Image Source: Pixabay

A steep uptick in U.S. bond yields alarmed investors ahead of important inflation data that may affect the rate of Federal Reserve policy easing, which caused Asian equities to fall on Wednesday. As the market reopened following the Veterans Day holiday, short-term Treasury rates surged overnight to their highest level since late July, pushing the U.S. dollar to a three-month high against the yen in the most recent session. Since Donald Trump was reelected to the White House last week, bond rates have risen on the belief that higher tariffs and lower taxes will boost government borrowing and the fiscal deficit. Markets also believe that Trump's suggested policies will increase inflation and possibly obstruct the Fed's efforts to cut interest rates. All of this is still a part of the Trump trade, which is fundamentally about increasing deficit spending. The battle between stocks and bonds eventually shifts market sentiment, though, as higher risk-free rates limit valuations, as has been demonstrated in previous market booms, with the Trump trade poster child Bitcoin retreating frm a test of 90k overnight, although many market participants view this pause as one that will refresh upside momentum. The forecast for China, a major customer that will be hardest hit by Trump's promised trade tariffs, caused commodities to decline generally. Beijing's stimulus initiatives have not inspired much hope for an economic recovery thus far. Both Hong Kong's Hang Seng and a subindex of mainland Chinese real estate equities fell more than 1%. The blue chips from China were flat. Both South Korea's Kospi and Japan's Nikkei saw declines.

The main macro driver today will likely be US CPI; core will likely remain at 3.3% year over year, while headline rate is anticipated to increase 0.2 percentage points to 2.6%. Similar to yesterday's UK data, which showed that it counted for less this time since the outlook had changed due to the Budget, this week's typically important US data release will also reveal nothing about the future after a Trump election victory based on October inflation figures. Even though subsequent changes in political decisions must be given more weight in the outlook, this extremely near-term data may still have some influence on the December Fed decision. It is generally anticipated that the headline rate for the October CPI release would increase from 2.4% year over year to 2.6% year over year. This comes after worries over the Middle East scenario caused energy prices to rise in the earlier part of the month. Given that this increase was only temporary, any October inflation bump could be reversed in November. An upside surprise here could raise more doubts about the likelihood of a rate drop in December, as the core rate is generally predicted to remain at 3.3% year over year. Disinflation has been fuelled by the core basket's regularly fluctuating prices; the "stickier" price components continue to exhibit more obstinate inflation rates.

Overnight Newswire Updates of Note

- Softbank To Get First New Nvidia Chips For Japan Supercomputer

- China Taps Global Bankers For Feedback To Lift Confidence

- Trump’s Cabinet Picks Signal Tougher Stance On China

- Global Markets Reel As Trump’s America First Agenda Unfolds

- Templeton Joins JPM, T. Rowe In 5% Treasury Yield Forecast

- Fed Policy Is 'Modestly Restrictive,' Kashkari Says

- US CPI Unlikely To Provide Fed With Greater Confidence

- Tariff Test For EU As Trump Prepares To Squeeze Trade Partners

- ECB’s Rehn: More Cuts Coming But Pace Of Easing Uncertain

- German Govt Collapse Could Have Silver Lining For EU Markets

- German ZEW Falls Unexpectedly Amid Political Upheaval

(Sourced from reliable financial news outlets)

FX Options Expiries For 10am New York Cut

(1BLN+ represents larger expiries, more magnetic when trading within daily ATR)

- EUR/USD: 1.0600 (1.8BLN), 1.0625 (1.1BLN), 1.0665-75 (818M)

- 1.0725 (2.3BLN), 1.0740-50 (3.3BLN)

- USD/CHF: 0.8750 (654M), 0.8800 (843M)

- GBP/USD: 1.2780-85 (310M), 1.3000 (411M). EUR/GBP: 0.8300 (301M)

- AUD/USD: 0.6500 (238M), 0.6600-05 (277M), 0.6650 (479M)

- USD/CAD: 1.3900 (515M)

- USD/JPY: 153.50-65 (585M), 154.35-50 (444M), 155.00 (1.1BLN)

- AUD/JPY: 100.00 (245M), 100.45 (279M), 101.00 (290M)

