After last week saw The Fed's balance sheet continue is decline back from its bank-bailout resurgence, all eyes will be back on H.4.1. report this evening to see if things have continued to 'improve' or re-worsened amid regional bank shares re-testing post-SVB amid earnings disappointments.

Following the unexpected OUTFLOW the previous week, this week saw money market funds resume their trend with a $53.8 billion INFLOW...

Source: Bloomberg

The breakdown was $48.9 billion from Institutional funds and $4.98 billion from retail funds.

That pushed assets back up near their $5.277 trillion record high and suggests last week's deposit OUTFLOWS may be about to re-accelerate - not good news for banks?

Source: Bloomberg

On top of the news from First Republic this week, one could argue that Round 2 of the banking crisis (bank superwalk as Jim Bianco has put it) is just beginning.

Bear in mind though that it's tax-time and their are some odd seasonal impacts to the data.

Though not wanting to piss all over those hopeful fireworks, we note that reverse repo continues to rise...

Source: Bloomberg

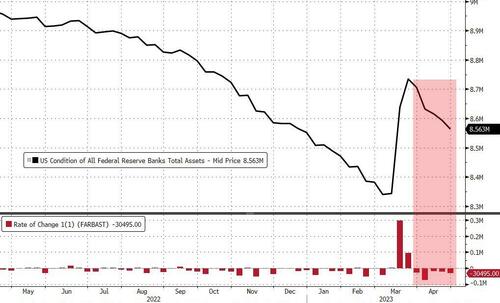

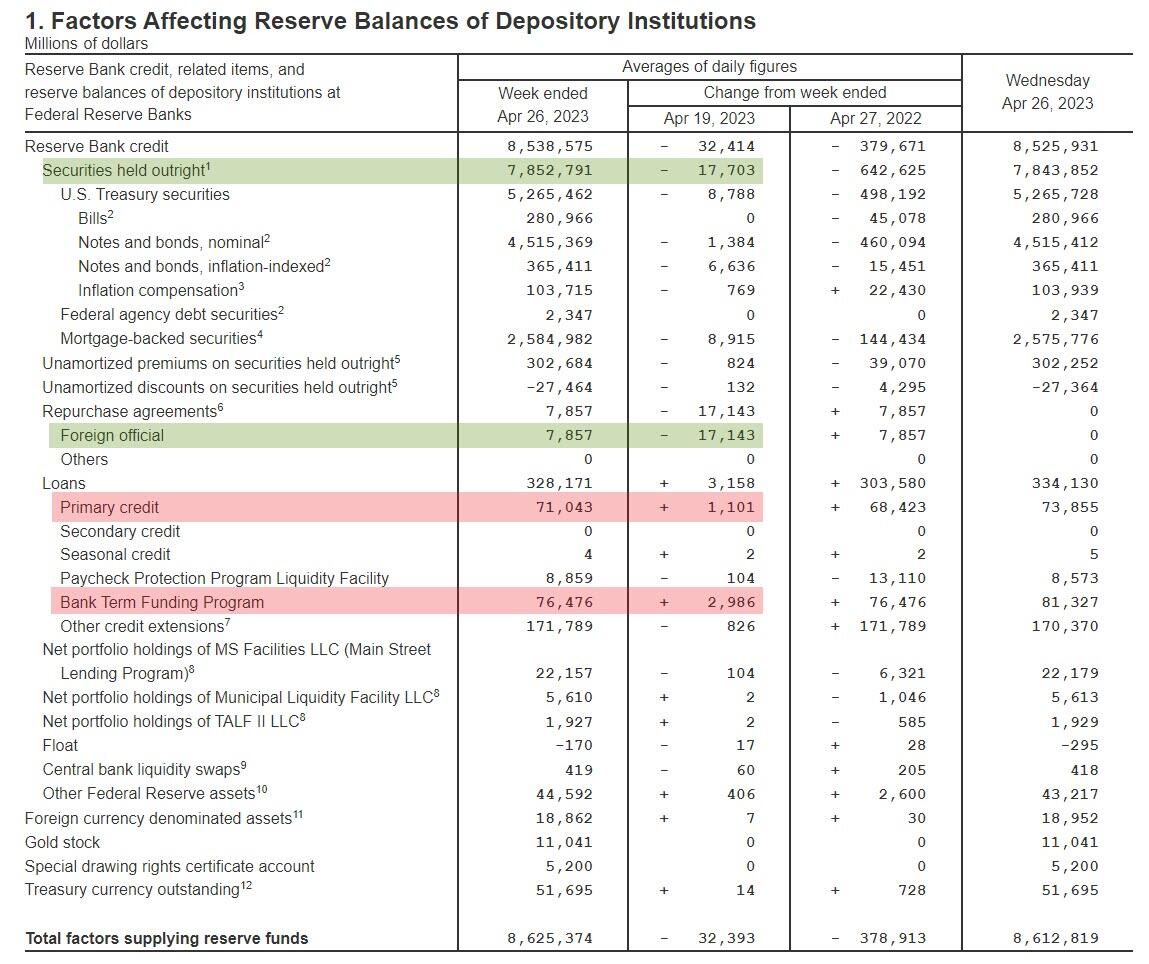

However, the most anticipated financial update of the week - the infamous H.4.1. showed the world's most important balance sheet shrank for the 5th straight week last week, by $30.5 billion, notably more than last week's tumble (helped by a $16.6bn QT)...

Source: Bloomberg

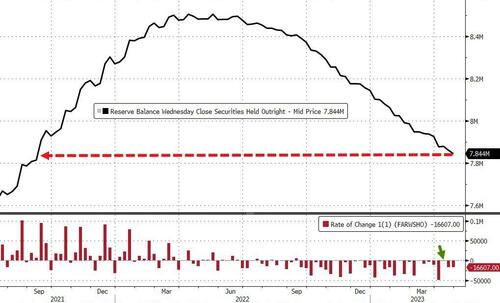

The Total Securities held outright on The Fed balance sheet fell to $7.84 trillion, the lowest since Sept 2021...

