Fourth-quarter 2023 GDP growth beat all expectations thanks to strong consumer and government spending plus a positive contribution from net trade. First-quarter GDP growth is expected to be weaker based on business surveys, but the Fed is close to declaring victory on inflation with the second consecutive 2% quarterly core inflation reading.

3.3% 4Q annualised GDP growth

GDP beats all expectations

US fourth-quarter GDP growth came in at 3.3% quarter-on-quarter annualised, well above the 2% consensus and above every forecast in the Bloomberg survey. The personal consolation is that at least we were closest (ING predicted 2.5%). The details show consumer spending was very strong, rising 2.8% while government spending increased 3.3% and non-residential fixed investment increased 1.9% with residential investment up 1.1%. Inventories added 0.07 percentage points to growth while net exports added 0.43pp.

This means the economy grew 2.5% for the full year of 2023, confounding expectations at the beginning of last year that tighter monetary policy and credit conditions would potentially lead the economy to fall into recession. That said, a great number today makes it more likely that first-quarter 2024 GDP will be weaker. Inventories are going to be making a negative contribution and trade is likely to also swing back to becoming a headwind while consumer momentum is also slowing somewhat. Investment also looks set to remain subdued based on business surveys. Early days, but we are pencilling in a 1-1.5% figure for the first quarter – the current consensus is for GDP growth of just 0.6%.

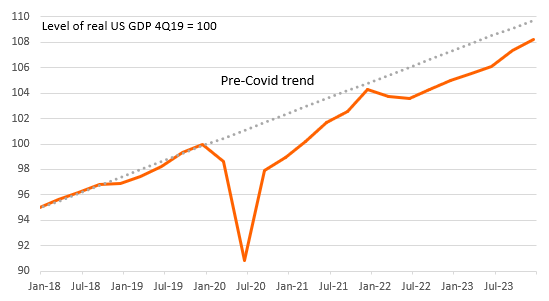

US real GDP level versus pre-Covid trend

(Click on image to enlarge)

Source: Macrobond, ING

But Job done on inflation

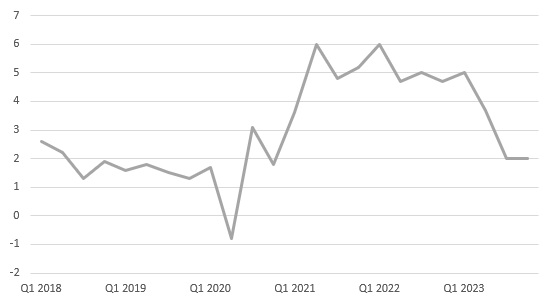

Just to mention that we have confirmation of 'job done' on inflation. The Fed's favoured measure of inflation – the core personal consumer expenditure deflator – has come in at 2% annualised for the second quarter in a row. Tomorrow's monthly data will also likely confirm that the MoM increase has come in below the key 0.17% MoM threshold for the sixth month in seven – that's the run rate we need to hit over 12 months to get us to 2% year-on-year.

As such the Fed now has huge scope to cut rates. We just think the Fed will wait a little longer to make sure it is really, really confident it can afford to cut – we expect the first move in May with 150bp of cuts this year. Neutral rates as described by the Fed are 2.5%, suggesting scope for 300bp of rate cuts to merely return us to 'neutral'. For the bond bulls who fear a bumpier, weaker outlook for the economy over the next couple of years, it could be even greater.

Core personal consumer expenditure deflator (QoQ% annualised)

(Click on image to enlarge)

Source: Macrobond, ING

More By This Author:

The Commodities Feed: Gold Trades Softer On Lower Rate Cut Expectations

FX Daily: Fed Cancels The Free Lunch

Asia Morning Bites For Thursday, January 25

Comments

Log in or sign up to join the conversation.