Image Source: Unsplash

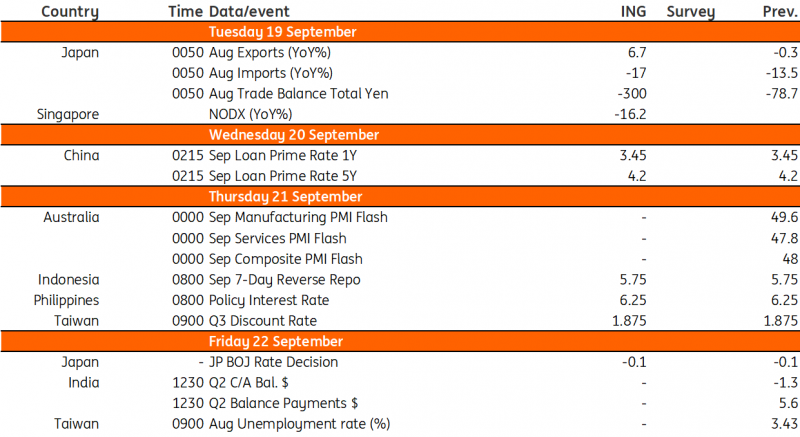

Central banks in Indonesia, Japan, the Philippines, and Taiwan will hold their respective policy meetings next week. China will also be announcing its 1-year and 5-year LPR rates.

China's 1-year and 5-year LPR rates are likely to remain unchanged

China will decide on one and five-year loan prime (LPR) rates next week. Given the current challenges, with the People's Bank of China helping to support the Chinese yuan, it is unlikely the central bank will announce any further rate cuts. We are expecting rates to remain unchanged.

Regional central banks to stand pat

The Central Bank of the Republic of China (CBC), Bank Indonesia (BI), and Bangko Sentral ng Pilipinas (BSP) are all expected to retain current policy settings in line with the US Federal Reserve.

For Taiwan, as inflation turned up recently and with the New Taiwan dollar being quite soft, we are expecting it to hold the rate steady.

Similarly, BI will likely hold rates steady to support the Indonesian rupiah, which is down 0.78% for the month.

Lastly, the BSP will also likely stand pat as inflation pressures flare up, with the latest inflation reading surging to 5.3% year-on-year.

Inflation and trade figures for Japan next week

We expect headline consumer inflation to slow to 3.1% YoY in August (vs 3.3% in July) with the ongoing energy subsidy program, however, core inflation excluding fresh food and energy will likely edge up slightly to 4.4% (vs 4.3% in July), which will be a major concern for the Bank of Japan (BoJ).

For the trade report, we expect exports in August to rebound from the recent dip, with strong auto shipments while imports could decline more sharply to -18% YoY compared to the previous month as base effects dominate the rise in commodity prices and weak Japanese yen.

Meanwhile, the BoJ is likely to stay pat next week. The central bank could however probably send a subtle hawkish message to the market after higher-than-expected inflation and a weak JPY, combined with rising global oil prices, pushed inflation up further.

Key events in Asia next week

Image Source: Refinitiv, ING

More By This Author:

FX Daily: A Dovish Hike Ahead Of A Hawkish Hold

Rates Spark: Transitioning From Level To Duration

Asia Morning Bites - Friday, Sept.15

Comments

Log in or sign up to join the conversation.