Asia Open: Walking On Eggshells

Image Source: Unsplash

MARKETS

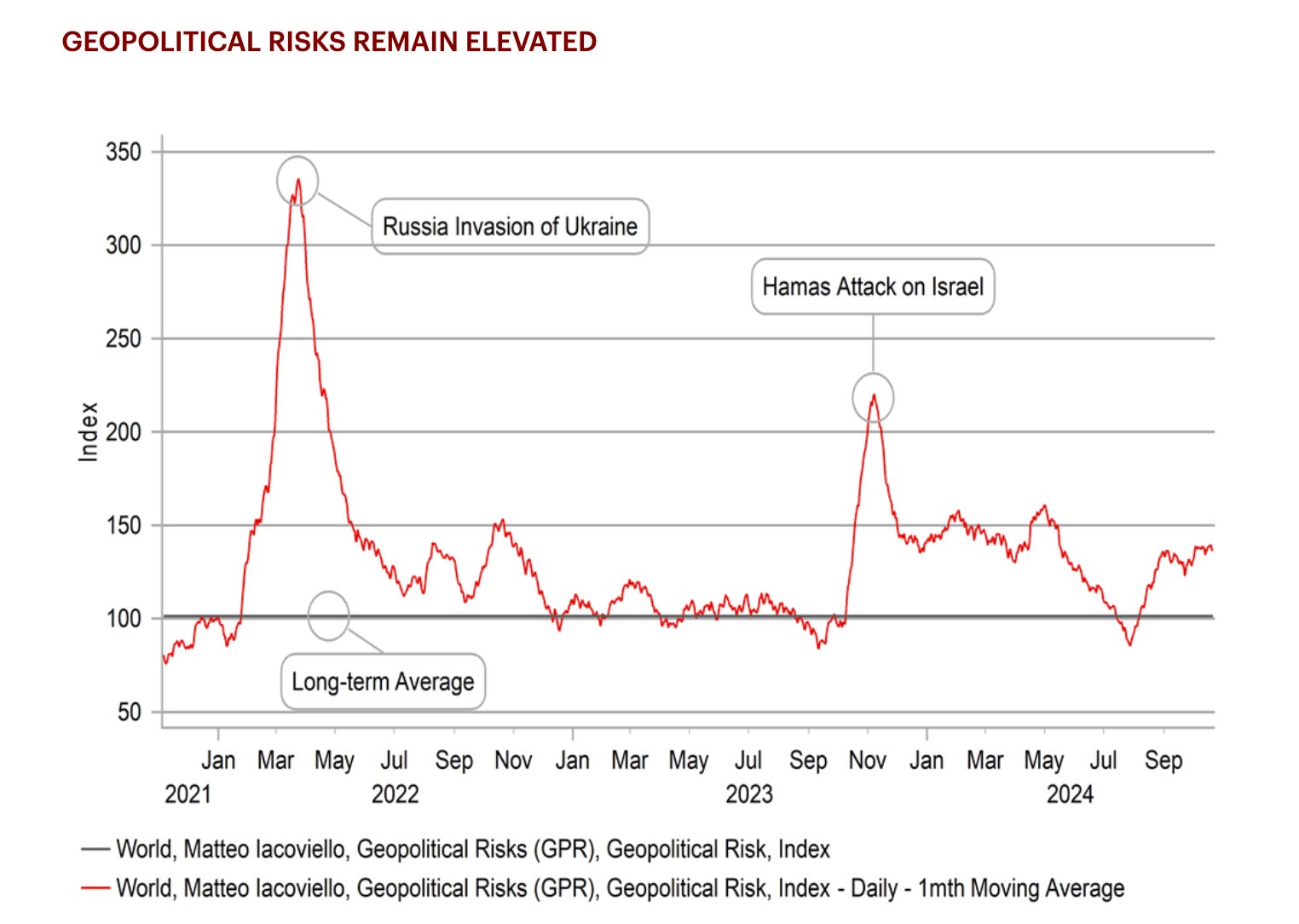

Stocks got a lift Monday as Middle East tensions simmered down. Israel’s weekend response to Iran, limited to a handful of military targets, managed to sidestep oil infrastructure and civilian sites, helping dial back the recent geopolitical risk premium. Oil’s 6% drop might have had bond traders dancing in their seats, but stocks rallying alongside high U.S. yields is as unpredictable as thunder on a sunny day. Something’s got to give—either Treasury bears or equity bulls will have to back off soon, but the catalyst is anyone’s guess.

