Could data centers and the power grid be America’s next “renaissance?” With the U.S. national debt exceeding $37 trillion and interest payments surpassing defense spending, many articles have been written about the “debt doomsday” event coming. Such was a point we made in “The Debt and Deficit Problem.”

“In recent months, much debate has been about rising debt and increasing deficit levels in the U.S. For example, here is a recent headline from CNBC:”

“The article’s author suggests that U.S. federal deficits are ballooning, with spending surging due to the combined impact of tax cuts, expansive stimulus, and entitlement expenditures. Of course, with institutions like Yale, Wharton, and the CBO warning that this trend has pushed interest costs to new heights, now exceeding defense outlays, concerns about domestic solvency are rising. Even prominent figures in the media, from Larry Summers to Ray Dalio, argue that drastic action is urgently needed, otherwise another “financial crisis” is imminent.”

As we discussed in that article, the “purveyors of doom” have been saying the same thing for the last two decades, yet the American growth engine continues chugging along. Notably, Ray Dalio and Larry Summers focus on only one solution: “cutting spending,” which has horrible economic consequences.

“Furthermore, investors must understand a critical accounting concept: that the government’s debt is the household’s asset. In accounting, for every debit there is a credit that must always equal zero. In this case, when the Government issues debt (a debit), it is sent into the economy for infrastructure, defense, social welfare, etc. That money is “credited” to the bank accounts of households and corporations. Therefore, when the deficit increases, that money winds up in economic activity, and vice versa. In other words, those shouting for sharp deficit reductions are also rooting for a deep economic recession.” – The Deficit Narrative

The other challenges with cutting spending are that it is politically toxic, and tax hikes drag on growth.

However, one solution that all the mainstream “doomsayers” overlook is raising productivity and GDP through private-sector capital investment. In other words, as the U.S. did following World War II, it is possible to “grow your way out of your debt problem.”

That’s where the AI data center boom and massive electricity demand come in.

The Economic Engine of Capex

The buildout of data centers and the power grid may offer the best opportunity to generate sustained growth. The scale of investment is large enough to matter, the economic multipliers are high, and the timeline aligns with when fiscal pressure will peak.

Data centers are the backbone of the digital economy. AI models, cloud platforms, and automation rely on them, and each large AI model requires thousands of GPUs housed in purpose-built facilities. These are not minor server rooms. They are $1 billion-plus industrial complexes. But, for the build-out of “data factories” to impact economic growth, a massive investment will be required to affect a $30 trillion (nominal) U.S. economy.

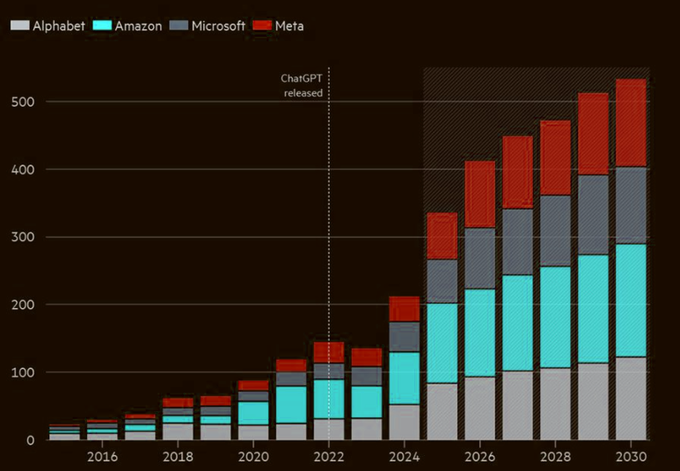

How much are we talking about? As noted in our previous article on data center demand, McKinsey projects that data center investment will reach $7 trillion globally by 2030. Over 40 percent of that will happen in the U.S. Alone. Moreover, Nvidia’s latest quarterly report forecasted data center capital expenditures by Apple, Meta, Microsoft, and Alphabet to reach $4 trillion by 2030, or roughly $1 trillion annually.

However, you can’t build a data center without power.

Data Centers Require Power

According to the Department of Energy, U.S. data center electricity consumption could double or triple by 2028. Deloitte expects a 30-fold increase in AI-related data center power usage by 2035, reaching 123 gigawatts. That’s more than the total residential demand in California. This means building new substations, transmission lines, and power plants. Therefore, as noted by Edison Electric Institute, investor-owned U.S. electric utilities will invest more than $1.1 trillion in the 2025-2029 period to meet that demand.

This infrastructure boom will not be optional. AI development needs low latency, which requires local capacity and reliable electricity. Since data centers are capital-intensive and mission-critical, the U.S. economy could see between $1.25 and $1.5 trillion in annual capex spending.

Why is that critical to our “debt to GDP” concerns? Large-scale capital spending is one of the few economic inputs reliably boosting long-term growth. Unlike stimulus checks or tax credits, infrastructure spending creates durable productivity improvements. We are already seeing this impact.

- The PwC study for the Data Center Coalition found that from 2017 to 2021, U.S. data centers added $2.1 trillion to GDP. That’s before the AI acceleration began.

- According to Reuters, in Q2 2025, AI-related capex accounted for over one-third of real GDP growth, which added roughly 0.4 percentage points to quarterly GDP.

