The death of George Floyd was both unjust and tragic. However, his death was the catalyst that lit a powder keg of dissension, which has simmered beneath the headlines for over a decade.

While we focus on events that fill our media streams, it is worth remembering Oscar Grant, Trayvon Martin, Manuel Diez, Kimini Gray, and Michael Brown. These events, and many others throughout history, show civil unrest has deeper roots. Pew Research made a note of this in 2017:

“The U.S. economy is in much better shape now than it was in the aftermath of the Great Recession. It cost millions of Americans, their homes, and jobs. It led him to push through a roughly $800 billion stimulus package as one of his first business orders. Since then, unemployment has plummeted from 10% in late 2009 to below 5% today, and the Dow Jones Industrial Average has more than doubled.

But by some measures, the country faces serious economic challenges: A steady hollowing of the middle class and income inequality reached its highest point since 1928.”

Look at the faces of those rioting. They are of every race, religion, and creed. What they all have in common is they are of the demographic most impacted by the current economic recession. Job losses, income destruction, financial pressures, and debt create tension in the system until it explodes.

It has been the same in every economy throughout history. While the rich eat cake, the rest beg on street corners for scraps. Eventually, those most disenfranchised and oppressed storm the castle walls with “pitchforks and torches.”

The Root Of The Problem

A recent article by MagnifyMoney hit on this issue.

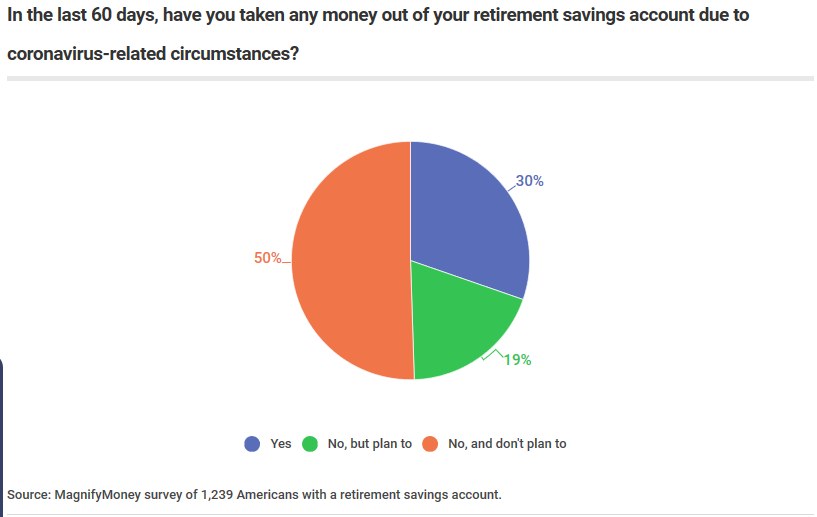

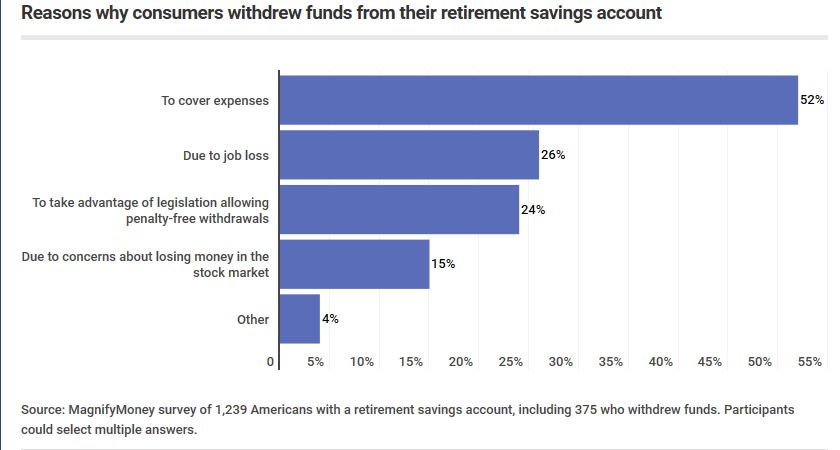

“As the coronavirus pandemic continues to pummel the economy, many Americans are decreasing their retirement contributions, but some are raiding their retirement accounts to pay for essentials. A new survey found 3-in-10 Americans dipped into the funds meant for their golden years — and the majority of those who have done so spent their nest egg on groceries.”