One thing’s for sure: bond yields show no sign of cooling. Ten-year yields touched 4.30% Monday, marking a 64-basis-point climb since the Fed’s September rate cut. Who said yields were supposed to fall in a cutting cycle? The looming November 5 election might be the wildcard that could throw a wrench into rate projections in 2025.

Across the globe, Asia is walking on eggshells. Markets are wobbling as political drama in Japan continues after the ruling coalition’s weak election performance, leaving the yen softer and Tokyo stocks on shaky ground. Meanwhile, China is banking on fresh liquidity injections from the PBoC, but any real calm likely won’t set in until after the U.S. election. If Trump returns with a 60% tariff on Chinese imports, Beijing could be backed into a corner, choosing between yuan devaluation or hefty fiscal stimulus—both loaded with risks.

A yuan devaluation would be a ticking time bomb, especially for Asia’s emerging markets. With the dollar already on its strongest run since April 2022, further dollar strength could hammer local currency debt, destabilizing regional economies. And over in bond land, traders keep inching Fed cut expectations down, pricing in a hefty inflation bounce no matter who takes the Oval Office.

The rally in U.S. stocks could hit a few derisking speed bumps as we head into a series of high-stakes events, including blockbuster tech earnings, a much-anticipated jobs report, and—cue the drumroll—the roaring U.S. elections all colliding, just as the Fed enters a quiet period before the November FOMC. If the Fed is holding back on cuts, expect that news to leak through the market’s “Fed Whisperers”—WSJ’s Nick Timiraos and FT’s Colby Smith.

Even with rate cuts expected, recent data has been anything but soft: CPI’s still hot, retail sales are solid, and last month’s jobs report surprised on the upside. But with payrolls on the horizon, some expect a weaker number—a “payback” that could nudge “Red Wave” vibes just days before the election. October’s report, muddied by strikes and hurricanes, will be tricky for policymakers to read and could stir more noise than clarity.

On the FX front, falling oil prices have offered some reprieve for the euro and yen, but widening swap differentials hint that markets might be pricing in a dovish trap door drop for both currencies. Crypto’s climbing, too, as Bitcoin rises and crypto companies see a boost from the chaos around the U.S. election, but mostly the Trump Trade factor.

