A week ago, the BLS revised lower the number of employed persons by nearly 900,000. Given that revision and a slew of recent revisions in other economic statistics, we must ask if GDP is also overstated. GDP, like other data, has a history of sharp revisions. For instance, consider the following research from the San Francisco Fed:

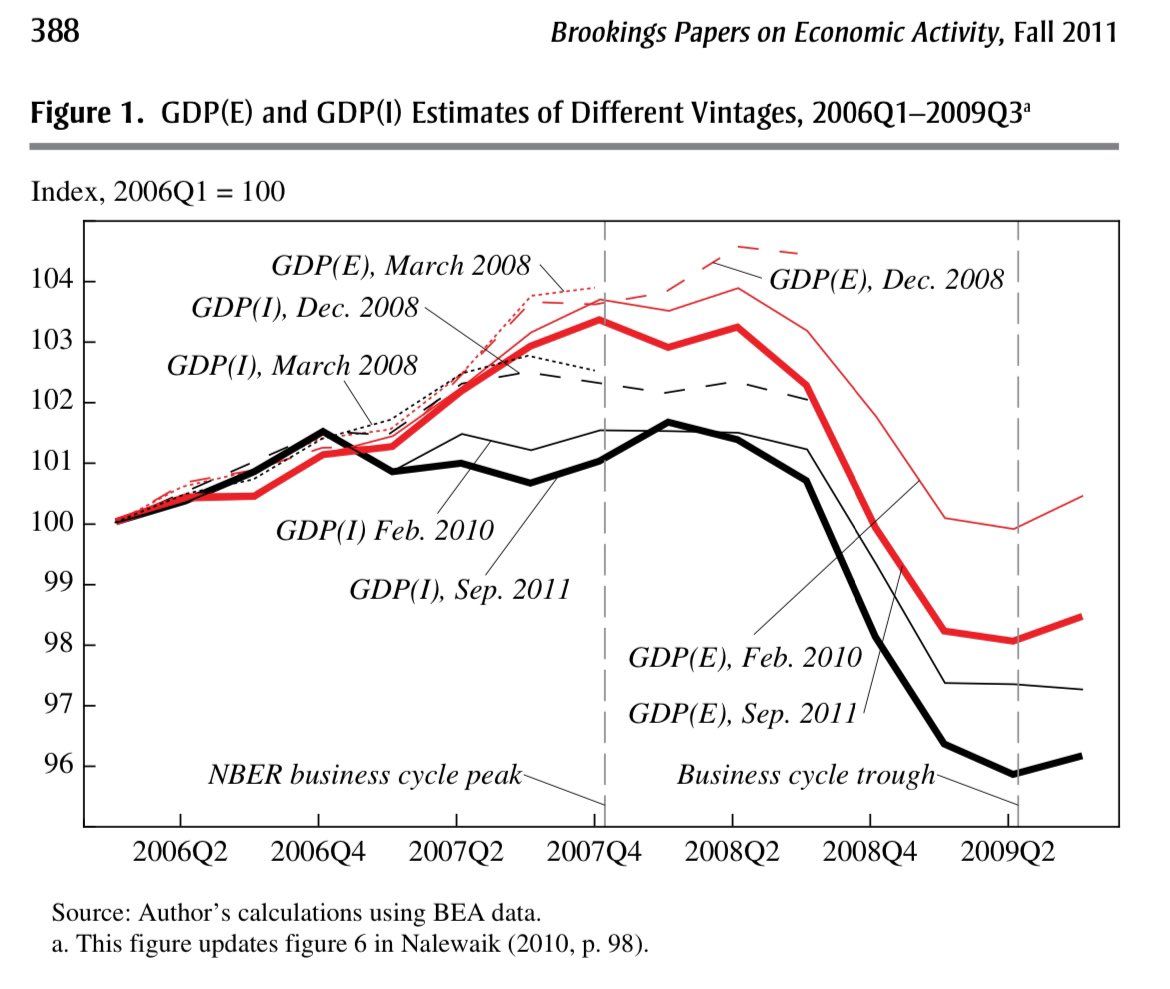

The figure shows that the decline in real GDP growth initially seemed far less serious than it turned out to be. In fact, for the first half of 2008, the data would have been consistent with only a relatively mild recession. But by the fourth quarter of 2008, the quarterly contraction was initially listed at –3.8% annual rate. With the passing of time, the data were revised down another whopping –4.6 percentage points, thus bringing the decline in GDP to an eye-watering –8.4% annual rate.

