Image Source: Unsplash

The coming week features growth and inflation readings for the region, plus a first look at China's PMI for the year.

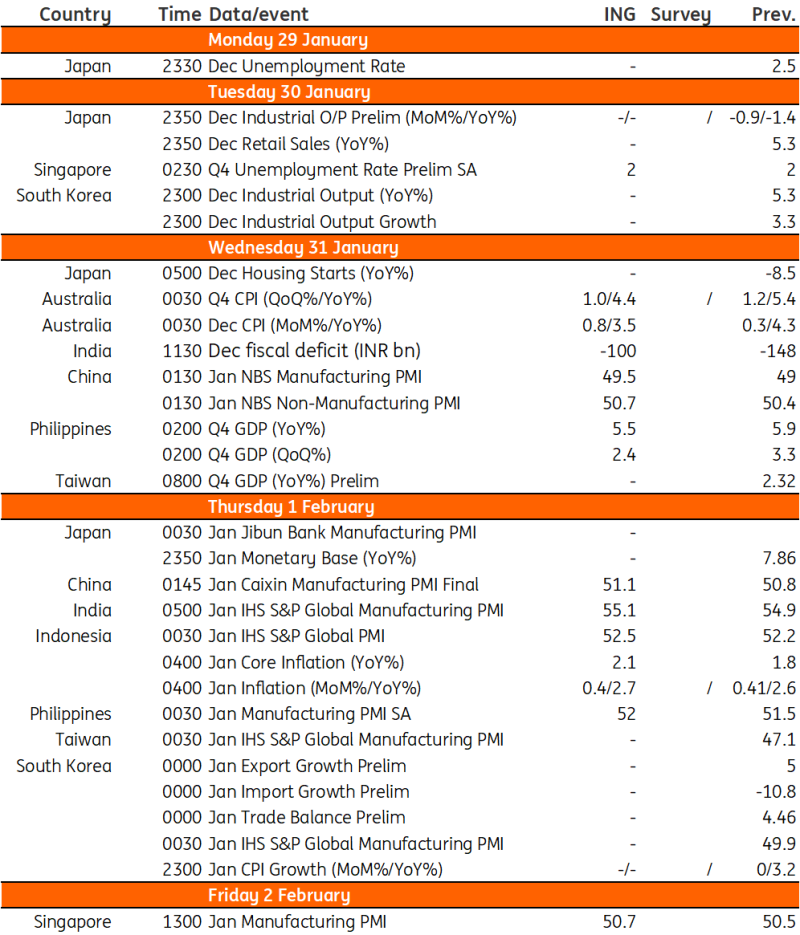

Australia inflation out next week

Australia's CPI inflation figure for the fourth quarter of last year is due for release – and more importantly, the December number, which will drive the quarterly result. Last year, cold, wet weather pushed up the prices of fresh food as well as energy (shortage of LNG and coal as mines were flooded) and collided with the re-opening surge in demand for tourism which caused recreation prices to spike higher. The net result of this was a 1.6% month-on-month increase in the CPI index and an inflation rate of 8.4%.

This December will also see holiday prices and recreation spike higher (as is normal for the time of year) but probably not to the same degree as last year. So, we expect the CPI increase to come in at about 0.8% MoM, which would take the inflation rate all the way down from 4.3% to only 3.5% year-on-year, within spitting distance of the RBA’s 2-3% target. That’s all very well, but the run rate for Australian monthly CPI is still way too high to take inflation meaningfully lower in the medium term. We will need to see this slow markedly over the first half of the year if rate cut expectations are not to turn sour.

India's fiscal deficit likely on track to achieve the target

India’s fiscal deficit for December is due and since August, a combination of solid growth and buoyant revenue plus fiscal discipline has led to much lower deficit figures than the corresponding months a year earlier.

The relevant comparison for December 2023 is December 2022’s INR148.22bn deficit. Anything around this sort of level or better would leave India well on track to achieve its deficit target for 2023/24 of 5.9% GDP equivalent.

China's PMIs could trend slightly higher by to start of 2024

The National Bureau of Statistics of China will release its January PMI data next week, which will provide the first key data point for indicating how the country's economy has started off the year. The manufacturing PMI has been in contraction for eight of the past nine months. By sub-index, production has been the bright spot recently, remaining in expansion for the past seven months.

