First Brands: Canary In The Rehypothecation Coal Mine?

The First Brands Group, manufacturer of auto parts, including Raybestos brakes and FRAM, filed for bankruptcy on September 29th. This bankruptcy is troubling in two ways.

First, per the ZeroHedge chart below, the price of First Brands loans fell by 80% in a day. In other words, the loan market had no clue of financial problems or accounting irregularities. To that end, financial investigators are discovering a complex maze of undisclosed off-balance sheet financing. Initially, it was thought that First Brands had about $6 billion in liabilities, but after some investigative work, it is now over $10 billion and growing.

Second is the issue of what appears to be the fraudulent rehypothecation of collateral backing the loans. Rehypothecation refers to using the same collateral for multiple loans and lenders. Here is an example:

- First Brands borrows $1 million from Lender A, backed with accounts receivable invoices of $2 million. The lender presumes that the collateral is more than enough to pay off the loan if First Brands fails to repay it.

- First Brands then goes to lender B and uses the same invoices to secure another $1 million loan.

- First Brands defaults. Lender A and B not only realize that First Brands can’t pay their debts, but they also do not have the exclusive rights to the collateral supporting the debt. Thus, the collateral is insufficient to cover their losses.

- The rehypothecation allowed First Brands to take on much more debt than would have otherwise been possible.

This event could have a ripple effect throughout the vendor financing industry, making it harder for small and mid-sized companies that regularly use trade financing to sustain operations. Furthermore, Jefferies Financial, one of First Brand’s bankers, may encounter some challenges. Per ZeroHedge:

As a result, Bloomberg reports that for Jefferies – who is, or rather was, First Brands’ banker for more than a decade – the speculation around its role in the sudden demise of First Brands has became too loud to ignore, and the bank has come under scrutiny for its relationship with the insolvent company and its spectacular collapse.

What To Watch Today

Earnings

(Click on image to enlarge)

![]()

Economy

(Click on image to enlarge)

![]()

Market Trading Update

Markets ended last week on a sour note. After several days of warnings, the S&P 500 fell sharply on Friday, closing 2.71% lower. That single-day move erased the week’s earlier gains and shifted the technical tone heading into next week. The index had previously maintained a record-long streak, 112 consecutive sessions, above its 50-day moving average. That trend is now threatened if selling pressure continues into early next week.

As shown, the negative divergence in relative strength warned of a potential for a sharp reversal. Momentum readings (RSI, MACD) were elevated heading into Friday, creating fragility. The drop on Friday took out the 20-day moving average, and the 50-day moving average, as noted, is crucial support heading into next week. The sudden drop also breached the bullish trend line that has been intact since May, suggesting there is risk to the downside.

(Click on image to enlarge)

Support/resistance levels

- Near-term resistance: ~6,750, which coincides with recent market highs.

- Key support: ~6,529 or the 50-day moving average. A breach of that support could usher in further weakness.

- Deeper support: ~6,381, which aligns with market dips.

- Critical support: ~6,049 of the 200-day moving average. That level must hold, or other factors are likely at play.

Friday’s sell-off was tied to multiple catalysts. Renewed geopolitical tensions and talk of tariff escalation added a layer of macro stress. At the same time, the lack of incoming economic data due to the government shutdown has increased uncertainty. Without CPI or PPI updates, traders are flying blind on inflation and wage pressures. As noted, that vacuum creates fragility, especially when momentum is already stretched and volatility is compressed. Breadth remains narrow, with most gains still concentrated in mega-cap tech, which was also responsible for the bulk of the drop on Friday. That makes the broader market more sensitive to any weakness in leadership names. The technical picture has shifted from stable to vulnerable in just one session. Next week will be critical in determining if this is a short-term shakeout or something more.

The Week Ahead

The bond market will be closed on Monday for the Columbus Day holiday. Like last week, due to the shutdown, we are unsure of what government economic data will be reported. That said, the media is reporting that the government is recalling some BLS employees deemed essential to release the September CPI report. Thus, later in the week, the September BLS employment report could be released. CPI, PPI, and Retail are on the calendar, but even if the government shutdown ends, it is likely these reports will take some time to compile.

Given the lack of economic data, earnings reports should take center stage. This week features earnings from the big banks, including JP Morgan, Citigroup, Wells Fargo, and Goldman Sachs, on Tuesday. JNJ, Kinder Morgan, and American Express will also report this week.

