Daily Market Outlook - Wednesday, April 2

Image Source: Pexels

Asian stocks edged lower as investors recalibrated their risk exposure ahead of President Donald Trump’s anticipated tariff announcement. Regional indices declined in Japan and South Korea, while Hong Kong experienced minor fluctuations, hovering near the flatline. Treasury yields climbed after a recent dip, reflecting market speculation on potential Federal Reserve easing. Trump has already enacted tariffs on aluminium, steel, and automobiles while raising duties on all imports from China. The action has unsettled markets as worries grow that a full-scale trade conflict could lead to a significant downturn in the global economy. During these unpredictable times, gold prices have surged, reaching a record high of over $3,000 per ounce. The yellow metal has risen 19% this year, following a 27% increase in 2024, marking its best annual performance in over a decade.

Market uncertainty has been prevalent as President Trump prepares to unveil changes to trade policy. Reports suggest that adjustments to import tariffs remain under discussion, with varying options regarding their scope and specific rates still on the table. The announcement is scheduled for 9 PM BST from the Rose Garden at the White House, leaving market participants more time to speculate on the details. Those anticipating a definitive resolution to the ambiguity may face disappointment. Reflecting this uncertainty, Trump’s press secretary remarked that the President is "always open to a good negotiation," hinting at the possibility of bilateral talks to refine tariff rates in the coming days, weeks, or even months. Market expectations have recently shifted toward the possibility of broader tariffs, raising the prospect of a short-lived relief rally if the measures announced are less severe than feared. Nonetheless, such optimism may be fleeting, given the prolonged uncertainty and potential economic disruption. Regardless of today's announcement, short-term economic indicators are likely to remain under pressure as rising costs and unpredictability weigh on growth. This was underscored yesterday when the March Manufacturing ISM survey fell below the critical 50 mark, signalling contraction. New orders dropped sharply (from 48.6 to 45.2), while prices paid surged (from 62.4 to 69.4), highlighting the challenges ahead.

In the Eurozone the ECB's hawkish contingent has been vocal in opposing an April rate cut, citing uncertainties in tariffs, global trade, defence spending, and Germany’s eased debt rules. However, these are potential risks, not certainties. Eurozone inflation shows improvement, with slower wage growth and declining price trends. March data reveals headline HICP at 2.2% (down from 2.3%) and core inflation at 2.4% (down from 2.6%), below expectations. Service prices hit a 35-month low at 3.4% year-on-year, while manufacturing remains in a 33-month contraction. With restrictive monetary policy and economic weakness, a pause in April seems unlikely.

Overnight Newswire Updates of Note

- Fed’s Goolsbee Warns Of Tariff-induced Pullback In Spending

- Investors Flock To Gold Funds As Fears Over Trump Tariffs Mount

- Option Traders Bet On Treasuries Rallying More On Trump’s Trade War

- Bayer Targets 2025 Launch Of Two Drugs With $1B+ Potential

- Visa Offers Apple $100M To Take Over Credit Card From Mastercard

- SoftBank Leads OpenAI's Funding Round Amid Rise Of DeepSeek

- Japan's FTC To Regulate Google And Apple Under New Smartphone Law

- BoJ’s Ueda: US Tariffs Could Have Big Impact On Global Trade

- Goldman Cuts FY25 Forecast For 10Y JGB Yield On US Recession Risk

- Goldman Picks Yen As Top Hedge Against US Recession, Tariff Risk

- Japan DPP: BoJ Hike In May Would Be Too Early Given Tariffs, Wages

- China Urges State-Owned Automakers To Merge With Aims To Boost EVs

- Chinese Megabanks’ Interest Margins Fall Lows As Economy Slows

- Aussie Labour Push Above-Inflation Wage Rise Despite RBA Warning

(Sourced from reliable financial news outlets)

FX Options Expiries For 10am New York Cut

(1BLN+ represents larger expiries, more magnetic when trading within daily ATR)

- EUR/USD: 1.0700 (1.4BLN), 1.0750 (644M), 1.0770-80 (490M), 1.0785 (278M)

- 1.0790-1.0800 (5BLN), 1.0825 (418M), 1.0850 (903M), 1.0885-95 (1BLN)

- 1.0900-10 (677M), 1.0920-25 (1.5BLN)

- EUR/GBP: 0.8345-55 (328M), 0.8500 (301M)

- GBP/USD: 1.2875 (247M), 1.3050 (200M), 1.3160 (395M)

- AUD/USD: 0.6220-30 (563M), 0.6250 (521M). NZD/USD: 0.5775 (376M)

- USD/CAD: 1.4210 (555M), 1.4400-10 (700M)

- USD/JPY: 149.00 (510M), 149.80 (308M), 149.95-150.05 (545M)

- 150.20-30 (653M). EUR/JPY: 161.20 (821M)

CFTC Data As Of 28/3/25

- Equity fund managers have increased their S&P 500 CME net long position by 83,572 contracts, bringing the total to 915,841. Meanwhile, equity fund speculators have raised their S&P 500 CME net short position by 41,376 contracts, now totalling 236,867. Speculators have also expanded their CBOT

- US Treasury bonds futures net short position by 24,765 contracts to reach 38,275. Additionally, they have reduced their CBOT US Ultrabond Treasury futures net short position by 14,792 contracts, now at 232,366. The CBOT US 10-year Treasury futures net short position has been trimmed by 71,284 contracts, bringing it to 810,090. Speculators have reduced their CBOT US 5-year Treasury futures net short position by 5,853 contracts to total 1,900,087, and the CBOT US 2-year Treasury futures net short position has been cut by 38,970 contracts, now standing at 1,181,586.

