We see fair value for 10Y EUR swaps around 3% for the rest of this cycle, equivalent to a 10Y Bund around 2.25-2.5%. Federal Reserve cuts and a sluggish European recovery mean a dip in EUR rates around the middle of the year, but this will prove temporary.

2023, year of the turn

2023 starts with a number of dilemmas for European rates. On the macro front, milder weather has allowed gas storage to hold up much better than expected at the start of the winter season, and commodity prices more broadly have continued their decline. The resulting slowdown in energy prices has taken European inflation off its peak. But there is a catch: core inflation has not yet turned a corner, and the encouraging situation in the gas market means that the European Central Bank doesn’t face as worrying a growth picture when it decides to raise rates as was feared even a few months ago.

The net effect is an ECB with fewer qualms about tightening policy further. Our economics team now forecasts two more 50bp hikes at the February and March meetings, possibly followed by another 25bp increase in May. Contrast that with a Federal Reserve widely expected to reduce further the pace of hikes in February to 25bp, and to conclude its hiking cycle this quarter, and you have the second dilemma facing market participants: should EUR rates continue their climb until a clearer turn appears in ECB policy, or should they follow their USD peers lower, assuming that the ECB pivot will necessarily follow the Fed’s, albeit with a lag?

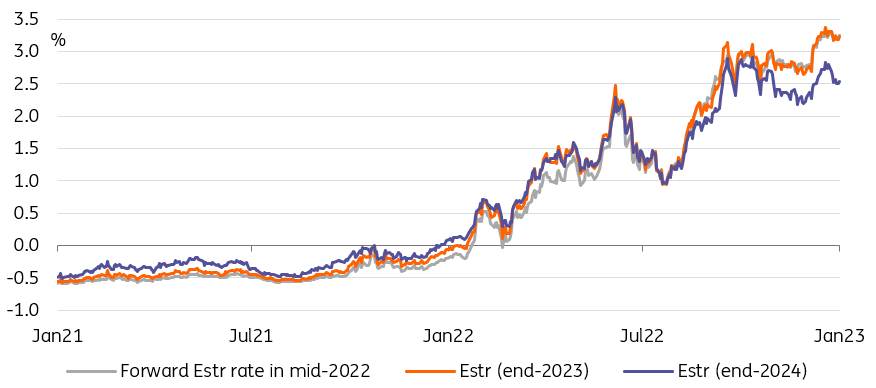

A hawkish shift at the ECB has also come with greater rate cut expectations in 2024

Source: Refinitiv, ING

A 3% fair value for 10Y swaps until the end of this cycle

The first step is to update where we see the long-term fair value (FV) for traded interest rates. Our economists’ expectation of a 3.25% peak in the ECB deposit rate, followed by cuts back to 2.5% by mid-2025, is close to the path implied by Euribor forwards. That path doesn’t include any inevitable cutting cycle beyond that year, as neither economists nor markets are comfortable with making recession calls more than three years ahead. This may seem surprising, but we think this state of play will persist until much closer to any rate-cutting cycle.

Assuming Euribor fixings will gradually rise relative to ECB policy rates as liquidity conditions are tightened, we have a fair value for 10Y EUR (against 6M Euribor) hovering around 3%. This estimate can move up or down based on the path of inflation and ECB policy but what matters, even more, is the market’s understanding of where rates would be cut to in a neutral setting. As the experience of the US has shown, hiking rates well above neutral typically results in an inverted curve, and means hikes aren’t transmitted to longer interest rates. We’re already seeing evidence of this in Europe.

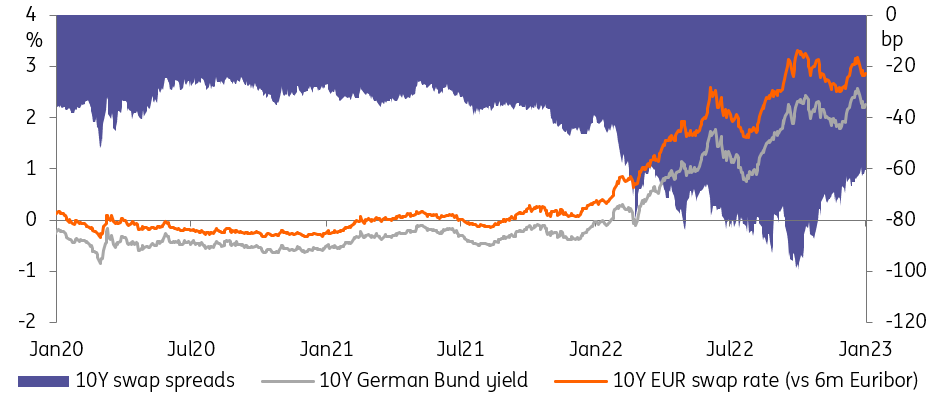

Whether the 10Y Bund settles around our 10Y EUR swap estimate depends on whether the swap spreads tightening trend continues. A lot of tightening has occurred in late 2022 so the pace will likely slow down but, as far as long-term fair value is concerned, a 2.25-2.5% range seems fair to us.

Swap spreads are a wild card in 1Q but tightening should resume later in 2023

Source: Refinitiv, ING

US read-across and a softer economy

This has to be weighed against a likely muted economic recovery in Europe, if it can be called that. Our economist colleagues forecast that, even taking lower gas prices into account, the eurozone economy will stagnate in 2023, at best. A softening global economy and the prospect of Fed cuts in the latter half of 2023 should put downward pressure on traded interest rates. The deep inversion of the US curve is an early illustration of this dynamic, although it has probably gone too far too quickly and will eventually reverse.

A trough in Bund yields around 2% by the middle of 2023 is entirely possible, as are temporary dips below that level in periods of economic gloom. Translating this to 10Y swap rates means that dips to 2.5% cannot be excluded. Bear in mind, however, that we see this coinciding with periods of economic angst, so this won’t necessarily bring better risk appetite in riskier markets. As 2023 progresses, we expect a re-steepening of EUR yield curves, and long-dated rates rising back to our fair value estimate.

Swap spreads at the beginning of the year are a potential wild card

The tightening in the fourth quarter, on easing collateral pressure and in anticipation of the first quarter supply surge, was the correct move but uncertainty remains about how the ECB will decide to treat government deposits placed at the Eurosystem. If nothing changes, these could amount to a significant amount of funds chasing collateral again by the end of April. This will be combined with still healthy swap paying flows in the first quarter as the ECB keeps market participants on their toes about the eventual end point of this tightening cycle. All this is to say that we wouldn’t be surprised to see swap spreads widen this quarter, before returning to their long-term tightening trend.

More By This Author:

Rates Spark: Headline Risk

FX Daily: Cautious Optimism Prevails

China: Timing Of Recovery Is A Big Question Mark

Comments

Log in or sign up to join the conversation.