Abstract

This paper identifies the bitcoin investor network and studies the relationship between connections and returns. Using transaction data recorded in the bitcoin blockchain from 2015 to 2020, we reach three conclusions. First, connectedness is not strongly correlated with higher returns in the first four years. However, the correlation becomes strong and significant in 2019 and Second, returns also differ among those connected addresses. By dividing the connected addresses into ten decile groups based on their centrality, we find that the top 20% most connected addresses earn higher returns than their peers during most of our sample period. Third, eigenvector centrality is more related to higher returns than degree centrality for the top 20% most-connected addresses, implying that the quality of connections may matter more than quantity among those highly connected addresses.

Do connections pay off in the bitcoin market?

- Kwok Ping Tsang and Zichao Yang

- Journal of Empirical Finance

- A version of this paper can be found here

What are the Research Questions?

Traditional asset pricing theory holds that the workings of information networks among investors are good descriptors of equity markets. Investors that are “better informed” about fundamentals and who trade earlier than less well informed investors will receive higher returns. As the” better information” is passed on through trading, “less informed” investors will eventually join in but earn lower returns. This paper attempts to determine whether or not the same mechanisms characterize largely unregulated crypto markets like bitcoin. The authors calculate returns and how they differ among investors inside the bitcoin network using address-level transaction data. From the network, all the qualified transaction addresses are clustered into a connected group and an unconnected group and three questions are specifically addressed:

- Do connected bitcoin addresses earn a higher return when compared with bitcoin addresses that are unconnected in the bitcoin investor network?

- Do more connected addresses earn a higher return than less connected ones?

- When centrality is used to measure an address’ connectedness, which centrality (either degree centrality or eigenvector centrality) is more related to higher returns?

The data source is Google’s bitcoin transaction dataset. Although beyond the scope of this summary, the authors provide a comprehensive description of the technical aspects about bitcoin that help understand the paper. I would recommend reading the paper just for that content.

What are the Academic Insights?

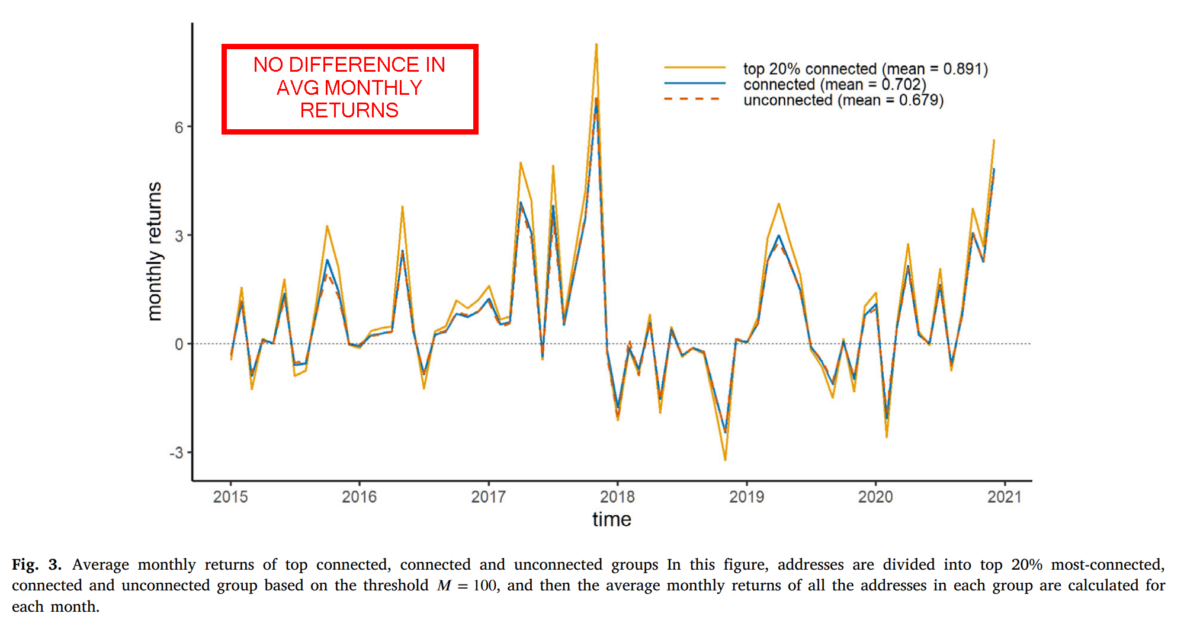

- NO. The authors detected no pattern suggesting the group of bitcoin users with connections is able to generate higher returns than the unconnected group during the sample period, with the exception of 2019-2020, where returns were higher. See Figure 3 below. The data consisted of a bitcoin investor network constructed out of bitcoin blockchain transactions observed over the period 2012-2020.

- YES. Based on their centrality measure, all connected addresses were sorted into ten deciles. The connected group includes addresses that have at least one connection with other addresses. The unconnected group includes the remaining addresses. For the addresses, the two most connected deciles produced consistently higher returns than any other connected addresses. For example, connected addresses in the bottom decile returned 5.7% higher than the unconnected group. The top 20% most connected addresses always outproduce the remainder.

- Across the entire sample and for the most connected addresses, the high eigenvector centrality measure is associated with higher returns.

Why Does it Matter?

Without arguing the question of whether or not bitcoin has fundamental value, this analysis instead treats the topic as a microstructure issue. The price and popularity of bitcoin is indeed affected by news regarding the size of its usage, innovation in technology, changes in regulations and so on. It is in that regard, that market for bitcoin is similar to the market for equities—“with more investors who are more centrally placed on average earning higher return than others.”

The Most Important Chart from the Paper

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Comments

Log in or sign up to join the conversation.