CFTC Data As Of 8/11/24

- USD net spec G10 long -$0.31bn

- EUR +1.04% in period; specs +26.7k contracts now -21.7k

- JPY -1.19%; specs sell 19.4k contracts now -44.2k; US-JP rate divergence

- GBP +0.2%; specs sell 21.3k contracts long cut to 45.1k

- CAD -0.63%; specs sell 7.7k contracts; BoC rate well below Fed in 2025

- AUD +1.14%; specs +3.5k contracts now +31k; RBA seen as more hawkish c.bank

- BTC -4.37% in period; specs +412 contracts, now -1,457

- Equity fund speculators trim S&P 500 CME net short position by 97,351 contracts to 194,685

- Equity fund managers cut S&P 500 CME net long position by 52,438 contracts to 992,952

- Speculators trim CBOT US 10-year Treasury futures net short position by 82,913 contracts to 818,270

Technical & Trade Views

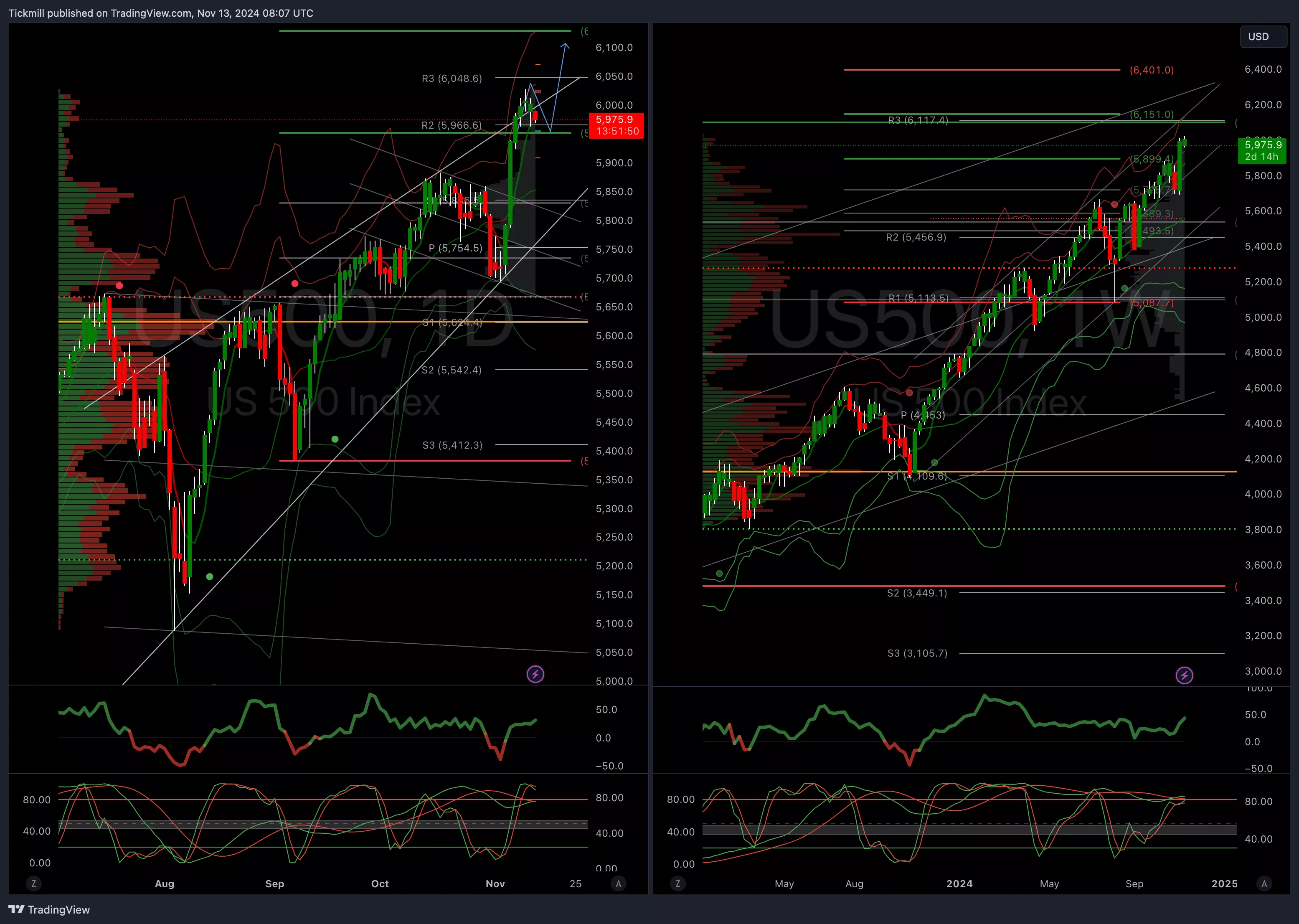

SP500 Bullish Above Bearish Below 5960

- Daily VWAP bullish

- Weekly VWAP bullish

- Below 5550 opens 5820

- Primary support 5800

- Primary objective 6100

(Click on image to enlarge)