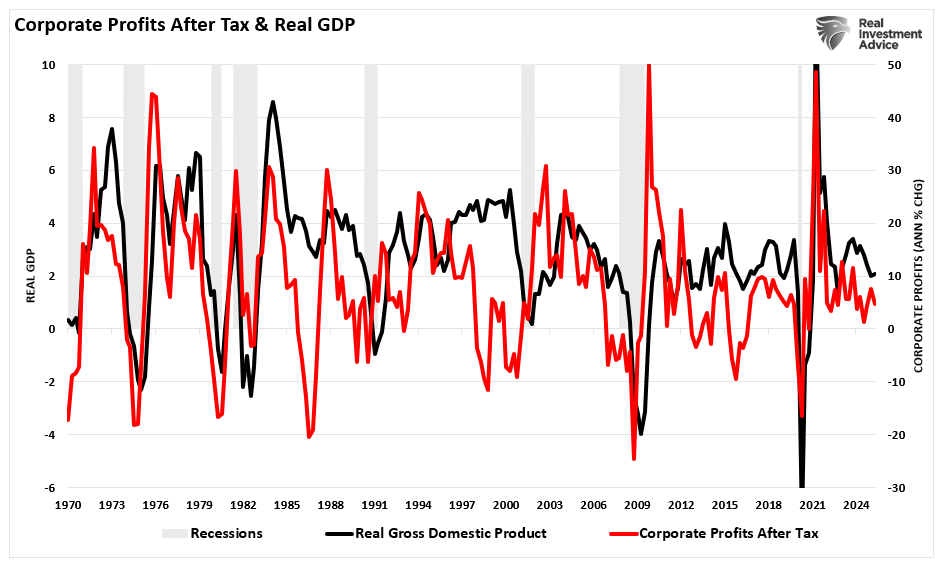

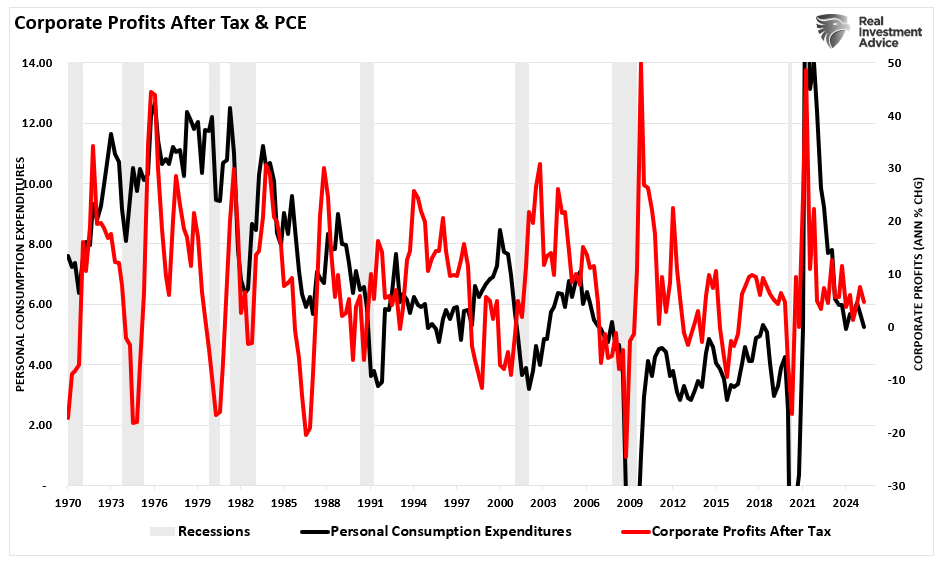

Corporate Profits: A Reading Without Rose-Tinted Glasses

If you want to understand where we are in the cycle, skip the noise and follow profits. Corporate profits are the lifeblood of investment, hiring, and market returns. Crucially, linkage to the real economy is very tight. In the national accounts (NIPA), the BEA’s “profits from current production” (with inventory valuation and capital consumption adjustments) rose in Q2-2025, but only modestly: up $6.8 billion from Q1, and notably revised down by $58.7 billion from the prior estimate. That’s not the surge you’d expect if we were entering a new, powerful profit upswing. The correlation is unsurprising, given that economic activity generates the revenue to obtain corporate profits.

While the revision to the third estimate of real Q2 GDP growth increased to 3.8% annualized, all was not what it seemed. The reversal of the import surge in Q1 to get ahead of tariffs did the heavy lifting in Q2. More notably, consumer spending, the main driver of economic activity, showed continued weakness. Again, the linkage between PCE and corporate profits is critical, given that spending generates corporate revenues.

The point for investors is that while the economic growth number “looks” hot, the profits revision tells a quieter story about corporate income momentum. In other words, output accelerated, but profit growth didn’t follow in lockstep. READ MORE…

Tweet of the Day

More By This Author:

Market Crack Or Beginning Of Something BiggerCorporate Profits: A Reading Without Rose-Tinted Glasses

The AI Trillion Dollar Question

Disclaimer: Click here to read the full disclaimer.