The surge in corporate debt in 2019 has now become a major concern regarding financial stability, according to a recent report by the IMF[1]. Corporations have issued a record $2.4 trillion in new debt throughout the developed economies in 2019. Investors, desperate for higher yields, have willingly embraced the corporate debt market and have pushed valuations to levels now considered to be highly vulnerable to external shocks. Over the course of the last 12 months, the steady decline in long term yields have compelled insurance companies, pension funds, and other institutional investors to reach out and invest in riskier and less liquid securities. The IMF report argues that the corporate debt levels represent significant risks to the financial stability in the developed countries. It warns that 40% of all corporate debt in the major economies should be classified “at-risk” in the event of a major down global downturn and “exceeding levels seen during the 2008-9 financial crisis”.

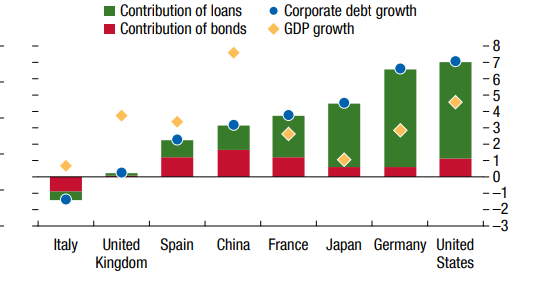

To put this debt accumulation into context, corporate debt issuances grew faster than GDP over the last 12 month period ending in the first quarter of 2019. (Figure 1). That fact that debt accumulation exceeded economic growth, begs the question just how was the debt deployed. If it were to add to business capital investment, then we would anticipate that the GDP would have grown faster in response to the stimulative effects of the additions to capital stock.

Figure 1 Growth in Corporate Debt (percent 2019Q1/2018Q1)

(Click on image to enlarge)

Source: IMF

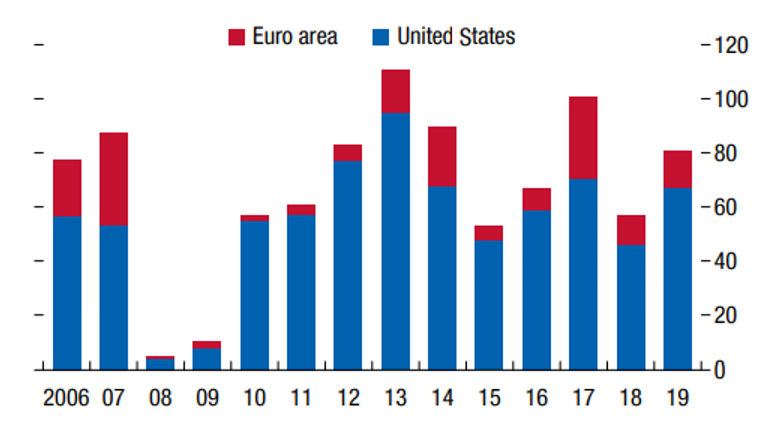

Instead, corporations used their newly acquired borrowed capital to reward shareholders with a combination of higher dividends and share buybacks, one of the most important factors accounting for the strong growth in equities since the 2008 crisis. As the economy weakens, more debt is downgraded , as the so-called “fallen angels” precipitate a bond crisis due to forced selling. Most recently, Dallas Federal Reserve President, Robert Kaplan expressed his worry that any further downgrades could lead to a very rapid widening in credit spreads and an equally rapid tightening in financial conditions. There need not be a recession, per se, to set off this crisis because the sheer volume of debt issued is very top-heavy with low-quality credit.

Figure 2 HY Bonds and Leveraged Loans Used for Shareholder Distribution ($billions)

(Click on image to enlarge)

Source: IMF

The IMF concludes by drawing particular attention to the rapid growth in the risky leveraged loan and private credit segments. This debt is funded by “nonbank financial institutions that are highly exposed to corporate paper, leveraged loans, private credit, and SME loans that would be susceptible to losses in an adverse scenario, possibly amplifying the magnitude of the downturn by cutting back.” Right now, investors are caught up in the euphoria of a strong equity markets as the year comes to a close. The IMF presents evidence that should greatly temper that excitement as the credit markets become ever more strained under the weight of corporate debt in an economy that may no longer be able to support those debt levels.

Comments

Log in or sign up to join the conversation.