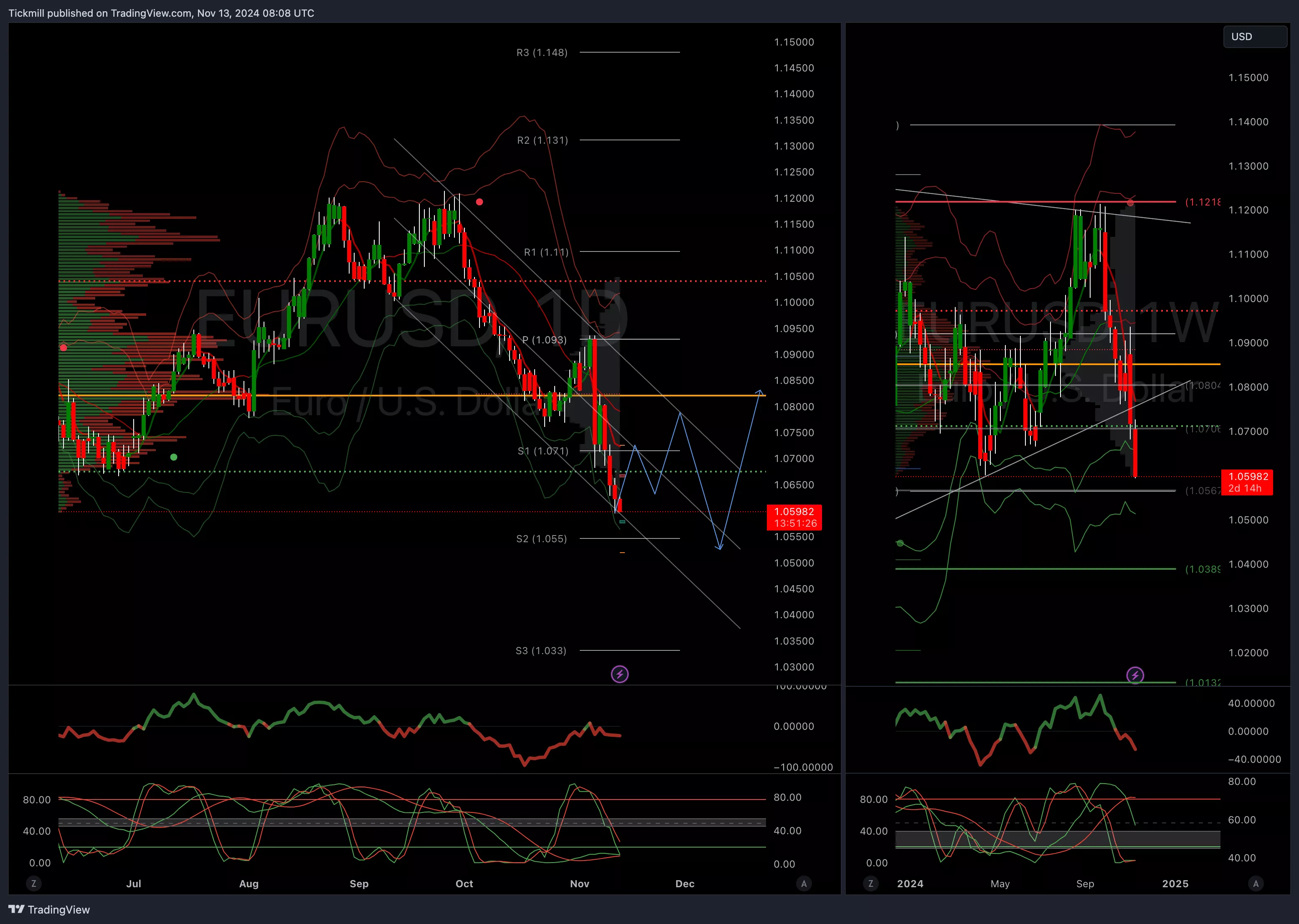

EURUSD Bullish Above Bearish Below 1.0810

- Daily VWAP bearish

- Weekly VWAP bearish

- Above 1.09 opens 1.0950

- Primary resistance 1.0950

- Primary objective 1.06 - TARGET HIT NEW PATTERN EMERGING

(Click on image to enlarge)

