Image Source: Pixabay

A lot of central bank comments will hit newswires today, but the odds of any meaningful signal being communicated to markets are low. On balance, we expect bonds to retain their bullish bias as long as today’s deals are well absorbed.

Bonds keep their bullish bias and look past Powell

Bonds continue to trade with a bullish bias. After weakness at the open yesterday, fixed-income markets recovered the ground lost thanks to the New York Fed consumer expectations survey seemingly confirming that the inflation upside is abating. Most notable was the reduction in inflation uncertainty and falling probability of three years ahead inflation remaining above 4%. Taken together, they aren’t sufficient to conclude that inflation is heading back to the Fed’s 2% target, but they will comfort investors in their view that the period of jumbo hikes from the Fed trying to cap inflation upside is behind us.

Too sharp a fall in market interest rates is detrimental to the Fed’s objective

The end of the Fed’s interest rate shock therapy is proving particularly beneficial for risk assets. In rates, the long-end has benefitted the most, courtesy of growing rate cut expectations: almost 50bp from the Fed Fund peak this year, and a further 150bp in 2024. While we agree, too sharp a fall in market interest rates is detrimental to the Fed’s objective. Indeed, while encouraging inflation news may spell the end of the aggressive phase of this tightening cycle, we expect the Fed to continue pushing back against cut expectations. This is in order to prevent financial conditions from easing too fast and undoing its policy-tightening work. Raphael Bostic was for instance insisting yesterday that the Fed should hold a rate above 5% through 2024.

Chair Jerome Powell is listed among today’s speakers. His attempts to impress his hawkish view on markets in recent months ended in failure. Recent data have, on balance, made his job even more difficult. For now, the focus is on the size of the next hike. Markets think 25bp is more likely, and both Bostic and Mary Daly said yesterday this is one of the options on the table. But the next step absents an effective pushback from the Fed is for the curve to price out any subsequent hikes, or even to price no more hikes in this cycle. Markets don’t need much encouragement to see the dovish side of everything.

US consumers see lower inflation upside and inflation uncertainty within three years

Image Source: Refinitiv, ING

Headline and supply risk today in Europe

Over in Europe, a paper by the European Central Bank (ECB) seemed to foresee a further acceleration of wages in the coming quarters. Whilst ECB economic papers aren’t a conduit for policy signals, wages are a key piece of the inflation puzzle in Europe and elsewhere. We expect the view of research staff on that topic to be something that resonates with governing council members, and by extension with markets. Along a similar vein, Bank of England (BoE) chief economist Huw Pill listed the reasons why inflation in the UK risks being more persistent than in Europe. The speech was full of hawkish soundbites but the fact that it was mostly backward-looking provided an excuse for bonds to ignore them.

Issuance has failed to make much of a dent in the (US-led) rally in bonds

There is also a long list of ECB and BoE speakers today. If recent history is any guide, a hawkish tone will dominate but the format of panel discussions brings the risk of out-of-context comments being reflected in headlines in news services. The other main potential market-moving event today is supplying. So far, issuance has failed to make much of a dent in the (US-led) rally in bonds but much will depend on how well each deal is received.

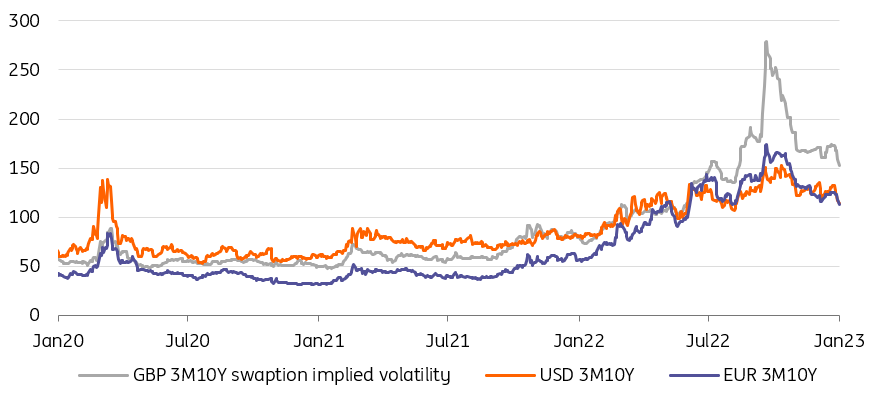

Falling implied volatility shows markets think the central bank shock therapy is behind us

Image Source: Refinitiv, ING

Today’s events and market view

November industrial production figures from France and Spain start today’s list of economic releases, followed in the afternoon by US small business optimism survey. The questions relating to hiring intentions and prices will as usual be more closely watched.

The Riksbank symposium speakers list includes central bank household names such as Isabel Schnabel of the ECB, Andrew Bailey of the BoE, Hurahiko Kuroda of the Bank of Japan, and Jerome Powell of the Fed. All are listed as taking part in panel discussions which isn’t an obvious format to send policy signals but brings the risk of misleading headlines.

As is usually the case in January, bond supply is what will keep a large part of market participants busy today. On the sovereign side, Belgium (10Y) and Italy (20Y, green) mandated banks for a syndicated deal that should materialize today. This will come on top of scheduled auctions from the Netherlands (3Y), Austria (3Y/24Y), and Germany (10Y Linker).

The US Treasury starts this week’s issuance slate with a 3Y T-note auction, this will be followed by 10Y and 30Y sales later in the week.

More By This Author:

FX Daily: Cautious Optimism PrevailsChina: Timing Of Recovery Is A Big Question Mark

Japan: A Modest Recovery Will Continue To Be Supported By Accommodative Macro Policies

Comments

Log in or sign up to join the conversation.