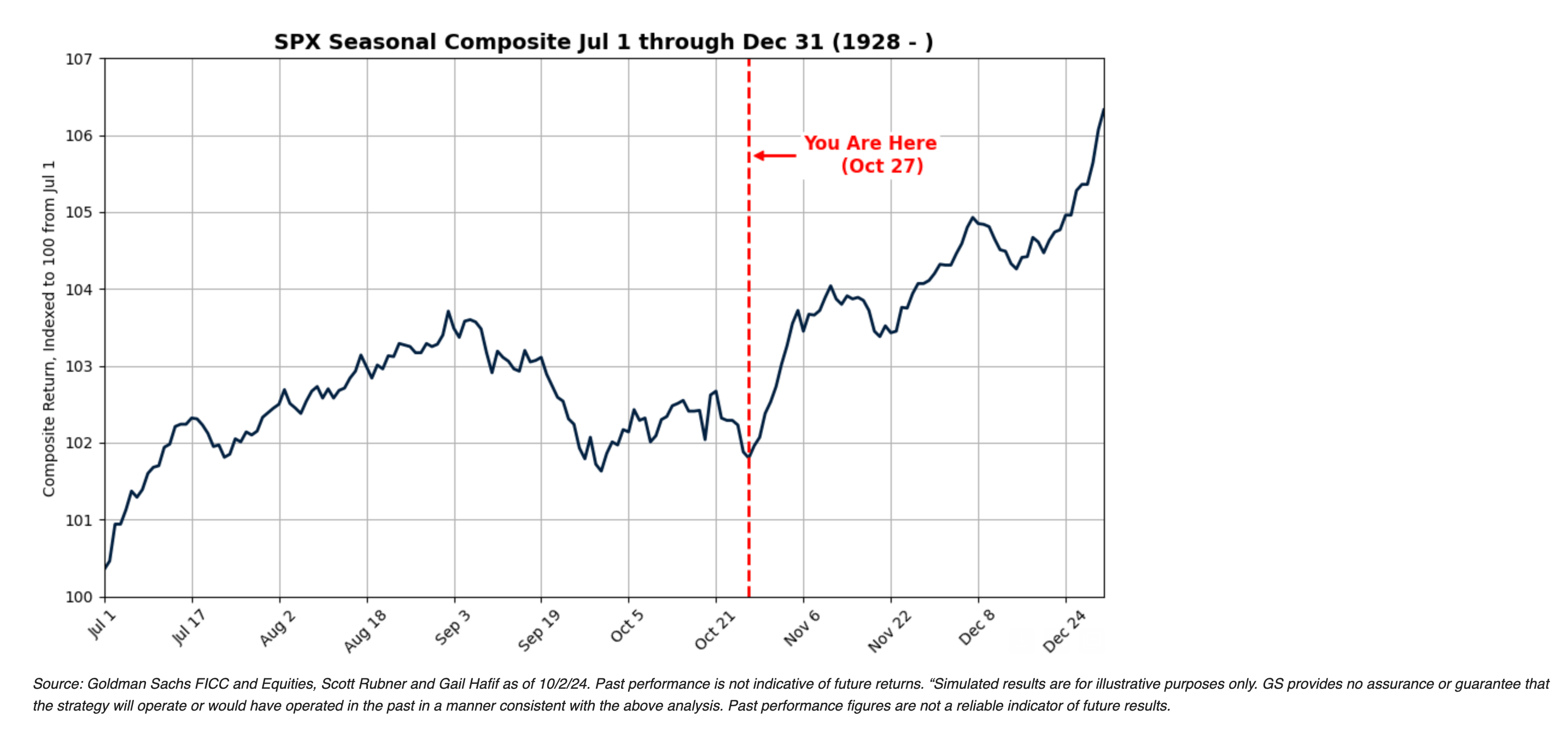

Meanwhile, Wall Street is gearing up for Big Tech earnings, with giants like Apple (AAPL), Microsoft (MSFT), and Meta (META) set to report. In the background, Goldman suggests corporate buybacks could boost stocks post-election. This time of year is also historically the market’s sweet spot, especially in election years. As Rubner, Goldman Palm Beach-based Delta One Salesman, reminds us, “Today kicks off the best trading stretch of the year,” with data from the past century backing up this trend. Hmm, Okki Dokki.

But when Wall Street’s “advising” on strategy, sometimes the most brilliant move is to tread carefully.

As I’ve noted, when Wall Street (or “ Worth Avenue “ in Palm Beach ) preaches certainty, remember that the future is inherently uncertain.

China's New Stimulus Efforts

China, meanwhile, is banking on the People’s Bank of China’s (PBOC) latest liquidity maneuvers to turn heads and ease some pressure. The PBOC has just rolled out a fresh lending tool to inject liquidity into the financial system—a timely move, considering that nearly 3 trillion yuan (about $406 billion) in loans are set to expire by year-end. With the clock ticking, Beijing hopes this tool will prop up market sentiment and counter any looming liquidity crunch.

The timing here isn’t just tactical; it’s essential. China’s economic engine has been sputtering with soft demand and lacklustre growth data, and with the potential shake-up of the U.S. election looming enormous, stability in the financial markets is critical for Beijing. If the liquidity injection gains traction, it could support equities and steady the yuan, offering a much-needed buffer against capital outflows.

Still, the success of this new tool isn’t guaranteed. Investors are eyeing just how effective the PBOC’s play will be, especially if global pressures mount post-election. It’s a high-stakes bet for China’s financial architects, and the world will be watching to see if this move can keep Beijing’s economic gears turning smoothly into the new year.

OIL MARKETS

The geopolitical risk premium in oil markets, heightened by Iran's missile attack on Israel on October 1, took a hit as oil prices tumbled with the easing of immediate conflict fears. However, tensions—and the embedded geopolitical risk—remain high, as some traders hedge against the possibility that Israel's initial strikes could signal the start of a broader campaign, particularly if Israel redirects its focus after addressing the immediate threats posed by Hamas and Hezbollah. Which is keeping a tentative floor under oil prices.

In the meantime, these shifting dynamics will likely bring OPEC’s supply strategy back into focus, highlighting a significant risk tail. With OPEC’s market share eroding in favour of the U.S. and other non-OPEC producers, there’s speculation that the cartel might raise output starting in December despite prices currently sitting below many members' fiscal breakeven levels. Such a move could add volatility as the oil market wrestles with both supply-side adjustments and ongoing geopolitical risks.

More By This Author:

Asia Open: Bracing For A Tilt-The-World Week

The Weekender: Election Speed Bumps Ahead

Tesla Triumphs While US Bond Yields Hit The Brakes