UK is freaking out

- Andrew Bailey was like nope -. “My message to the funds involved and all the firms is you’ve got three days left now. You’ve got to get this done.” L you have three days

- its not going to QE this away, given the inflation situation.

- Markets did not like - stocks, gilts, even the 10Y all freaked out

- Because if they do go back to tightening that could mean that no pivot ever

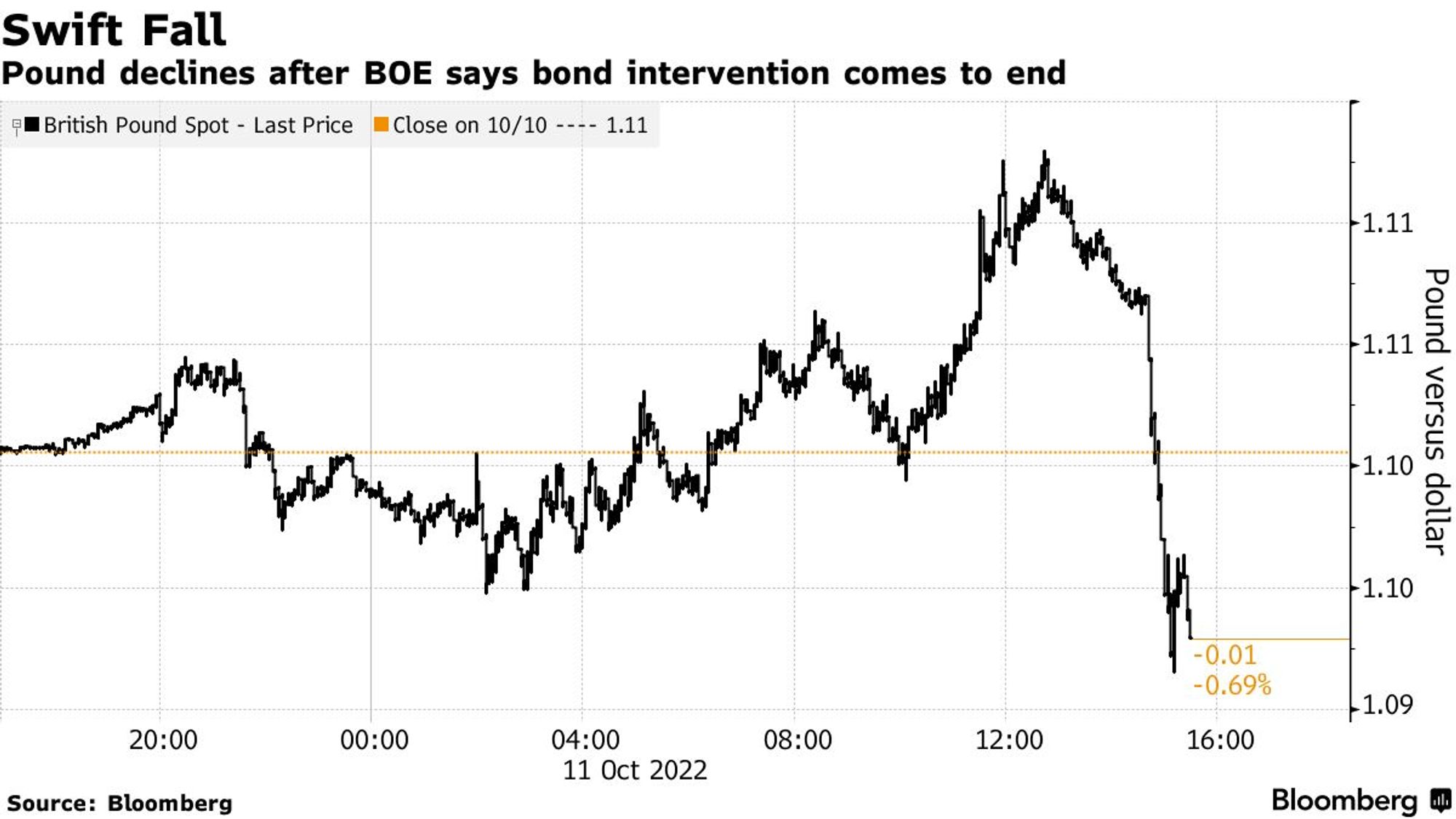

Bank of England Governor Andrew Bailey said that the central bank will halt intervention in the bond market as planned at the end of this week.

(Click on image to enlarge)

- Pension plans in late September saw a wave of margin calls after Prime Minister Liz Truss’s government announced large, debt-funded tax cuts that fueled an unprecedented bond-market selloff.

- The outsize moves in U.K. bond markets last month led to huge collateral calls on pensions to back up the leveraged investments. The pension funds have sold other assets, including government and corporate bonds, to meet those calls, adding to pressure on yields to rise and creating a spiral effect on markets.

- LDIs [use leveraged financial derivatives tied to interest rates to amplify returns] were at the root of the bond selloff that prompted the BOE’s original intervention

- The LDI issue that’s facing the market, the fact that the market is moving to the degree that it did, particularly yesterday, suggests that there’s still an awful lot [of selling] there

- The bank’s bond purchases, however, are meant to run out on Friday

- They had to buy more stuff: Policy makers have already been forced to expand the scope of emergency measures Tuesday to add inflation-linked debt to purchases in an effort to stop “fire sale dynamics.” While that initially sparked a rally in bonds, long-dated yields began rising again, following a record surge in real yields on Monday.

- If the market is already shifting yields aggressively higher with the BOE in the market on the buying side, how will the market deal with an active QT program, where a pre-defined size will have to be pushed into the market?

- Prior to the postponement of bond sales, officials had repeatedly stressed that there would be a high bar for delaying the start, with only “very distressed” market conditions warranting a change of plan. It could argue those terms have been met.

- If the market is already shifting yields aggressively higher with the BOE in the market on the buying side, how will the market deal with an active QT program, where a pre-defined size will have to be pushed into the market?

- But no one wants to sell: Pensions have also appeared hesitant to sell their bonds to the BOE, reflecting a mismatch in what the central bank is offering and what the market needs. The way that the bank has structured this intervention is they can only buy assets if people put offers into them, but nobody is putting offers in

- If they sell gilts now, they’re doing it in the likelihood that they’ll need to buy them back in the future at some point and they might be more expensive

- Old Fellas: Pension funds are traditionally slow-moving organizations that make decisions with multidecade horizons. The market turmoil has hurtled them into the warp-speed-style moves usually reserved for traders at swashbuckling hedge funds.

- The bond sales are meant to start on Oct. 31, the same day that Chancellor of the Exchequer Kwasi Kwarteng is set to release a medium-term fiscal plan

- But with the fixed income rout this year the losses are mounting. The Fed alone has a mark-to-market loss of $720bn

Video Length: 00:05:23

More By This Author:

The US Dollar Is A Tipping Domino

Does The Fed Want More People To Be Unemployed?

Credit Suisse: Great Financial Crisis 2.0?

Comments

Log in or sign up to join the conversation.