Image Source: Pixabay

Asian equities retreated as concerns over potential shifts in US geopolitical strategies weighed on investor sentiment, curbing risk appetite. Meanwhile, the Japanese Yen strengthened. The MSCI index tracking Asian markets fell by 0.6%, while a measure of Chinese tech firms listed in Hong Kong tumbled as much as 3.6% after recently hitting a three-year high. Treasuries gained during Asian trading hours, and gold remained steady at record-high levels. President Trump has intensified pressure on Ukraine to negotiate a peace deal with Russia, unsettling European allies who fear a possible shift away from long-standing support for Ukraine. Additionally, he added to market uncertainty by considering a 25% tariff on lumber, leaving investors guessing about his trade policy direction. US equity futures slipped, and the Yen climbed to its strongest level against the Dollar since December, driven by speculation that the Bank of Japan might raise interest rates sooner than anticipated; investors are now awaiting key inflation data set to be released on Friday.

Gold prices have surged to a new all-time high, driven by safe-haven demand, bringing their 2025 gains to 12%. This marks the ninth record high for the metal this year, following an impressive 27% rise last year—its strongest annual performance in over a decade. Both Citi and Goldman Sachs have recently raised their gold price forecasts, predicting it will surpass the $3,000 mark. A key driver of this bullish outlook is sustained demand from central banks.

The FOMC minutes from January revealed little new, reiterating Powell's stance that further rate cuts require more progress on inflation. Echoing the BoE, the FOMC emphasised a cautious approach due to policy uncertainties, keeping rates stable for now. Attention may shift to balance sheet policy, with two key points: (i) Some members suggested pausing or slowing QT due to reserve fluctuations tied to the debt ceiling, and (ii) the Fed's Treasury holdings may eventually align with the maturity distribution of existing debt. The potential reduction of the $25bn/month Treasury runoff cap is a positive signal for markets.

Heading into next week, German politics and inflation data are set to dominate the macro outlook. Monday is expected to centre around the results of the German elections and the potential formation of a coalition government. Merz’s CDU currently leads in the polls, hoping for a vote distribution that allows a two-party coalition. However, a three-party coalition may be necessary if smaller parties manage to secure the required 5% vote share for representation in the Bundestag. Meanwhile, geopolitical developments involving the US, Russia, Ukraine, and Europe are likely to remain in focus, especially during what appears to be a relatively quiet week for major economic data releases.

In the US, the spotlight will be on Friday’s PCE inflation report, which will indicate whether January’s elevated CPI figures are mirrored in the Fed’s preferred inflation measure. Additional key updates include Q4 GDP revisions (Thursday), various regional Fed surveys, and several Fed speakers throughout the week. For Europe, Germany will see a busier week of data releases, including the IFO Business Climate Index (Monday), retail sales figures (Thursday), and preliminary February inflation data (Friday). In the UK, while the economic data calendar remains light, a packed schedule of MPC speakers compensates. Lombardelli (Monday), Ramsden (Monday/Friday), Dhingra (Monday/Wednesday), and Pill (Tuesday) are all expected to make appearances. Additionally, a Treasury Select Committee hearing on the February Monetary Policy Report is anticipated to take place at some point during the week.

Overnight Newswire Updates of Note

- China Keeps Loan Prime Rates Unchanged, As Expected

- China Tries To Woo Foreign Firms Back After Slump In Investment

- Morgan Stanley Drops Bearish China Stocks Call, Lifts Target 22%

- Australia Hiring Gains Persist Even As Unemployment Edges Up

- RBA’s Hauser: Holding Rates Would Have Led To CPI Undershoot

- Japan’s Food Inflation Is Becoming Harder For BoJ To Overlook

- Fed Officials Seek ‘Further Progress’ On Inflation Before More Cuts

- Vice Chair Jefferson: Fed Can Take Its Time With Labor Market Solid

- French Premier Survives Confidence Vote Over Migration Comments

- Asian Currencies Face More Pain Against Peers As Low Carry Bites

- Gold Holds Near Record High On Trump Tariff Worries

- Oil Edges Lower With Focus on US Stockpiles, Supply Uncertainty

(Sourced from reliable financial news outlets)

FX Options Expiries For 10am New York Cut

(1BLN+ represents larger expiries, more magnetic when trading within daily ATR)

- EUR/USD: 1.0350 (1.2BLN), 1.0370-75 (1BLN), 1.0400-10 (3.7BLN)

- 1.0420 (1.4BLN), 1.0430 (3.8BLN), 1.0435-40 (1.4BLN), 1.0450 (2.7BLN)

- USD/CHF: 0.8935 (650M), 0.9025 (200M), 0.9070 (290M)

- EUR/GBP: 0.8350 (377M). GBP/USD: 1.2500 (305M), 1.2520 (1.3BLN)

- NZD/USD: 0.5660-65 (1.4BLN).