America was not prepared financially for the downturn caused by the pandemic. They are angry, financially stressed, and the visible face of their ire has become Wall Street and the Fed.

Since the “Financial Crisis,” the role of the Federal Reserve shifted from its dual mandate of “full employment” and “price stability” to a seeming inclusion of a “third mandate” supporting consumer confidence via the inflation of asset prices. As Ben Bernanke stated in 2010:

“This approach eased financial conditions in the past and, so far, looks to be effective again. Stock prices rose, and long-term interest rates fell when investors began to anticipate the most recent action.

Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending.”

Unfortunately, it didn’t work out that way.

Unintended Consequences

As with all things, there are always the unintended consequences which follow. For the vast majority ofAmericans:

- Housing did not become more affordable.

- Wall Street bought massive numbers of homes at distressed prices and went into the landlord business, which led to a rise in home prices.

- Many Americans, still recovering from the “Financial Crisis” were unable to obtain financing.

- For many others, affordability due to suppressed wage growth was the issue.

- Lower corporate bond rates didn’t lead to more investment, but rather increased share repurchases which benefited “C-Suite” executives at the expense of the working class.

Instead, as discussed previously, the Fed’s policies led to a growing divergence between the stock market and the economy. To wit:

“The one lesson that we have clearly learned since the 2008 “Great Financial Crisis,” is that monetary and fiscal policy interventions do not lead to increased levels of economic wealth or prosperity. What these programs have done, is act as a wealth transfer system from the bottom 90% to the top 10%.

Since 2008 there have been rising calls for socialistic policies such as universal basic incomes, increased social welfare, and even a two-time candidate for President who was a self-admitted socialist.

Such things would not occur if “prosperity” was flourishing within the economy. “

This is simply because the stock market is not the economy.

Stocks Are Not The Economy

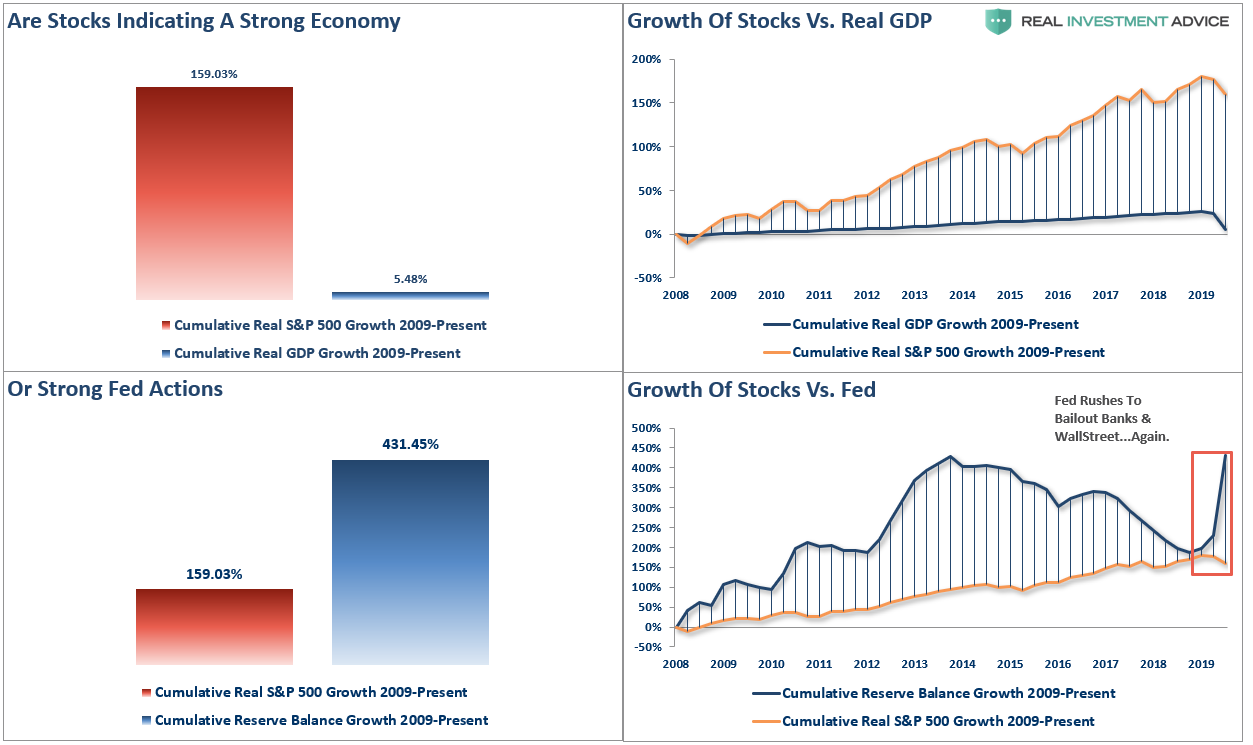

The Fed’s interventions and suppressed interest rates have continued to have the opposite effect of which was intended. I have shown the following chart below previously to illustrate this point.