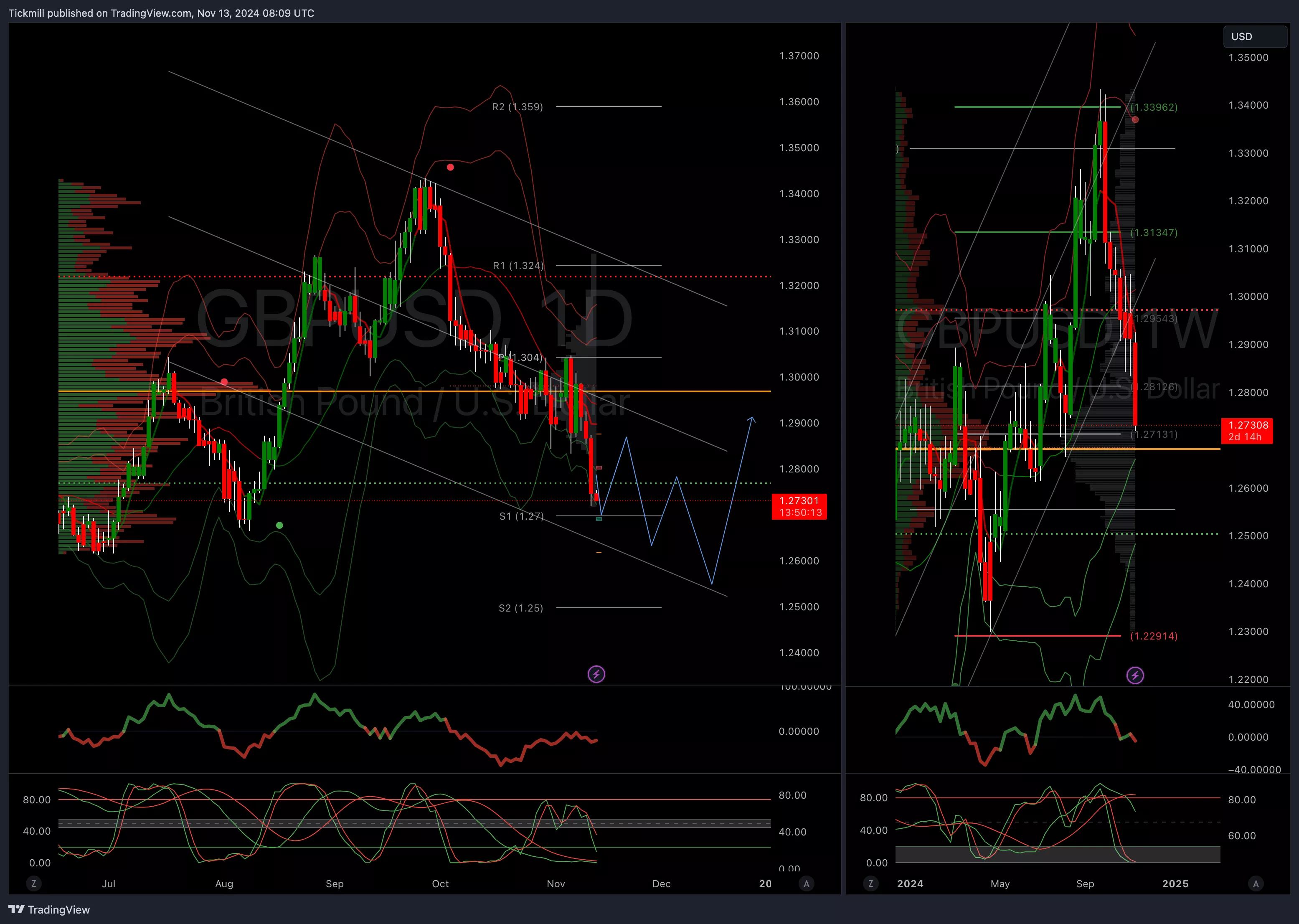

GBPUSD Bullish Above Bearish Below 1.3050

- Daily VWAP bearish

- Weekly VWAP bearish

- Below 1.29 opens 1.27

- Primary resistance 1.3050

- Primary objective 1.27

(Click on image to enlarge)

