Crisis Investing

A Gadsden flag hung out of a Southwest Airlines 737 cockpit. Photo via American Greatness.

A Market Buffeted By Bad News

The apparent work slowdown at Southwest Airlines (LUV), snarling air travel last weekend, is the latest bit of bad news to hit the economy and markets. Since we shared our bear-proof portfolio back in July ("Building A Bear-Proof Portfolio"), we've had the ongoing energy crisis, the China Evergrande (EGRNF) crisis, and the supply-chain crisis ("America Is Running Out Of Everything"). Altogether, this seems like a good test of a portfolio built to manage unforeseen risks. Let's see how it's done so far. First, a quick recap of how we built the portfolio.

Our Approach To Crisis Investing

In short, it's to buy and hedge a handful of names that a) we estimate will do well over the next several months and b) are relatively inexpensive to hedge. The goal here is to do well while the market goes up, and limit your downside if it doesn't.

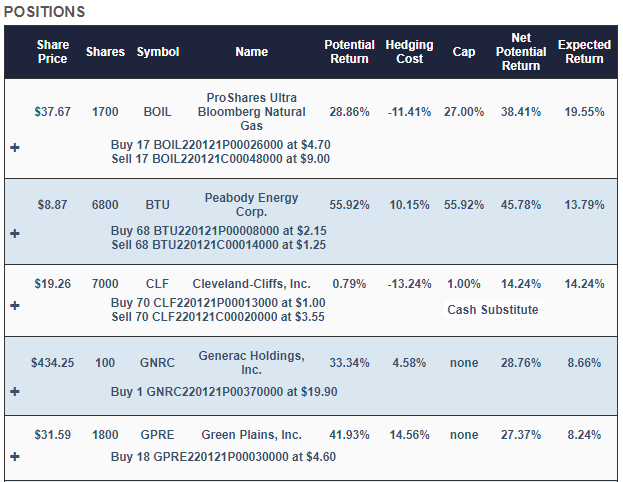

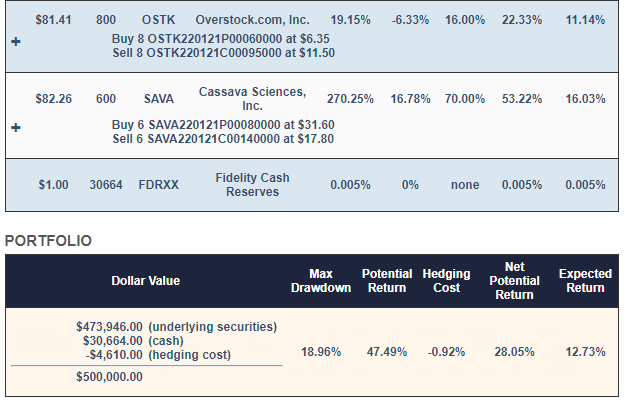

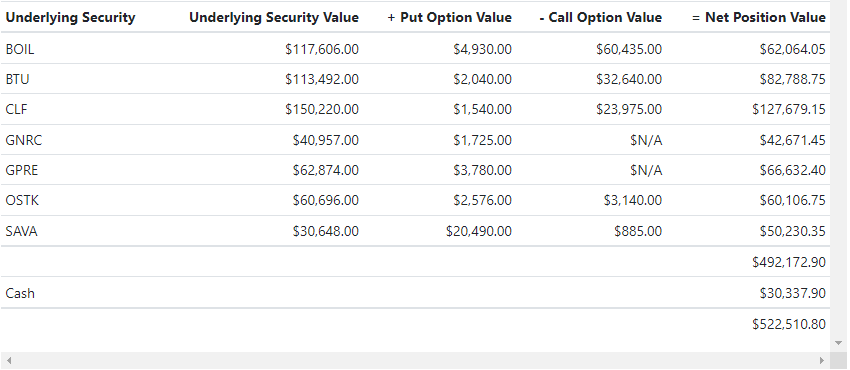

Using that process, this is the portfolio our system generated in July for someone with $500,000 to invest who was unwilling to risk a decline of more than 20% in the event of a catastrophic crash:

Screen captures via Portfolio Armor on 7/19/2021.

Why Those Stocks?

Each trading day, our system analyzes total returns and options market sentiment to estimate potential returns for thousands of stocks and ETFs. The ProShares Ultra Bloomberg Natural Gas ETF (BOIL), Peabody Energy (BTU), Generac Holdings (GNRC), Green Plains (GPRE), Overstock.com (OSTK), and Cassava Sciences (SAVA) were selected because they were among our top names: the ones that had the highest potential returns, net of hedging costs. Our system started with roughly equal dollar amounts of each, and then rounded them down to round lots, to reduce hedging costs. It swept up most of the leftover cash from the rounding-down process into a tightly hedged Cleveland-Cliffs (CLF) position, to further reduce hedging cost.

Why Those Hedges?

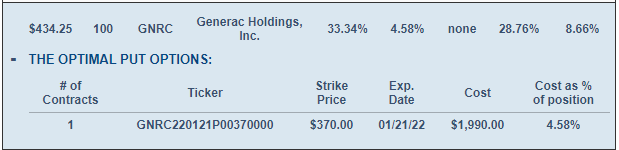

On our website, if you click the plus signs in the portfolio above, the positions expand to give you a better look at the hedges. For example, this is what the GNRC position looks like expanded.

GNRC is hedged with an optimal, or least expensive, put option. Most of the other positions are hedged with optimal collars. Our system estimates returns both ways to determine which type of hedge is best. We elaborated on that process in a previous post: When To Hedge With Puts Versus Collars.

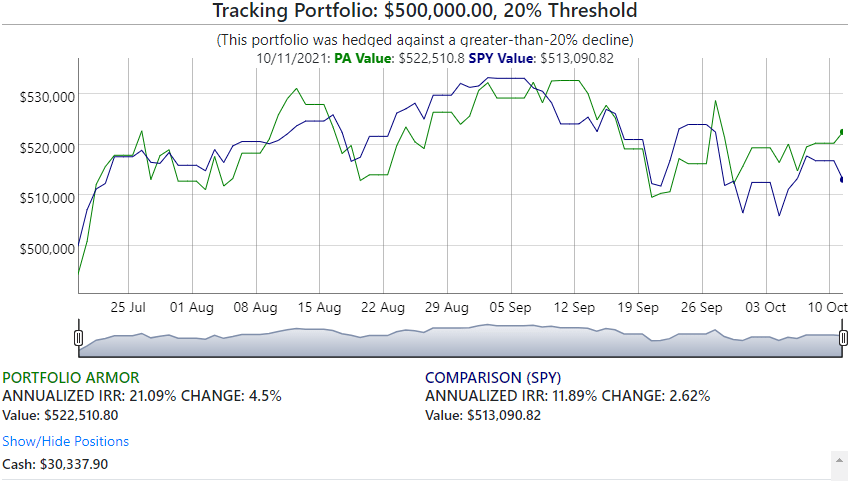

Enough Details: How Is It Doing So Far?

Net of hedging and trading costs, was up 4.5% as of Monday's close, versus SPY which was up 2.62% over the same time period.

So far, not bad.

Disclaimer: The Portfolio Armor system is a potentially useful tool but like all tools, it is not designed to replace the services of a licensed financial advisor or your own independent ...

more