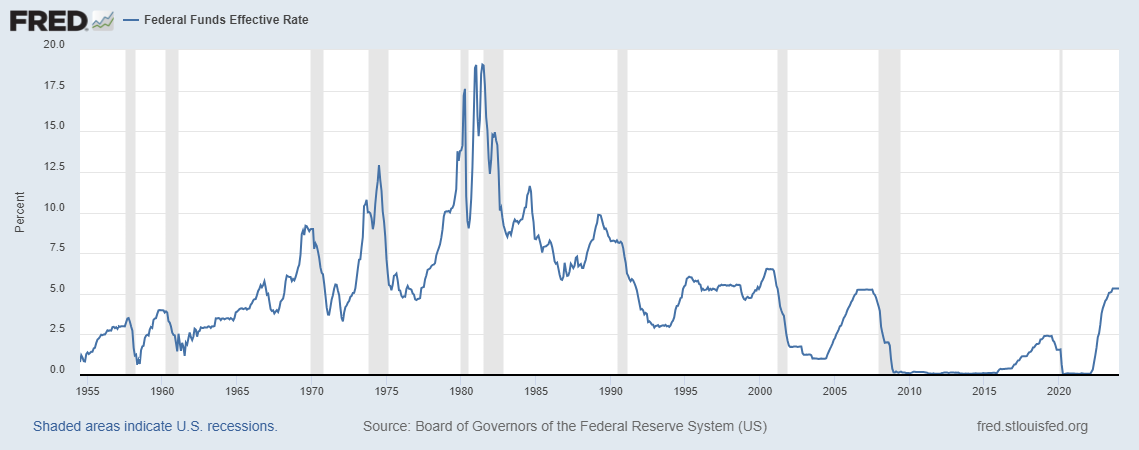

Reader Bruce Hall notes the correlation between Fed funds rate peaks and recessions, as a counterpoint to my use of spread inversions.

(Click on image to enlarge)

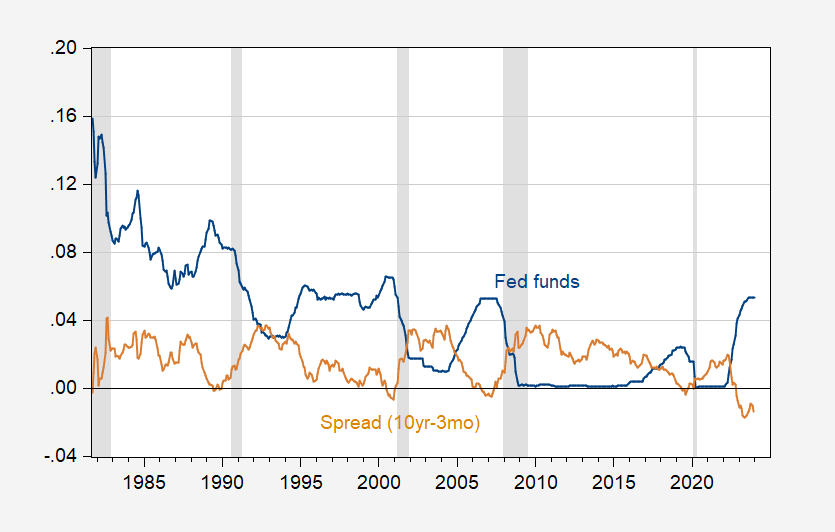

Let’s compare peaks to inversions:

Figure 1: Fed funds (blue), and 10yr-3mo Treasury spread (tan). NBER defined peak-to-trough recession dates shaded gray. Source: Treasury, Fed via FRED, NBER.

Inversions and peaks precede recessions. Which one does better as a single predictor? I assess using a standard probit regression.

Figure 2: Probit regression on recession lead by 12 months on Fed funds (blue), and on 10yr-3mo Treasury spread (tan). NBER defined peak-to-trough recession dates shaded gray. Source: NBER, and author’s calculations.

The probit regression on the Fed funds has a pseudo-R2 of 0.07, while that on the spread has a pseudo-R2 of 0.27.

For my part, I’ll stick to the spread.

More By This Author:

Other Metrics For Evaluating Recession Onset And The “Technical Recession” Of 2022H1Recessions Defined And (Maybe) Predicted

Exchange Rate Pass Through Into Import Prices, CPI

Comments

Log in or sign up to join the conversation.