Image Source: Unsplash

Asian stocks reached their highest levels in a month, fuelled by hopes that Trump might ease the effects of his auto tariffs, which could lead to a reduction in trade tensions. The regional MSCI index saw a 0.4% increase, and S&P 500 futures also rose after a White House official stated that imported vehicles would be exempt from extra tariffs on aluminium and steel. Hyundai was at the forefront of gains among South Korean car manufacturers. The Dollar index climbed by 0.2%, while gold prices dropped by as much as 1.1%. A Japanese holiday has led to no Treasury trading during Asian hours, following a rally in the US session that reduced the 10-year yield to 4.21% from a peak of 4.30%. This occurred despite the Treasury announcing an increase in borrowing for the current quarter to $514 billion, up from the previous estimate of $123 billion. The holiday has also closed some equity markets, but where trading has occurred, many indices are modestly positive, reflecting US stock performance. The period of relative calm continues in the post-Liberation Day context. Supporting this trend, the Wall Street Journal reports that Trump plans to ease automotive tariffs. In foreign exchange, the Dollar index is advancing as the London session opens, returning to Monday’s end-of-day level. The Canadian Dollar initially rose on news of Carney's general election win but reversed the gain to trade unchanged overnight, as the victory was narrow and required a coalition. Spain's grid operator reported that power has been almost fully restored overnight following yesterday’s blackout, mitigating potential market ripple effects today. Reports on US job openings and consumer confidence are providing market focus for the US session ahead.

Today marks the final day of the fifteen-day period during which the Bank of England (BoE) observes financial market variables to inform the Monetary Policy Committee (MPC) projections for the May Monetary Policy Report (MPR). Typically, the focus is on changes in the market-implied path of the Bank Rate compared to the previous period and its impact on the central projection for the Consumer Price Index (CPI). Notably, since February, there has been a significant shift: the Bank Rate is now anticipated to be approximately 50 basis points lower two years from now than projected in the last MPR. This more stimulative outlook generally suggests upward pressure on the new May MPR projection for CPI. However, other factors are at play. The exchange rate has strengthened by about 2%, which, in isolation, might not seem significant, especially compared to January when fiscal concerns were affecting the GBP. Yet, this increase positions the trade-weighted exchange rate near its post-referendum peak. Additionally, the rise in the Cable since Liberation Day contradicts the typical expectation that a country imposing tariffs would see its exchange rate strengthen. Consequently, given the MPC's increased emphasis on the exchange rate, the stronger level suggests a potential for a slightly more dovish narrative in May, as import prices benefit from disinflationary effects, aiding in controlling the overall CPI profile.

Overnight Newswire Updates of Note

- PM Carney’s Liberals Win Canada Election, Setting Up Talks With US

- Trump To Soften Blow Of Automotive Tariffs

- Trump Floats Improbable Income-Tax Cut Tied To Tariffs

- Macron Urges Trump To Take a Firmer Line With Putin Over Ukraine

- UK Food Inflation Hit 11-month High In April, Industry Data Shows

- Gold Slips As Traders Await US Data For Clues On Tariff Impacts

- US Steelmaker Nucor Tops Quarterly Estimates On Higher Spot Prices

- NXP Semi Sink On Tariff Concerns, CEO Kurt Sievers To Step Down

- Boeing Removed From Credit Watch By S&P In Turnaround Boost

- ADB Head: Tariff War Shows Asian Nations Need New Trade Partners

- New Zealand To Tighten Budget Belt As US Tariffs Threaten Growth

- RBA’s Kent Highlights Recent ‘Sharp Rise’ In Aussie Volatility

- Japan Worries Trump Tariffs Will Push Countries Toward China

- Chinese Carmakers Reset European Ambitions As EU Tariffs Bite

(Sourced from reliable financial news outlets)

FX Options Expiries For 10am New York Cut

(1BLN+ represents larger expiries, more magnetic when trading within daily ATR)

