Most of the major asset classes scored gains last week, led by US real estate investment trusts, based on a set of ETFs through Friday’s close (Jan. 27).

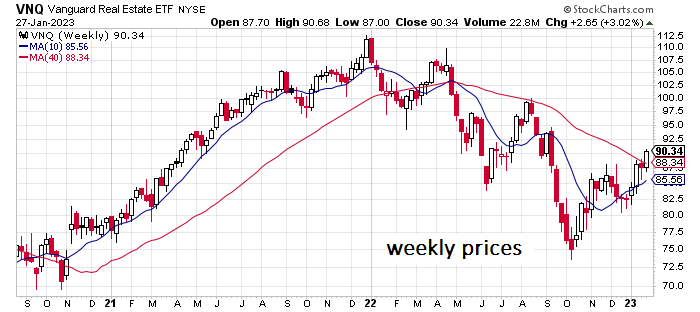

Vanguard Real Estate Index Fund (VNQ) gained 3.0% last week, lifting the ETF to its highest close since September. Part of the reason for the rebound in REITs is probably linked to speculation that the Federal Reserve is close to ending its rate hikes. If true, the relatively high-yielding real estate sector’s allure shines that much brighter. VNQ’s trailing 12-month yield is 3.91%, according to Morningstar.com – modestly above the 10-year Treasury yield (3.52% as of Jan. 27). Assuming bond yields are peaking, the payout premium in REITs looks set to rise.

The question for yield-focused investors is whether the attractive payout will compensate for market volatility in the near term? The recent strength in risk assets generally persuades some analysts to see better days ahead after a sharp correction in stocks and bonds in 2022. But Morgan Stanley strategists say it’s still too early to ring the all-clear bell.

“Better price action in stocks has started to convince many investors they are missing something — compelling them to participate more actively,” write Michael Wilson and his team in a research note. “We think the recent price action is more a reflection of the seasonal January effect and short covering after a tough end to December and a brutal year.”

Last week’s losers: commodities (GCC) and government bonds in developed markets ex-US (BWX).

The Global Market Index (GMI.F), an unmanaged benchmark maintained by CapitalSpectator.com, rebounded last week, gaining 1.6%. This index holds all the major asset classes (except cash) in market-value weights via ETFs and represents a competitive measure for multi-asset-class-portfolio strategies.

Nearly all the major asset classes continue to suffer losses for the trailing one-year window. Commodities (GCC) are still the lone outlier, posting a modest 4.2% gain at Friday’s close vs. its year-ago price.

GMI.F’s one-year performance is in the hole by 6.0%.

Comparing the major asset classes through a drawdown lens continues to show relatively steep declines from previous peaks for most markets around the world. The softest drawdown at the end of last week: US junk bonds (JNK) with a 9.1% slide from its last peak.

GMI.F’s drawdown: -13.1%.

More By This Author:

Is US Recession Risk High, Low… Or Both?

Is Rally In Communications Stocks A Sign Of New Sector Leadership?

Fed Pivot Watch - Wednesday, Jan. 25

Comments

Log in or sign up to join the conversation.