From Jan 1st, 2009 through the end of March, the stock market rose by an astounding 159%, or roughly 14% annualized. With such a large gain in the financial markets, one would expect a commensurate growth rate in the economy.

After 3-massive Federal Reserve driven “Quantitative Easing” programs, a maturity extension program, bailouts of TARP, TGLP, TGLF, etc., HAMP, HARP, direct bailouts of Bear Stearns, AIG, GM, bank supports, etc., all of which totaled more than $33 Trillion, cumulative real economic growth was just 5.48%.

While monetary interventions are supposed to be supporting economic growth through increases in consumer confidence, the outcome has been quite different.

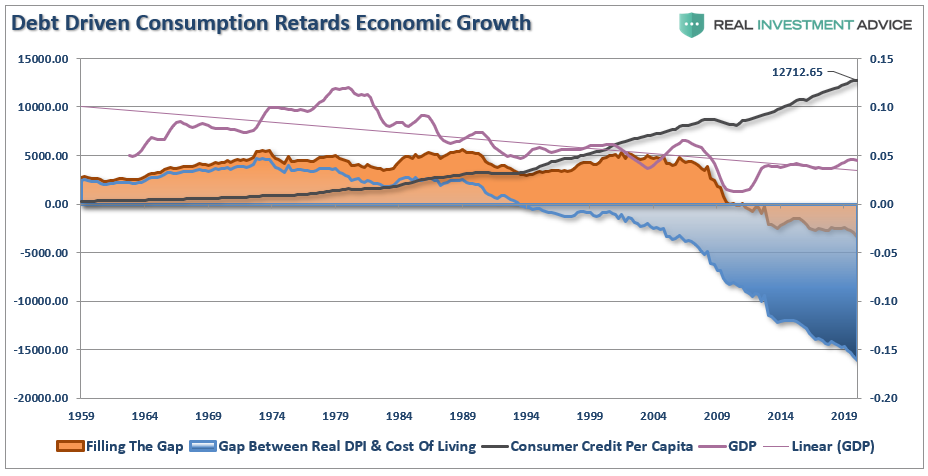

Low, to zero, interest rates have incentivized non-productive debt, and exacerbated the wealth gap. The massive increases in debt has actually harmed growth by diverting consumptive spending to debt service.

“The rise in debt, which in the last decade was used primarily to fill the gap between incomes and the cost of living, has contributed to the retardation of economic growth.”

Financial Shortcomings

The recent economic downtown caused by the pandemic has once again exposed the financial weakness that plagues the broader economy. Thereport by MagnifyMoney shows nearly 50% of Americans made changes to their plans within the first month of the pandemic for basic necessities.

What this tells you is that individuals could not survive more than ONE MONTH before tapping retirement savings. But what about the 50-60% of individuals that didn’t have a plan to start with?

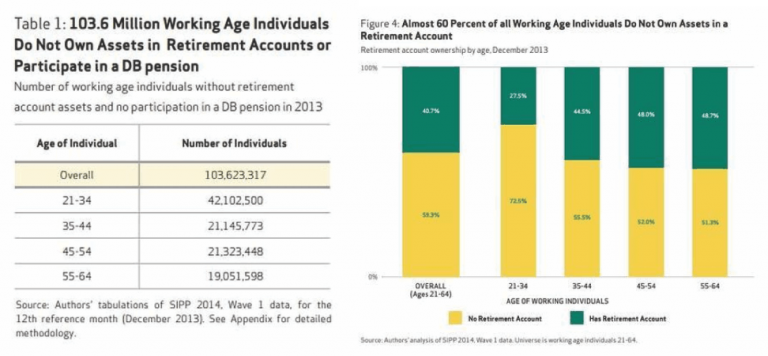

“A 2018 report from the non-profit National Institute on Retirement Security which found that nearly 60% of all working-age Americans do not own assets in a retirement account.”

