%, matching the New Zealand official cash rate after the RBNZ hiked 50bp overnight. It will put the pressure on the US Federal Reserve to follow suit, but for now we stick with our 75bp call for July 27th. Canada's economy is arguably in a firmer position given the jobs market is even stronger than the US' (employment well above pre-Covid peak) and the commodity exposure suggests more resilience in the current economic environment than the US where recession fears are clearly on the rise.

Central Bank policy rates

Source: Macrobond, ING

Front loading, but with much more to come

The BoC statement highlights the breadth of price pressure, commenting that "more than half of the components that make up the CPI are now rising by more than 5%" and the surge in inflation expectations, "more consumers and businesses are expecting inflation to be higher for longer". The fear is this becomes embedded which "If that occurs, the economic cost of restoring price stability will be higher".

They also cite "further excess demand" having been built up in the economy, but have cut their growth forecasts for next year due to tighter monetary policy. They have described today’s action as a "front load" move, which implies this is a one-off aggressive hike, but indicate that "interest rates will need to rise further" with the central bank "resolute in its commitment to price stability".

We are currently forecasting 50bp hikes in September and October with a 25bp move in December. This would take the policy rate up to 3.75% by year-end, but the odds are certainly moving towards a more aggressive move in September at the very least, especially if inflation shows little sign of abating.

More By This Author:

China’s Import Growth Lagged Behind Exports For A Good Reason

Eurozone Industrial Production Ticks Up In May But Outlook Remains Bleak

FX Daily: 75bp Is The New Normal

Comments

Log in or sign up to join the conversation.