- EUR/USD: 1.1175-85 (1.1BLN), 1.1190-05 (2.6BLN

- 1.1250 (231M, 1.1265 (288M), 1.1300 (360M)

- 1.1325 (1.12BLN), 1.1340-50 (402M), 1.1360-65 (286M)

- 1.1375-80 (546M), 1.1440-45 (421M)

- USD/CHF: 0.8300-10 (447M), 0.8325 (310M)

- EUR/CHF: 0.9230 (490M), 0.9400 (651M)

- EUR/GBP: 0.8385 (933M), 0.8600 (831M), 0.8675 (646M)

- AUD/USD: 0.6325 (403M), 0.6475 (201M), 0.6500 (280M)

- 0.6600-05 (1.2BLN). NZD/USD: 0.6025 (415M)

- USD/CAD: 1.3800-10 (1.9BLN), 1.3820-25 (1.23BLN)

- 1.3835-40 (538M), 1.3860-65 (300M), 1.3925-35 (942M)

- 1.3970 (728M)

- USD/JPY: 141.00 (735M), 143.00 (900M), 143.75-85 (720M)

- 144.00 (2.84BLN. AUD/JPY: 88.50 (896M), 97.50 (678M)

Barclays is the first to unveil its preliminary model forecasts for month-end FX flow. The model anticipates a robust demand for USD across all leading currencies. This comes in the wake of the 2nd April liberation day, which caused a global risk-off sentiment and a decline in stock markets. Conventional safe havens, such as US Treasuries and the USD, experienced significant declines as well. This situation resulted in an unexpected expansion of U.S. swap spreads and a spike in credit spreads. The trade-weighted USD dropped by 4.6% in April, prompting a rebalancing that drove USD demand

Credit Agricole’s FX Month-End model signals real money USD buying versus corporate GBP selling and EUR buying

CFTC Data As Of 25/4/25

- Speculators in equity funds have boosted their net short position on the S&P 500 CME by 19,828 contracts, reaching a total of 259,476 contracts. In contrast, equity fund managers have increased their net long position on the S&P 500 CME by 2,780 contracts, bringing the total to 807,842 contracts.

- Speculators have also raised their net short position in CBOT US Treasury bonds futures by 6,902 contracts to reach 107,687 contracts, while they increased their net short position in CBOT US Ultrabond Treasury futures by 27,545 contracts, totaling 247,602 contracts.

- Speculators have reduced their net short position in CBOT US 10-year Treasury futures by 31,649 contracts, leading to a revised total of 906,106 contracts. They raised their net short position in CBOT US 5-year Treasury futures by 129,859 contracts, bringing the total to 2,191,434 contracts.

- Speculators increased their net short position in CBOT US 2-year Treasury futures by 43,222 contracts, reaching 1,297,995 contracts. The net long position in Japanese yen stands at 177,814 contracts, while the euro's net long position is 65,028 contracts. The British pound has a net long position of 20,490 contracts. In contrast, the Swiss franc shows a net short position of -25,474 contracts, and the net short position for Bitcoin is -806 contracts..