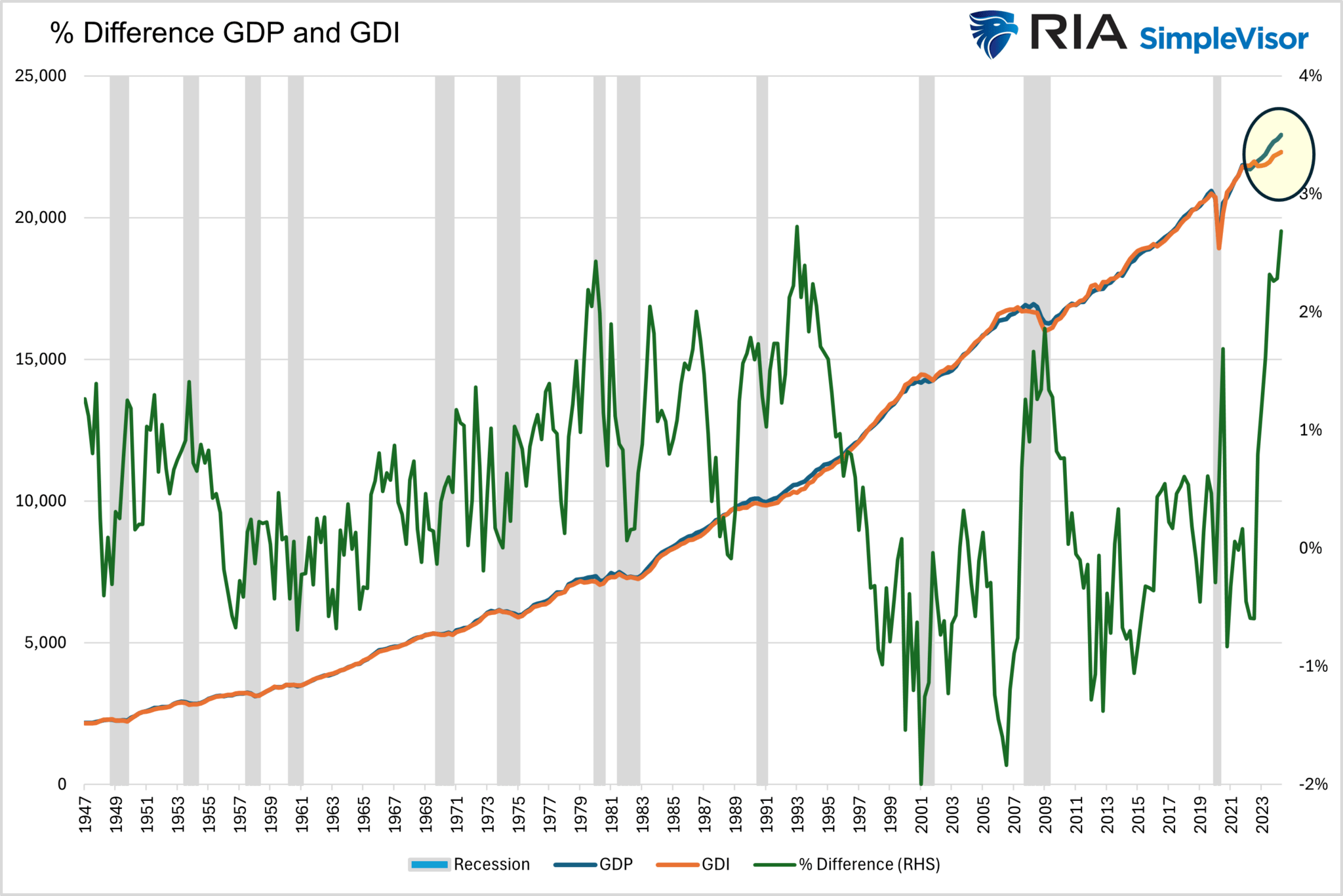

To help us appreciate if it is overstated and potentially by how much we turn to GDI. Gross Domestic Product (GDP) and Gross Domestic Income (GDI) are two very similar measures of economic activity. The difference is that GDP measures output, while GDI assesses income. These measures should tell the same economic story. However, GDI has proven to be more reliable and often leads GDP.

Hence, if the relationship normalizes, a downward revision is likely. Currently, the difference between GDP and GDI is $615 billion. Therefore, if a revision or even a normalization were to occur, GDP would decrease by 2.7%. We have more on the GDP-GDI relationship in a section below.