The Multiplier Effect

But it isn’t just $1 trillion in CapEx. These projects create upstream demand for construction, power equipment, semiconductors, cooling systems, and skilled labor. They support engineering, real estate, logistics, and utility services. Most notably, they set the stage for sustained gains in productivity. Once operational, AI systems reduce costs, improve decision-making, and enable scale in industries from health care to manufacturing. In other words, there is a “multiplier effect” to these projects. The American Society of Civil Engineers (ASCE) estimates that every $1 billion in infrastructure investment creates 13,000 jobs and adds $3 billion to GDP over a decade.

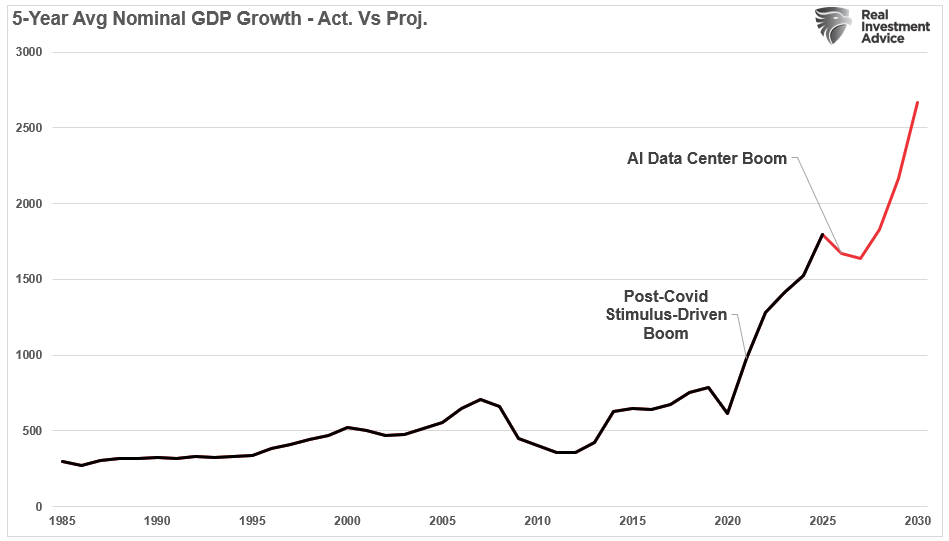

Therefore, by 2030, if the $5 trillion in combined investment in AI data centers and power generation comes to fruition, the U.S. economy will see an additional $15 trillion in growth. The chart below shows the average 5-year growth rate in nominal GDP and projected growth.

The chart below assumes we will continue to issue debt at the average quarterly pace since 2021. However, instead of wasting money, we focus on productive investments while maintaining all current spending programs and obligations. Assuming some conservative growth estimates resulting from the investments, the “debt to GDP” ratio will begin declining in 2026 and revert to more sustainable levels by 2030.

However, this isn’t a guarantee, but it is certainly potentially more realistic than a “debt crisis” that sends the U.S. into an economic depression.

Risks and Constraints

The growth opportunity is significant, but not risk-free. While the bears constantly ring the alarm bell about the current level of debt and deficits, the more dire economic consequences they forecast may fail to come to fruition.

As noted by Goldman Sachs:

“Generative artificial intelligence has the potential to automate many work tasks and eventually boost global economic growth. AI will start having a measurable impact on US GDP in 2027 and begin affecting growth in other economies worldwide in the following years. The foundation of the forecast is the finding that AI could ultimately automate around 25% of labor tasks in advanced economies and 10-20% of work in emerging economies.”

They currently estimate a growth boost to GDP from AI of 0.4 percentage points in the US.

Increases in productivity, productive capital investment, and increased labor demand for the infrastructure buildout (which will also result in higher wages) should provide the economic boost needed.

Conclusion

Will it solve all of the current socio-economic ills facing the U.S.? No. However, it may provide the growth boost necessary to revitalize economic growth and prosperity in the U.S., which we have not seen since the 1970s. But there are risks to this outlook.

- The scale of spending may lift electricity prices. A study from NC State found national prices could rise 8 percent by 2030, with some localities seeing 20–25 percent jumps. If not managed, this could erode industrial competitiveness.

- Jobs per dollar of investment are low. Data centers are automated. Once built, they require few workers. A $1 billion facility may employ only 100 people full-time.

- There is a local backlash. Projects require land, water, and energy. Communities are resisting tax incentives and environmental costs. Several counties have imposed moratoriums.

- Permitting delays and regulatory hurdles remain high. The average interconnection wait for new power projects is over 3 years. Without reform, many AI investments will be delayed or redirected.

The government will need to be involved to unlock the full economic benefit.

- Public policy must streamline permitting, including environmental review, grid interconnection, and land use.

- Given that infrastructure and national security are at stake, a public/private partnership should be involved.

- Tax policy should avoid distortion. Many subsidies go to projects that were already economically viable.

- The focus should be on shared infrastructure, such as transmission lines, regional data hubs, and reliability upgrades.

- Utilities need regulatory clarity. Traditional cost-of-service models may not align with the fast pace of AI demand, so performance-based rates or return-on-equity mechanisms may be required.

- Energy policy must support generation diversity. Solar and wind are inefficient, and AI demands require firm natural gas, nuclear, and advanced storage capacity.

The goal should be energy abundance. High reliability, low prices, and scalable infrastructure will attract private AI investment and increase growth.

It may also just be enough to keep the demise of the U.S. from occurring any time soon.

More By This Author:

Market Mechanics Override Weakening Economic DataThe Fed Cuts Rates: What Comes Next?

Semiannual Reporting Requirements Are Overhyped

Comments

Log in or sign up to join the conversation.