Technical & Trade Views

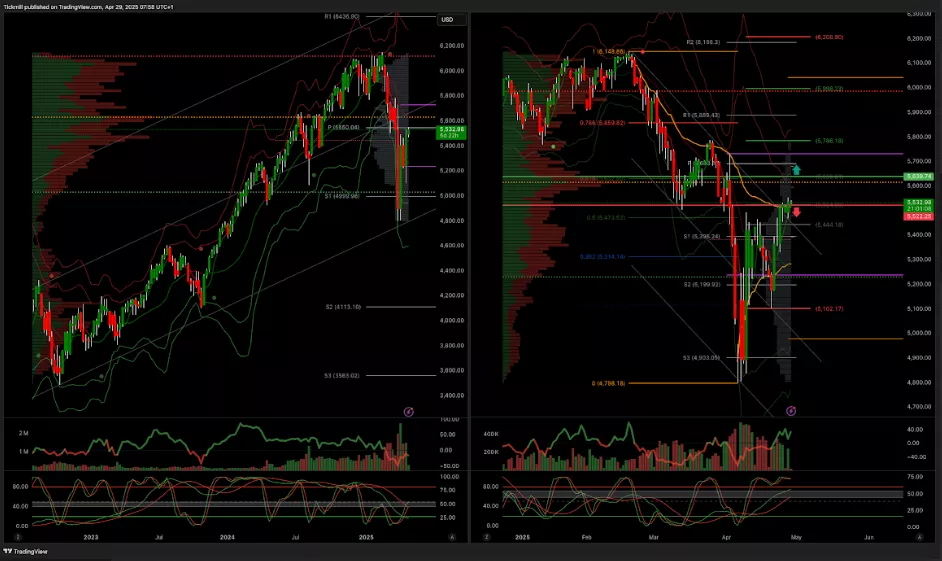

SP500 Pivot 5610

- Daily VWAP bullish

- Weekly VWAP bullish

- Seasonality suggests bullishness into late April

- Above 5640 target 5790

- Below 5500 target 5385

(Click on image to enlarge)

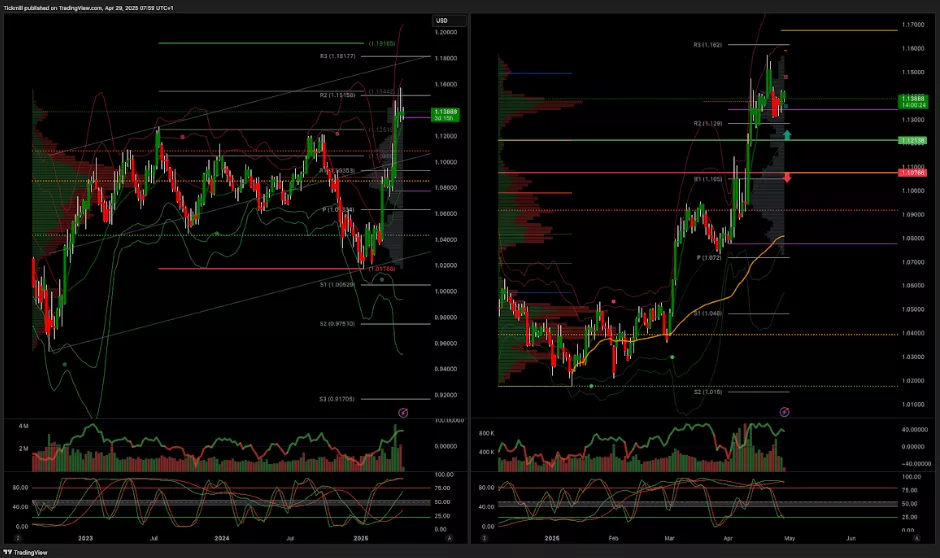

EURUSD Pivot 1.11

- Daily VWAP bullish

- Weekly VWAP bullish

- Seasonality suggests bearishness into the end of April

- Above 1.12 target 1.19

- Below 1.1070 target 1.0945

(Click on image to enlarge)

GBPUSD Pivot 1.28

- Daily VWAP bearish

- Weekly VWAP bullish

- Seasonality suggests bullishness into late April

- Above 1.34 target 1.38

- Below 1.29 target 1.27

(Click on image to enlarge)

USDJPY Pivot 147.70

- Daily VWAP bullish

- Weekly VWAP bearish

- Seasonality suggests bearishness into early May

- Above 1.52 target 153.80

- Below 146.53 target 139

(Click on image to enlarge)