Source: Bloomberg

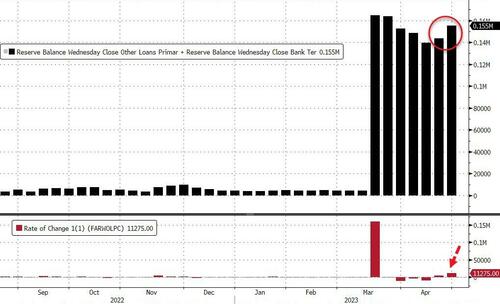

Looking at the actual reserve components that were provided by the Fed, we find that Fed backstopped facility borrowings ROSE AGAIN last week from $144 billion to $155.2 billion (still massively higher than the $4.5 billion pre-SVB)...

Source: Bloomberg

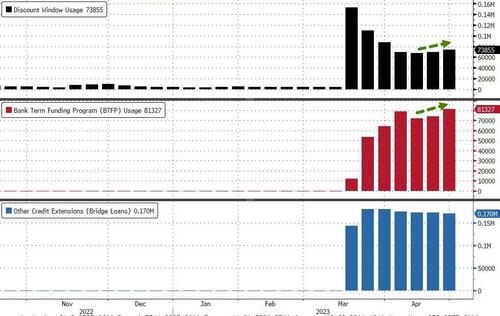

...but the composition shifted, as usage of the Discount Window rose by $4 billion to $73.8 billion (upper pane below) along with an $8 billion increase in usage of the Fed's brand new Bank Term Funding Program, or BTFP, to $81.3 billion (middle pane) from $79.0 billion last week. Meanwhile, other credit extensions - consisting of Fed loans to bridge banks established by the FDIC to resolve SVB and Signature Bank were relatively unchanged at around $170BN (lower pane)...

Source: Bloomberg

Scanning down the H.4.1, we note that Foreign repo was down $17BN to around $8BN (though it is still troubling that some bank still needs this much USD) and Other Fed Assets rose $2.2 billion (after falling last month)...

(Click on image to enlarge)

Of course, we get to see the actual deposit outflows (or inflows) tomorrow after the bell, but it appears the hopeful bounce was nothing more than the tax-related seasonal we warned about last week.

More By This Author:

Amazon Soars After Smashing Expectations, Guiding Higher

Amazon Earnings Preview: Here Are The Main Things To Look For

Stagflation: Q1 GDP Much Weaker Than Expected On Inventory Plunge As Inflation Comes In Red Hot

Comments

Log in or sign up to join the conversation.