New orders have been sluggish, contracting throughout the fourth quarter of 2023. Employment and inventories have both been in contraction even longer, below 50 for 10 consecutive months. For the January 2024 data, we expect the manufacturing PMI to edge up to 49.5 to start the year, remaining below the 50 threshold but implying a smaller contraction.

Taiwan's 4Q GDP expected to come in at 3.6% YoY

Taiwan’s 2023 fourth quarter GDP is expected to rise to 3.6% YoY, which would mark the third consecutive quarter of higher YoY growth. Both private consumption and government spending are expected to be drivers of fourth quarter growth.

The contribution from net exports likely improved, as exports saw weak YoY growth and imports continued to see double digit declines through October to November 2023. In contrast, gross fixed capital formation is expected to remain a drag on the GDP numbers due to an unfavorable base effect.

Hong Kong 4Q GDP to accelerate

We expect Hong Kong's fourth quarter GDP data release to confirm further recovery in the economy, with fourth quarter growth rising 4.9% YoY and taking annual growth to 3.4% YoY. Though the high yearly growth is bolstered by a favorable base effect, monthly economic data including retail sales and the private sector PMI also indicate a sequential recovery. Heading into 2024, with the base effect normalizing, we are likely to lead to more muted YoY growth.

Private consumption expenditure and gross domestic fixed capital formation are expected to remain the main contributors to fourth quarter GDP, while a recovery of exports in October and November should signal a moderate uptick in the net exports component as well.

Japan releases industrial production and jobs report

Japan’s industrial production has been quite soft over the past months, possibly related to temporary production interruptions by car manufacturers. However, we expect to see a nice rebound from December on the back of solid output gains in vehicles and machinery, suggested by stronger-than-expected December exports outcomes.

Meanwhile, labor market conditions should remain tight, supported by the service sector. Healthy labor conditions will likely support the modest growth of retail sales.

Korea's trade, inflation, and industrial production

Korea's exports are expected to jump sharply to 16.5% YoY in January (vs 5.0% in December), exaggerated by favorable calendar effects. The Lunar New Year celebration fell into January last year, it should therefore distort the headline outcomes for a couple of months. Aside from more working day effects, January exports are expected to improve on the back of semiconductor recovery and inventory restocking for vehicles. Meanwhile, imports should decline even faster, reflecting falling commodity prices and weak domestic demand. We expect manufacturing PMI to rebound in January, led mainly by solid external demand.

January headline inflation should slow down quite sharply to 2.6% YoY (vs 3.2% in December) but mainly due to a higher year-earlier base in utility fees. The Bank of Korea may be concerned about potential price hikes when government subsidy programs end in March, and no rate hike is expected at the February meeting as a result. December IP will not be particularly market-moving as fourth quarter GDP data for 2023 has already been released. We expect manufacturing industrial production to rise for a second month but at a slower place. Robust gains in semiconductors should continue, but vehicle outputs are expected to decline. Sluggish retail sales and construction investment must also have dragged down overall growth.

Philippines 4Q growth could hit 5.5%

Philippine fourth quarter GDP should expand by 5.5% YoY, with growth fueled by robust household consumption and accompanied by a healthy dose of government expenditure. We are, however, expecting capital formation to stay subdued given elevated borrowing costs, while a stark widening of the trade deficit should result in net exports turning negative.

This should bring full year 2023 growth to 5.5% YoY, which is decent but unfortunately below the government's official target of 6-7%. With growth slipping below the government’s target, we believe the central bank will refrain from tightening policy rates further – although Governor Eli Remolona has reiterated his preference to maintain his current hawkish stance for now.

Indonesia's inflation likely settled at 2.7%

Price pressures in Indonesia remain relatively subdued, with January headline inflation likely at 2.7% YoY. This is within Bank Indonesia’s 2024 inflation target of 1.5-3.5%. Even so, Governor Perry Warjiyo remains wary of a potential flare up in price pressures to start the year. He may particularly be worried about potential food price spikes due to El Nino, and he has indicated BI will likely not cut policy rates until the second half of the year.

Key events in Asia next week

More By This Author:

US GDP Confounds Slowdown Fears, But ‘Job Done’ On Inflation

The Commodities Feed: Gold Trades Softer On Lower Rate Cut Expectations

FX Daily: Fed Cancels The Free Lunch

Comments

Log in or sign up to join the conversation.