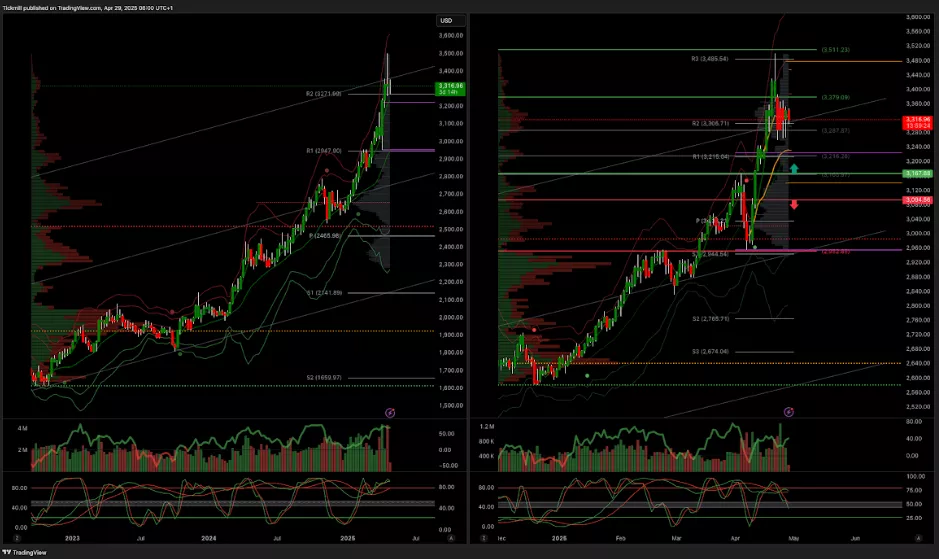

XAUUSD Pivot 3100

- Daily VWAP bearish

- Weekly VWAP bullish

- Seasonality suggests bearishness into late April

- Above 3200 target 3640

- Below 3000 target 2950

(Click on image to enlarge)

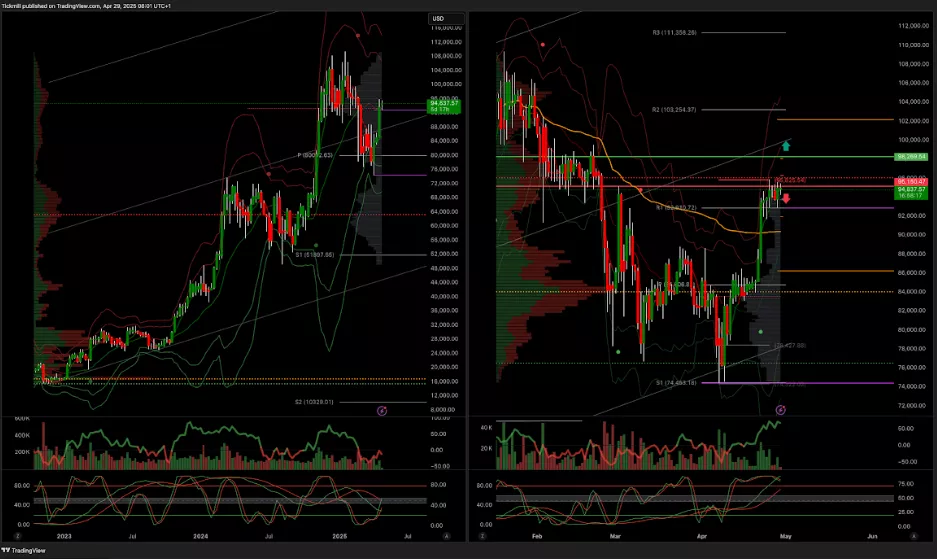

BTCUSD Pivot 96.7k

- Daily VWAP bullish

- Weekly VWAP bullish

- Seasonality suggests bullishness into late April

- Above 97k target 105k

- Below 95k target 65k

(Click on image to enlarge)

More By This Author:

The FTSE Finish Line - Monday, April 29

S&P 500 Weekly Action Areas & Price Targets - Monday, April 28

Daily Market Outlook - Monday, April 28

Comments

Log in or sign up to join the conversation.