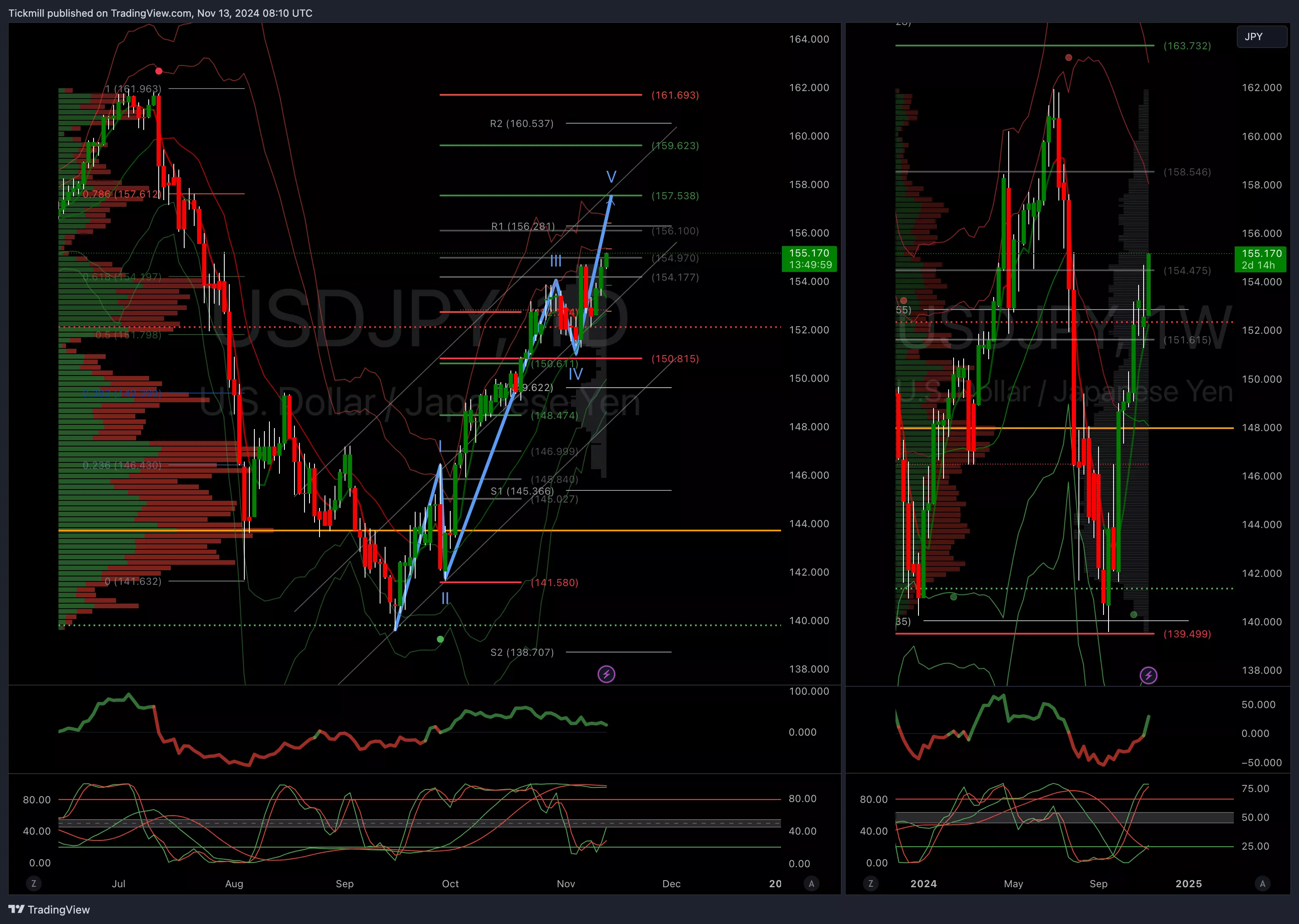

USDJPY Bullish Above Bearish Below 152.30

- Daily VWAP bullish

- Weekly VWAP bullish

- Below 152 opens 150.80

- Primary support 148

- Primary objective is 157.50

(Click on image to enlarge)

