Swinging For The Fences

Ready to swing for the fences. Photo via Pixabay.

Getting Aggressive

Often we focus on limiting risk because many of our subscribers are older investors with a lot to risk. But we have some younger subscribers with less money but larger risk tolerances. Here's a solution our system came up with for one of those investors on Wednesday.

When You're Willing To Risk A Large Decline

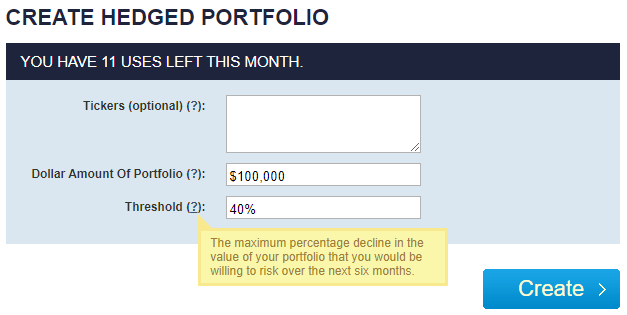

Ordinarily, we'd consider an aggressive investor someone who was willing to risk a decline of up to 20% over six months. But what if you were willing to risk twice that? Here's what that looked like for an investor with $100,000 to put to work on Wednesday. He entered $100,000 as the dollar amount of his portfolio on our site, and 40% as his decline threshold.

This and subsequent screen captures are via Portfolio Armor.

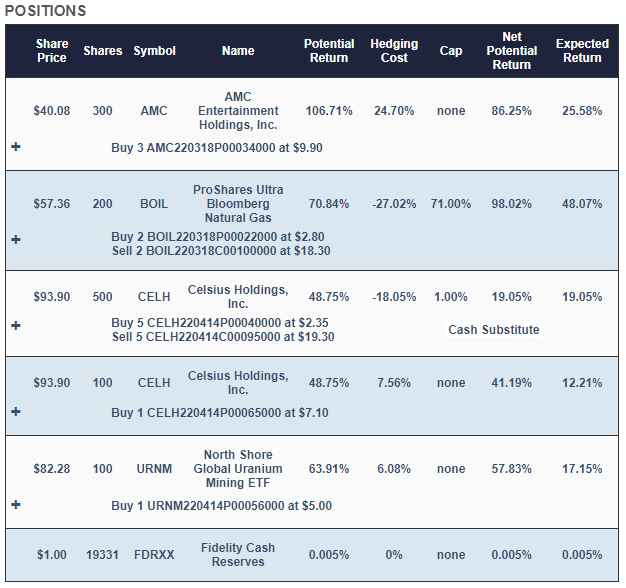

After clicking "Create" and waiting for a few moments of data crunching, this is the portfolio the site presented him.

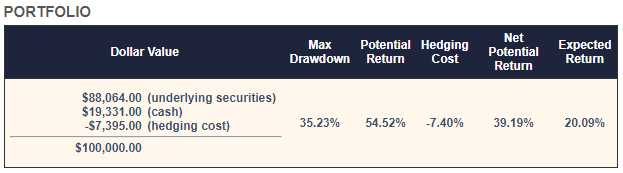

With this, his maximum drawdown over the next six months - that is, if every underlying security went to zero - would be a decline of 35.23%. The hedging cost was -7.4%, meaning that if the underlying security prices didn't move at all over six months, he'd be up 7.4% from the aggregate net credit. And his expected return here was a gain of about 20% over six months (while this portfolio could return anything above the maximum drawdown, the expected return is a ballpark estimate of how this sort of portfolio would perform on average if you ran it multiple times).

Why Those Names?

Each trading day, our system analyzes total returns and options market sentiment to estimate potential returns for thousands of stocks and ETFs. AMC Entertainment Holdings, Inc. (AMC), the ProShares Ultra Bloomberg Natural Gas ETF (BOIL), Celsius Holdings, Inc. (CELH), and the North Shore Global Uranium Mining ETF (URNM) were selected because they were among our top names: the ones that had the highest potential returns, net of hedging costs (we wrote about AMC in our previous post: Meme Stock Meets Meme Cryptocurrency, and we wrote about BOIL earlier this month, Supply-Side Inflation Hits Home). Our system started with roughly equal dollar amounts of each, and then rounded them down to round lots, to reduce hedging costs. It swept up most of the leftover cash from the rounding-down process into a tightly hedged CELH position, to further reduce hedging cost.

Why Those Hedges?

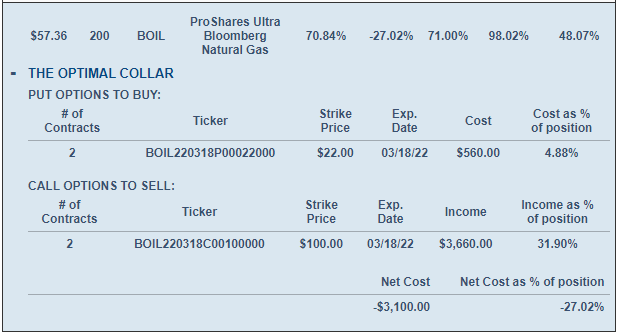

On our website, if you click the plus signs in the portfolio above, the positions expand to give you a better look at the hedges. For example, this is what the BOIL position looks like expanded.

As you can see, BOIL was hedged with an optimal, or least expensive, collar. Some of the other positions are hedged with optimal puts. Our system estimates return both ways to determine which type of hedge is best. We elaborated on that process in a previous post: When To Hedge With Puts Versus Collars.

Smoothing Out Returns

With a concentrated portfolio like this, you'll likely see some volatility in returns: you'll hit some home runs, and you'll strike out some times. A way to smooth out your returns is to split your money in a couple of tranches and invest half now and then the rest in three months. Since each portfolio lasts for six months, you'll get four at-bats per year with that approach. If you prefer, you could use three tranches and invest one every two months, for six at-bats.

We'll check back on this one in six months and see if it was a home run, a strikeout, or something in between.

As a reminder, we're raising our prices by a third at the end of the week, but current customers will be grandfathered and retain our current prices.

Disclaimer: The Portfolio Armor system is a potentially useful tool but like all tools, it is not designed to replace the services of a licensed financial advisor or your own independent ...

more