Here are some findings from that report:

- Account ownership rates are closely correlated with income and wealth. More than 100 million working-age individuals (57 percent) do not own any retirement account assets, whether in an employer-sponsored 401(k)-type plan or an IRA nor are they covered by defined benefit (DB) pensions.

- The typical working-age American has no retirement savings. When all working individuals are included—not just individuals with retirement accounts—the median retirement account balance is $0 among all working individuals. Even among workers who have accumulated savings in retirement accounts, the typical worker had a modest account balance of $40,000.

- Three-fourths (77 percent) of Americans fall short of conservative retirement savings targets for their age and income based on working until age 67 even after counting an individual’s entire net worth—a generous measure of retirement savings.

Read those finding again.

If we use a more optimistic number of 50%, then 50% of American workers did not have the ability to tap additional “savings” to offset financial hardships during the pandemic.

It’s no wonder they are in the streets rioting.

Only The Few

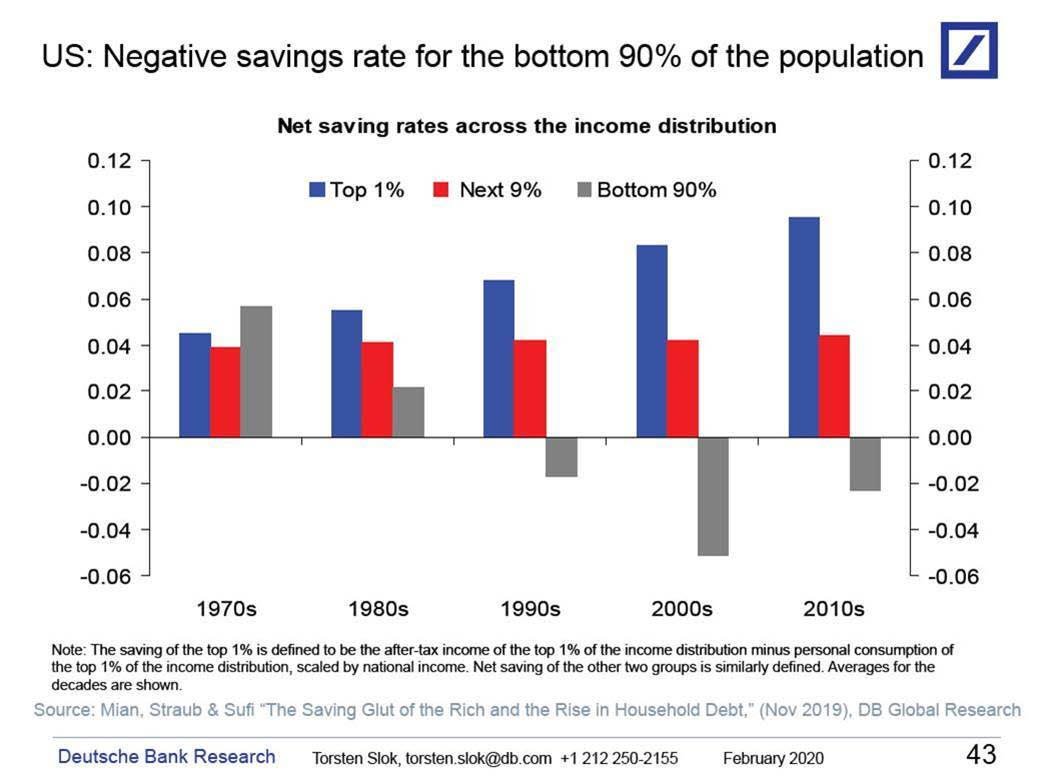

While the “savings rate” suggests that individuals are “hoarding money” due to the downturn, the reality is quite different. If American’s had savings they would not be tapping into 401k plans and begging for checks. However, Deutsche Bank recently showed the savings rate for 90% of Americans is negative.

This is far different than the Governmental statistics suggesting the average American is saving 33% of their income.

In actuality, if you aren’t in the “Top 20%” of income earners, you probably aren’t saving much, if any, money.