- The Japanese yen holds a net long position of 125,376 contracts, while the Swiss franc reports a net short position of -37,593. The British pound has a net long position of 44,283 contracts, and Bitcoin holds a net long position of 1,179 contracts.

Technical & Trade Views

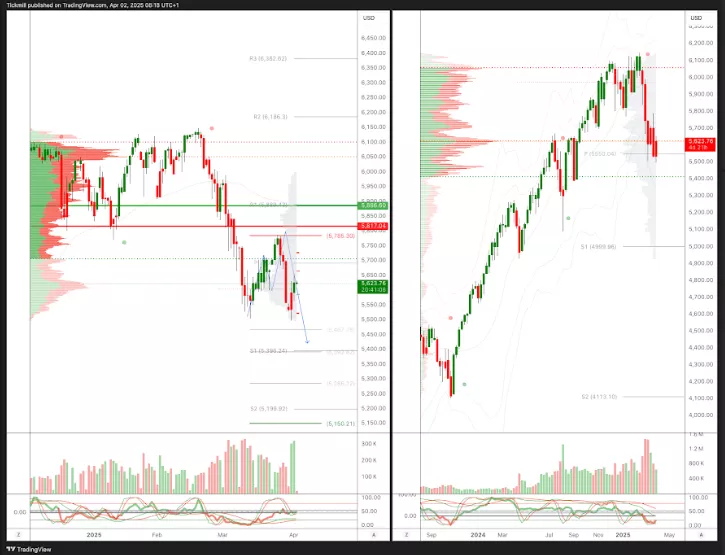

SP500 Pivot 5790

- Daily VWAP bullish

- Weekly VWAP bearish

- Seasonality suggests bullishness into late April

- Above 5885 target 5950

- Below 5815 target 5415

(Click on image to enlarge)

EURUSD Pivot 1.0750

- Daily VWAP bearish

- Weekly VWAP bullish

- Seasonality suggests bearishness into the end of April

- Above 1.0750 target 1.11

- Below 1.0690 target 1.0550

(Click on image to enlarge)

GBPUSD Pivot 1.28

- Daily VWAP bearish

- Weekly VWAP bullish

- Seasonality suggests bullishness into late April

- Above 1.2850 target 1.32

- Below 1.2790 target 1.2660

(Click on image to enlarge)

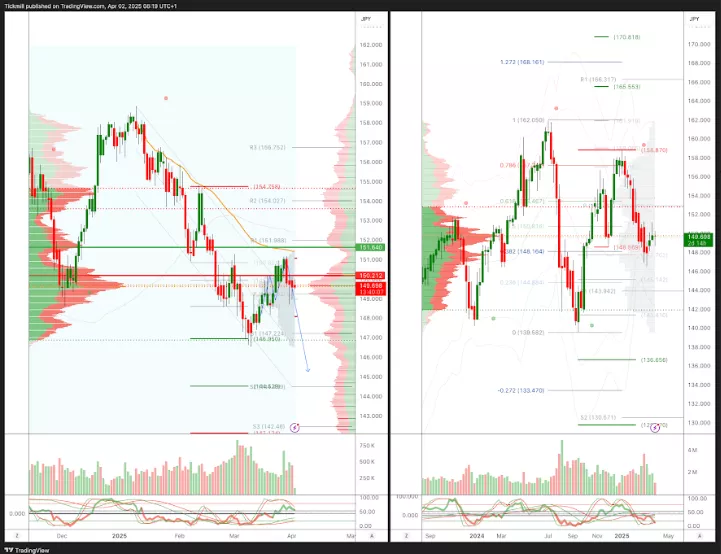

USDJPY Pivot 150.50

- Daily VWAP bearish

- Weekly VWAP bullish

- Seasonality suggests bullishness into Apr 9th

- Above 1.52 target 153.80

- Below 150.50 target 145

(Click on image to enlarge)

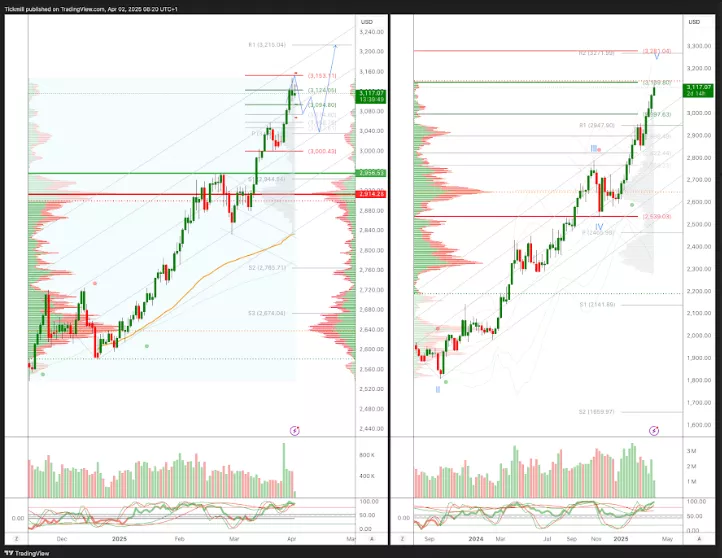

XAUUSD Pivot 2950

- Daily VWAP bullish

- Weekly VWAP bullish

- Seasonality suggests bearishness into mid/late April

- Above 2900 target 3100

- Below 2880 target 2835

(Click on image to enlarge)

BTCUSD Pivot 90k

- Daily VWAP bullish

- Weekly VWAP bearish

- Seasonality suggests bullishness into Apr 9th

- Above 97k target 105k

- Below 95k target 65k

(Click on image to enlarge)

More By This Author:

The FTSE Finish Line - Tuesday, April 1

Daily Market Outlook - Tuesday, Apr. 1

The FTSE Finish Line - Monday, March 31