- AUD/USD: 0.6325 (760M), 0.6340-50 (1.3BLN), 0.6375 (1.1BLN), 0.6400 (522M)

- USD/CAD: 1.4155-65 (1.2BLN), 1.4175 (852M), 1.4200 (357M), 1.4250 (350M)

- USD/JPY: 1.4885 (320M), 149.15 (360M), 149.55-60 (380M)

- 150.00 (310M), 150.25 (315M), 151.00 (560M). AUD/JPY: 96.40 (490M)

CFTC Data As Of 14/2/25

- The Euro holds a net short position of 64,425 contracts, while the Japanese Yen shows a net long position of 54,615 contracts. Bitcoin maintains a net short position of 367 contracts, and the Swiss Franc reports a net short position of 38,745 contracts. The British Pound registers a net short position of 3,168 contracts.

- Equity fund managers have increased their net long position in S&P 500 CME futures by 9,526 contracts, bringing the total to 929,941 contracts. Conversely, equity fund speculators have expanded their S&P 500 CME net short position by 33,021 contracts, reaching a total of 366,233 contracts.

- Speculators shifted to a net long position in CBOT US Treasury bond futures, climbing to 44,001 contracts for the week ending February 11, compared to the previous 4,927 contracts. Additionally, they reduced the net short position in CBOT US ultrabond Treasury futures by 3,675 contracts, now standing at 239,941 contracts. However, speculators increased the net short position in CBOT US 2-year Treasury futures by 79,988 contracts, totaling 1,298,612 contracts, and raised the net short position in CBOT US 10-year Treasury futures by 43,331 contracts, now at 751,034 contracts. Meanwhile, the net short position in CBOT US 5-year Treasury futures was trimmed by 65,931 contracts, bringing the total to 1,861,735 contracts.

Technical & Trade Views

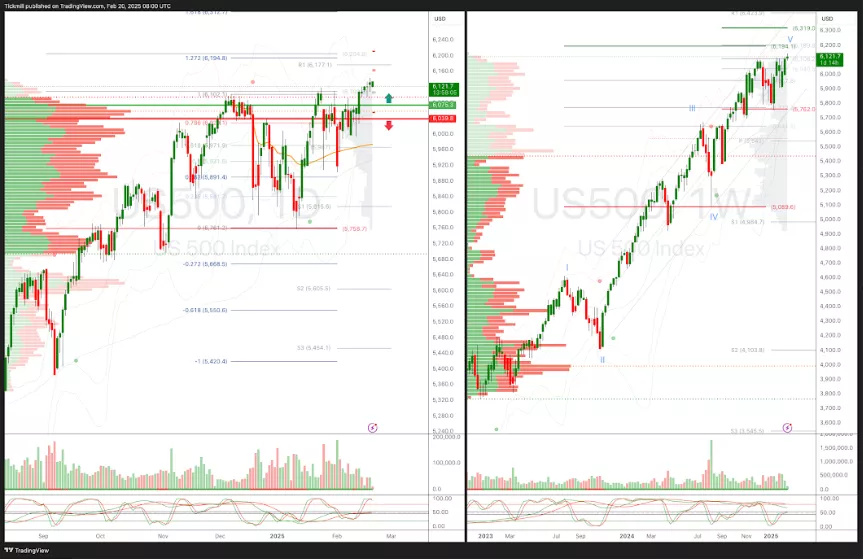

SP500 Pivot 6040

- Daily VWAP bullish

- Weekly VWAP bullish

- Seasonality suggests bearishness Into March 7th

- Long above 6075 target 6195

- Short Below 6045 target 5743

(Click on image to enlarge)

EURUSD Pivot 1.0435

- Daily VWAP bearish

- Weekly VWAP bullish

- Seasonality suggests bearishness into March 30th

- Above 1.0505 target 1.0634

- Below 1.0435 target 0.9758

(Click on image to enlarge)

GBPUSD Pivot 1.2614

- Daily VWAP bullish

- Weekly VWAP bullish

- Seasonality suggests bearishness into March 10th

- Above 1.2685 target 1.2812

- Below 1.2615 target 1.1878

(Click on image to enlarge)

