As mentioned in several of my reports within the department store space, I have highlighted the challenges faced by the sector as well as liquidity analysis to identify the survival of the retailers in the Post-COVID world. Several of the retailers have started reporting their Q1 results which were albeit unsurprisingly worse and have had initiated coverage on DDS with SELL rating, We focus on Kohl's in this initiating coverage report focusing on the near term challenges and the long term sustainability of the company.

Q1 2020 Results

The company reported a decline of 41% in total revenue in line with many of the other retailers which were forced to shut down amidst the coronavirus pandemic. Digital sales, however, showed some promise having grown 24% in the quarter. Gross margin witnesses a steep decline from 36.8% to 17.3% on YoY basis due to permanent markdowns in the inventory across significantly lower sales due to COVID-19 coupled with higher shipping cost with an increase in digital sales and unfavorable product mix. While SG&A expenses declined 19.5% YoY on an absolute basis excluding COVID-19 expenses as the company furloughed most of its 85,000 associates as the company shuttered their stores, as a proportion of sales SG&A expenses spiked up from 33% in the year-ago period to ~49% on the current period. The company has sufficient liquidity and balance sheet strength comprising $2bn in cash and $500mn in a revolver facility with maturities coming only until 2023. It also suspended its dividend program and cut back its capex investments by $500 mn in the CY2020 cutting down technology spends as well as an additional fulfillment center.

Strategic Highlights

The company has 90% of the stores in off-mall neighborhood locations which would lead to higher digital sales due to proximity as well as increased consumer comfort regarding safety and precautions which could have a sentimental impact on the footfalls. It also reduced its quarterly receipts by 30% which implies a 3% reduction over the corresponding period a year ago, as a response to the weakening sales and created a special reserve of inventory. Management is cautious and expects to double down the reduction to 60% in the coming quarter, to boost financial flexibility. The company is focussing on driving digital penetration and expect to have higher shipping and fulfillment cost which is likely to pressure margins in the near term. During the 2008 crisis, KSS dropped 39% from the peak levels of $40 to sub-$25 levels compared to S&P decline of 51% in the corresponding period. However, it recovered sharply post hitting the bottom gaining 53% in the subsequent months. In the current time, however, there is a different story as the stock has fallen almost 70% YTD compared to S&P gain of ~5% which highlights the unique challenges that the departmental stores continue to face. Will the company be able to strive through a shift in consumer tastes, rising unemployment, looming recession, and increasing competition from online retailers?

Valuation

The company mentioned the current gross margins are likely to continue in the coming quarter and we expect margins to further dip due to increased digital penetration leading to higher shipping costs along with the discounted inventory. We expect a decline of 26% in revenue growth in the next quarter boosted by a 50% growth in digital sales, as we believe, digital sales would continue to drive the growth as consumers adjust to the new-normal. We expect sales degrowth to ease significantly in the second half and expect the company to post an adjusted loss per share of $11.9. Assuming the tax losses are carry forwarded so that the company does not pay any tax in 2021.

| Q1 2020 | Q2 2020 | Q3 2020 | Q4 2020 | Q1 2021 | Q2 2021 | Q3 2021 | Q4 2021 | |

| Store Revenue | 1,165.0 | 1,584.2 | 2,649.7 | 4,222.9 | 1,514.5 | 2,138.7 | 3,312.1 | 5,067.5 |

| Digital Revenue | 995.0 | 1,500.8 | 1,307.4 | 1,961.1 | 1,194.0 | 1,801.0 | 1,568.9 | 1,961.1 |

| Total Revenue | 2,160.0 | 3,085.1 | 3,957.1 | 6,184.0 | 2,708.5 | 3,939.7 | 4,881.0 | 7,028.6 |

| Growth | (43%) | (26%) | (9%) | (5%) | 25% | 28% | 23% | 14% |

| Gross Profit | 373.0 | 509.0 | 870.6 | 1,484.2 | 812.6 | 1,339.5 | 1,757.1 | 2,249.1 |

| Gross Margin | 17.3% | 16.5% | 22.0% | 24.0% | 30.0% | 34.0% | 36.0% | 32.0% |

| SG&A | (1,066.0) | (1,079.8) | (1,187.1) | (1,669.7) | (758.4) | (1,181.9) | (1,513.1) | (2,178.9) |

| D&A | (227.0) | (227.0) | (227.0) | (227.0) | (227.0) | (227.0) | (227.0) | (227.0) |

| Other Revenue | 268.0 | 187.6 | 206.4 | 227.0 | 249.7 | 274.7 | 302.1 | 332.3 |

| Impairment | (66.0) | - | - | - | - | - | - | - |

| EBIT | (718.0) | (610.1) | (337.2) | (185.5) | 76.9 | 205.3 | 319.2 | 175.6 |

| Interest expense | 58.0 | 58.0 | 58.0 | 58.0 | 58.0 | 58.0 | 58.0 | 58.0 |

| PBT | (776.0) | (668.1) | (395.2) | (243.5) | 18.9 | 147.3 | 261.2 | 117.6 |

| Tax | (235.0) | - | - | - | - | - | - | - |

| PAT | (541.0) | (668.1) | (395.2) | (243.5) | 18.9 | 147.3 | 261.2 | 117.6 |

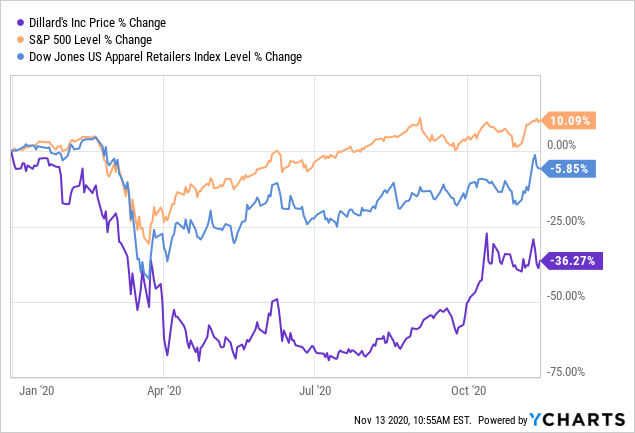

Data by YCharts

We expect the company to recover the lost sales in the subsequent year and expect the company to post FY21E EPS of $3.50. KSS has traded at an average 1Y Fwd. P/E multiple of 10x. And we apply a 7x PE multiple and assign a value of $24.5 per share. We believe KSS is one of the best-positioned brands among the departmental stores and expect them to benefit from the weakness of the other players. Risks to rating would primarily be the commentary in the 2H 2020 and any second wave of coronavirus shutdown.

Comments

Log in or sign up to join the conversation.