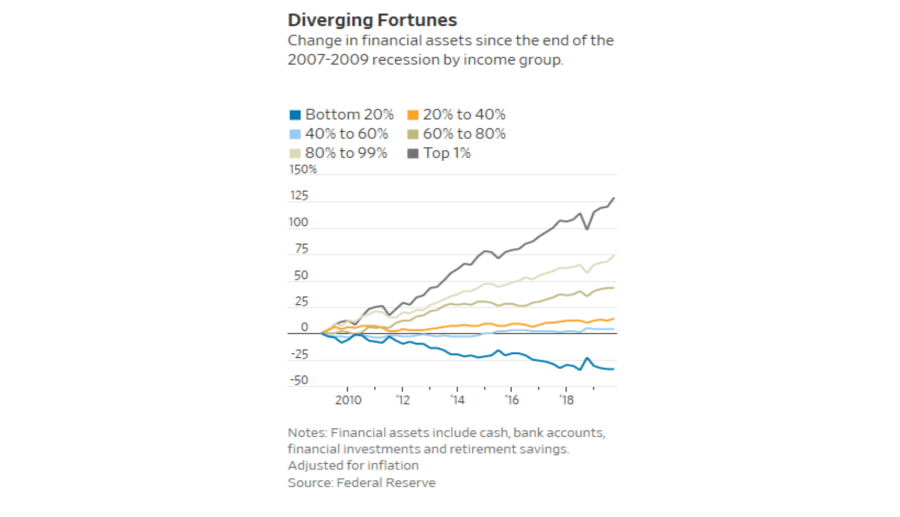

The problem for the Fed is their own policies are what created the “wealth gap” to begin with. As noted by the WSJ.

“As of December 2019—before the shutdowns—households in the bottom 20% of incomes had seen their financial assets, such as money in the bank, stock and bond investments or retirement funds, fall by 34% since the end of the 2007-09 recession, according to Fed data adjusted for inflation. Those in the middle of the income distribution have seen just 4% growth.” – WSJ

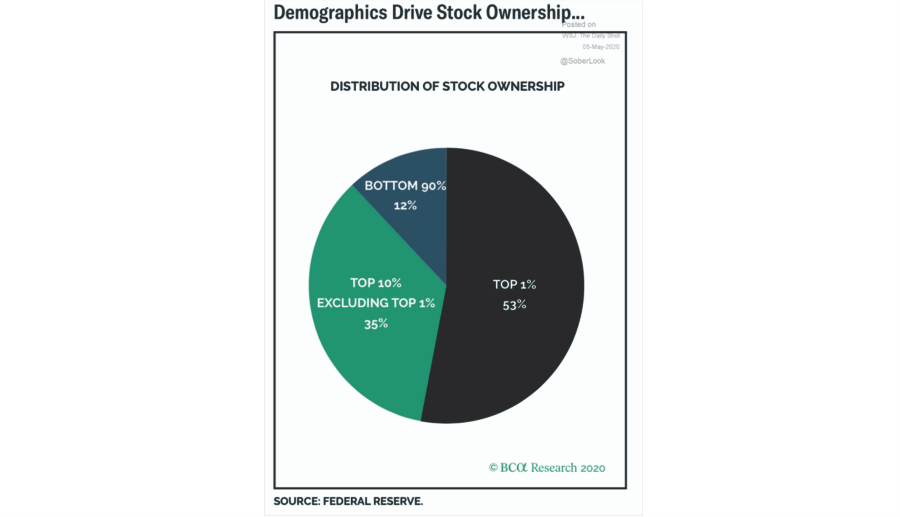

This isn’t surprising. A recent research report by BCA confirms one of the causes of the rising wealth gap in the U.S. The top-10% of income earners owns 88% of the stock market, while the bottom-90% owns just 12%.

The Fed Did It

The lack of economic improvement is clearly evident across all demographic classes. However, it has been the very policies of the Federal Reserve which created a wealth transfer mechanism from the poor to the rich. The ongoing interventions by the Federal Reserve propelled asset prices higher, but left the majority of American families behind.

The problem is the Fed has become trapped by its policies, and consequently, started taking direction from Wall Street. Such has led the Federal Reserve to become a “hostage” of its own making.

If the Fed removes any monetary accommodation, the market declines. The Fed is forced to subsequently increase support for the financial markets, which exacerbates the wealth gap.

It’s a virtual spiral from which the Fed can not extricate itself. It’s a great system if you are rich and have money invested. Not so much if you are any one else.

As we are witnessing, the United States is not immune to social disruptions. The source of these problems is compounding due to the public’s failure to appreciate “why” it is happening.

Eventually, as has repeatedly occurred throughout history, the riots will turn their focus toward those in power.

That, as they say, is when “s*** gets real.”

Comments

Log in or sign up to join the conversation.