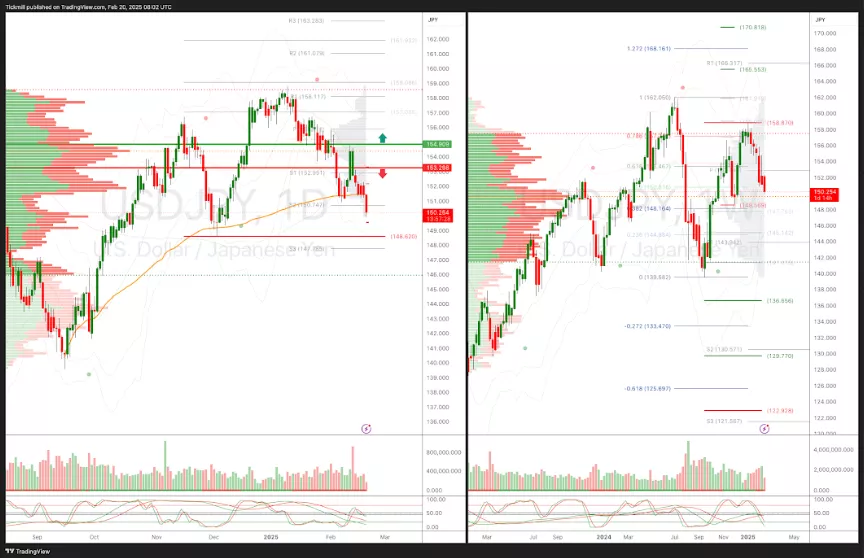

USDJPY Pivot 153.77

- Daily VWAP bearish

- Weekly VWAP bearish

- Seasonality suggests bullishness into Apr 9th

- Above 1.5377 target 165.50

- Below 152.41 target 150

(Click on image to enlarge)

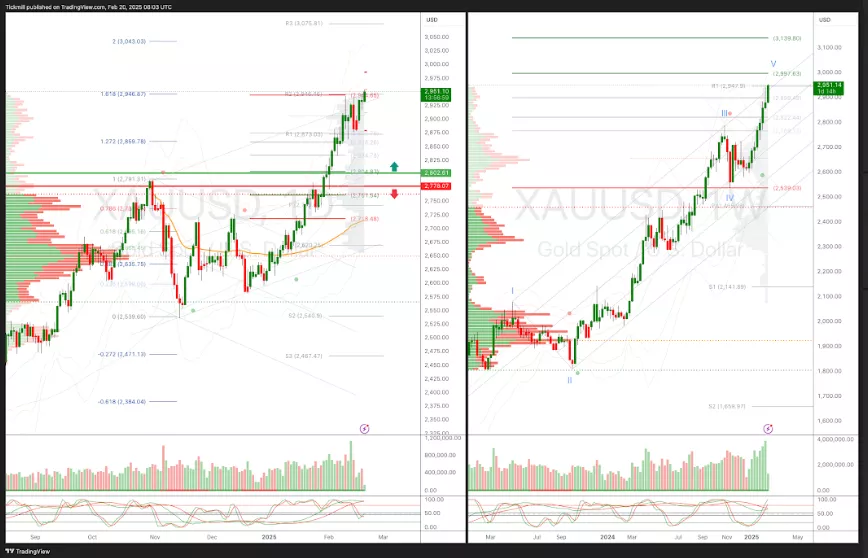

XAUUSD Pivot 2692

- Daily VWAP bearish

- Weekly VWAP bullish

- Seasonality suggests volatile bullishness into Feb 22nd

- Above 2725 target 2997

- Below 2692 target 2475

(Click on image to enlarge)

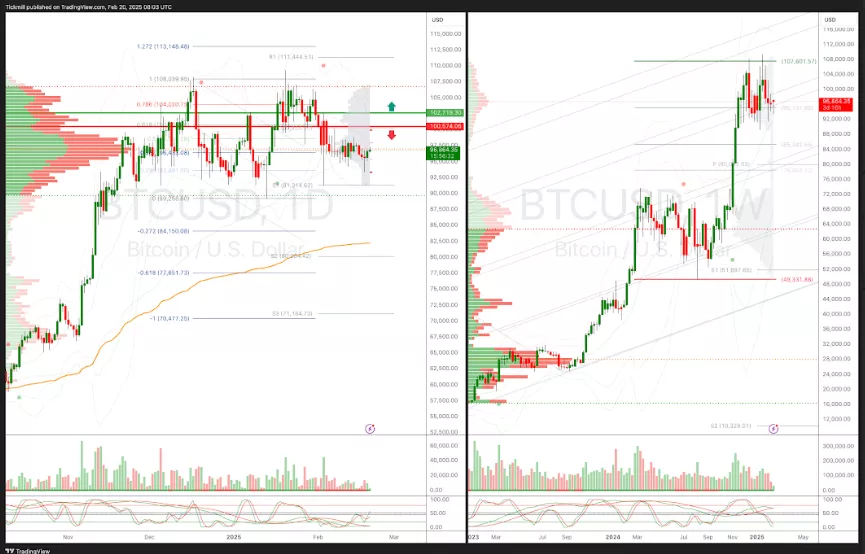

BTCUSD Pivot 101,960

- Daily VWAP bullish

- Weekly VWAP bearish

- Seasonality suggests bullishness into Apr 9th

- Above 104,020 target 110,000

- Below 101,942 target 86,266

(Click on image to enlarge)

More By This Author:

The FTSE Finish Line - Wednesday, Feb. 19

Daily Market Outlook - Wednesday, Feb. 19

The FTSE Finish Line - Tuesday, Feb. 18

Comments

Log in or sign up to join the conversation.