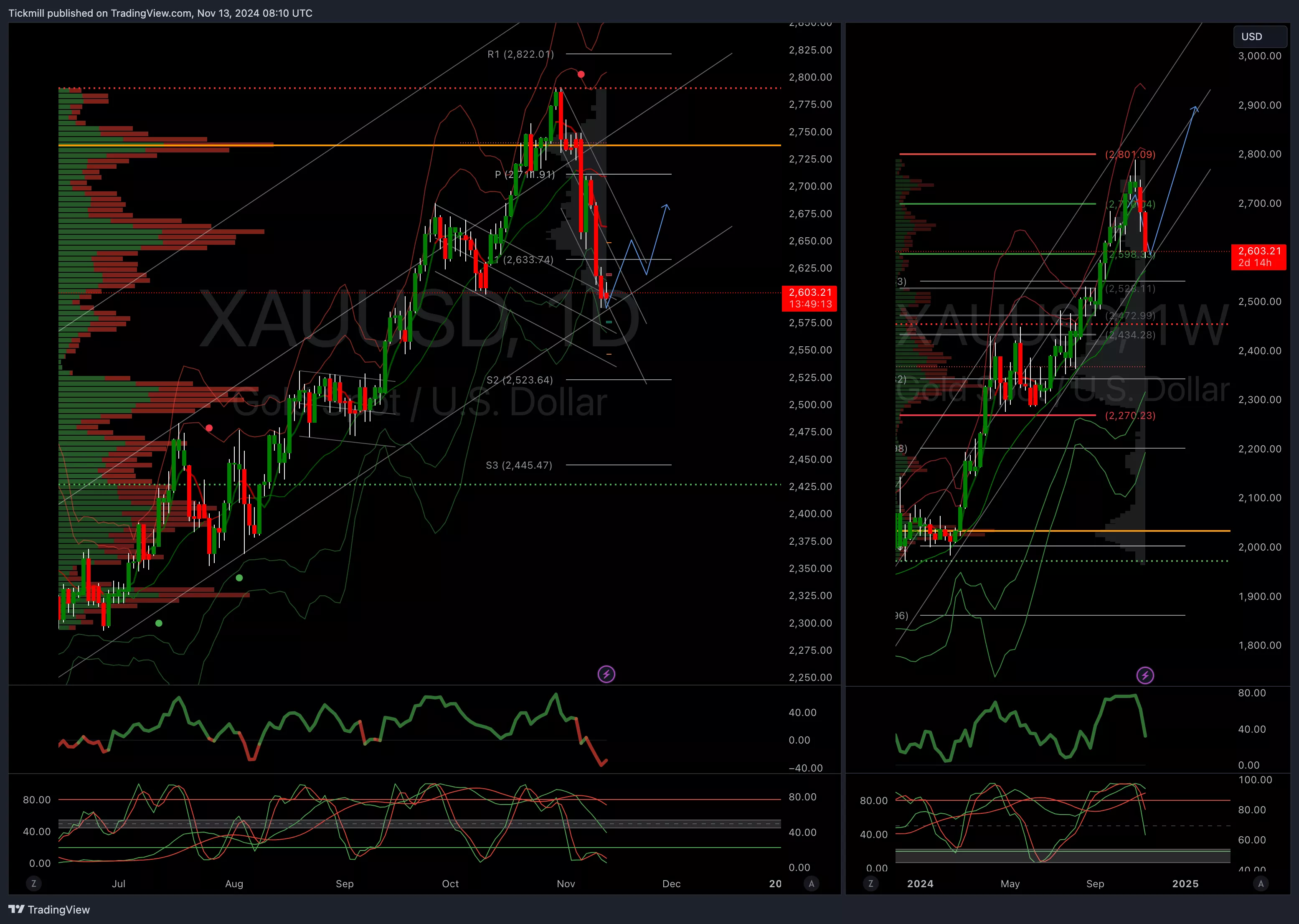

XAUUSD Bullish Above Bearish Below 2600

- Daily VWAP bearish

- Weekly VWAP bearish

- Below 2590 opens 2530

- Primary support 2600

- Primary objective is 2800

(Click on image to enlarge)

BTCUSD Bullish Above Bearish Below 84500

- Daily VWAP bullish

- Weekly VWAP bullish

- Below 84000 opens 80000

- Primary support is 64000

- Primary objective is 100,000

(Click on image to enlarge)

.webp)

More By This Author:

FTSE Falls Again After Yesterday’s Dead Cat Bounce

Daily Market Outlook - Tuesday, Nov. 12

FTSE Snaps Four Day Losing Streak, Jobs Data Eyed

Comments

Log in or sign up to join the conversation.