(Click on image to enlarge)

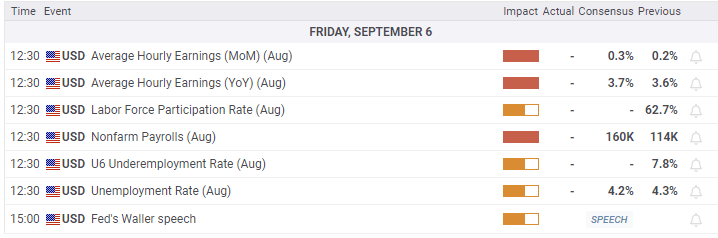

What To Watch Today

Earnings

- No notable earnings releases today

Economy

(Click on image to enlarge)

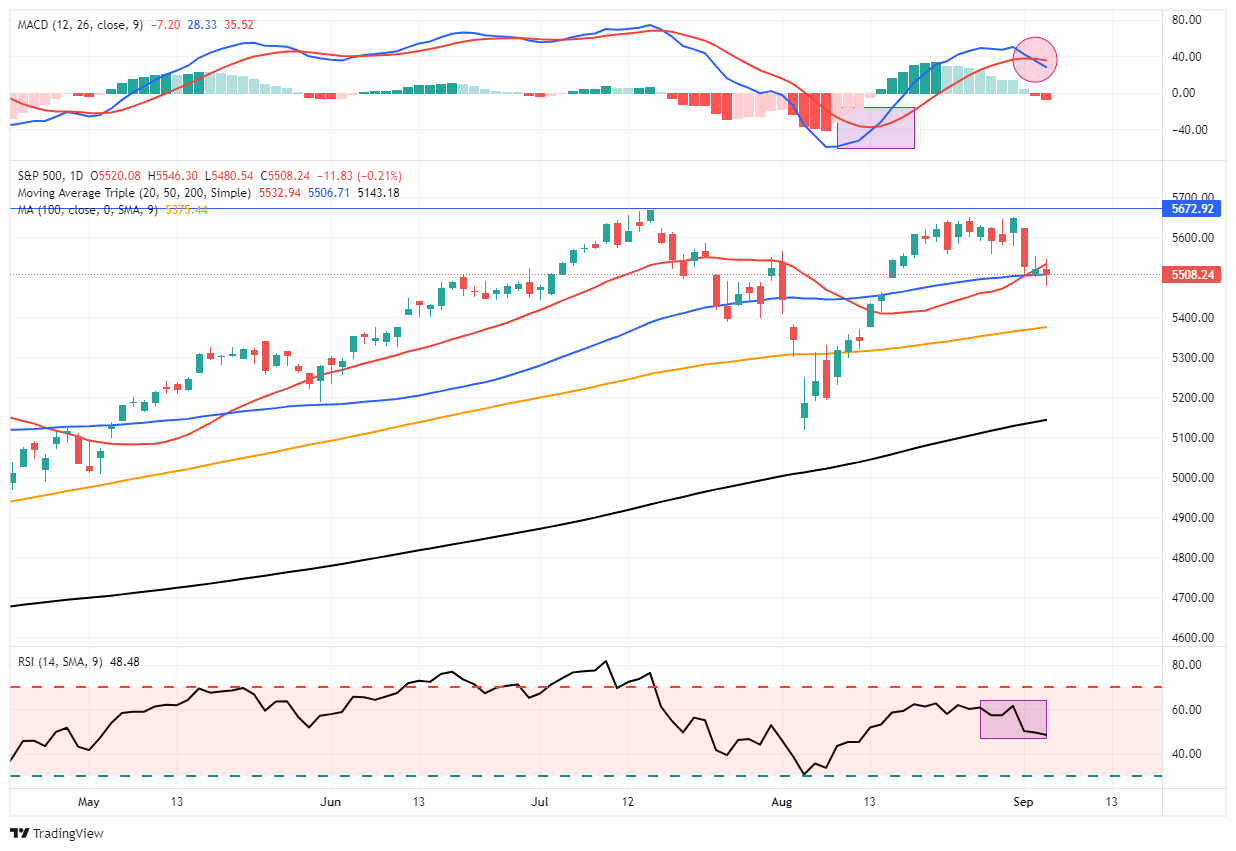

Market Trading Update

Yesterday, we discussed that the market was testing initial support at the 50-DMA. The market flirted with breaking that initial level of support as the sell signal deepened. However, there are two important points to consider before taking action. First, when the market moves down to previous support levels, it generally coincides with short-term oversold conditions. Secondly, the initial break isn’t validated until a failed retest of that broken support.

While the market is not deeply oversold, the selling pressure has generated enough stress to elicit a short-term bounce. Such could be the case if the employment report this morning keeps Fed rate cut expectations on the table. Secondly, look for a bounce before reducing risk. As is often the case, investors tend to make knee-jerk reactions that lead to poor outcomes when markets sell-off.

This morning’s employment report will likely decide the market’s fate over the next few trading days. A too-strong report will send interest rates higher and stocks lower as expectations for Fed rate cuts get pushed out. The opposite will likely be the case if the report is exceptionally weak. After the employment report, we should know better where the market goes next.

(Click on image to enlarge)

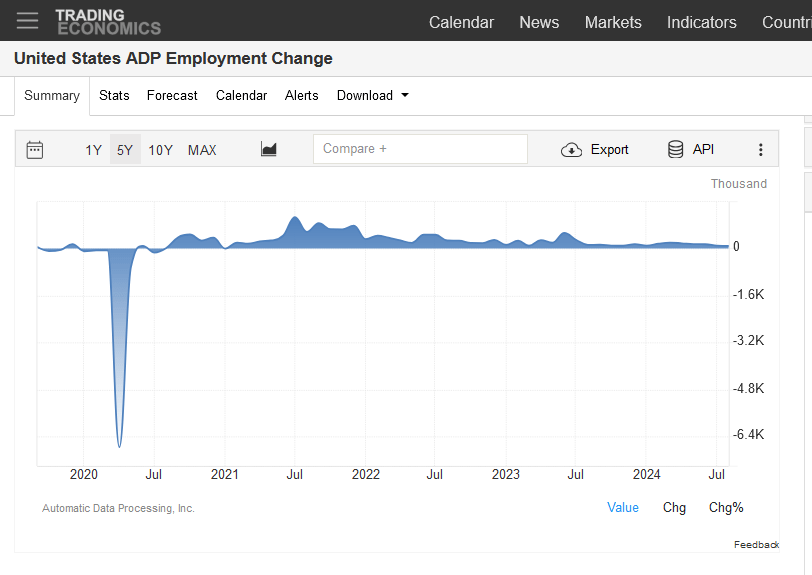

ADP Jobs Report

We share the commentary below from ADP to help us set expectations for today’s BLS jobs report.

Private businesses in the US added 99K workers to their payrolls in August 2024, the least since January 2021, following a downwardly revised 111K in July and well below forecasts of 145K. Figures showed the labor market continued to cool for the fifth straight month while wage growth was stable.”The job market’s downward drift brought us to slower-than-normal hiring after two years of outsized growth,” said Nela Richardson, chief economist, ADP. “The next indicator to watch is wage growth, which is stabilizing after a dramatic post-pandemic slowdown”. Year-over-year, pay gains were flat in August, remaining at 4.8 percent for job-stayers and 7.3 percent for job-changers.

It is important to note that the ADP and the BLS employment reports have not been in sync since the pandemic. Therefore, take the data below and the commentary above with a grain of salt.

(Click on image to enlarge)

More On GDP GDI And Labor Market Revisions

The following is from Anna Wong, Chief Economist Bloomberg.

There is this myth that GDI always get revised toward GDP. It is a myth, because turns out that GDI leads GDP in turning points of the economy (per BEA and Fed research). And GDP tends to get revised toward GDI in lead up to and during recessions…though obvious only several years later. The discrepancy is GDP and GDI also turns out to be predictive of unemployment rate in the lead up to cyclical peaks.

Bottomline: why do I have to spend my Friday night writing about this rather reading a nice book? I’d rather not. But people on this app put too much signal on GDP, particularly in today’s economic environment. Research would say to put more weight on GDI in turning points.

The chart below accompanies a Fed article by Jeremy Newaik. As shown, the initial 2008 GDP readings were revised sharply lower over the following few years.

(Click on image to enlarge)

Tweet of the Day

(Click on image to enlarge)

More By This Author:

The Treasury Yield Curve Sets Off A Recession Warning

Risks Facing Bullish Investors As September Begins

Long-Term Signals Suggest Lower Forward Returns

Comments

Log in or sign up to join the conversation.