Photo by Tech Daily on Unsplash

Buyers returned to US stocks after worries about Oracle's plans for significant capital investments in artificial intelligence infrastructure led to a general retreat from riskier assets. The S&P 500 rebounded from earlier losses to close up 0.2%, achieving a record closing value and approaching the intraday peak seen in October. Blue-chip and small-cap indexes, which have lagged during the tech-centric equity bull market, reached all-time highs. The Nasdaq 100 reduced a 1.6% loss, although sentiment remained cautious towards major tech stocks following Oracle's disappointing earnings report, which is viewed as an indicator of the AI investment surge. Concerns about major AI players lingered, with Nvidia dropping 1.5% as the Magnificent Seven index fell. Bitcoin recovered slightly after dipping below $90,000. The dollar showed a slight decline. Oracle's results reignited worries regarding inflated tech valuations and whether substantial investments in AI infrastructure will yield significant returns. These concerns have contributed to weeks of volatility throughout November. Despite the sector's role in propelling much of the S&P 500's growth this year, apprehensions about spending have led some investors to shift towards other sectors while the outlook for the US economy remains robust. Oracle’s earnings report was released after the S&P 500 closed just shy of a record on Wednesday, buoyed by a Federal Reserve rate cut and Chair Powell’s positive outlook on the economy. Investors felt reassured that policymakers maintained the possibility of further easing next year, even though the recent quarter-point cut had three dissenting votes. Traders still anticipate two rate cuts in 2026, despite Fed forecasts suggesting only one.

Asian markets surged following new highs in US and global equity indexes, driven by this week's Federal Reserve interest rate cut and an optimistic outlook for the US economy. MSCI's Asian share index increased by 0.9% on Friday, heading towards its best close since November 14th. Japan's Topix led the gains in the region, nearing an all-time high, with financial stocks benefiting from speculation that a Bank of Japan interest rate hike is likely next week. In contrast, Chinese mainland shares declined after the country's leadership signalled a commitment to ongoing economic support but ruled out increasing stimulus next year. The MSCI All Country World Index, one of the broadest measures of the stock market, increased by 0.1% on Friday after hitting a record high in the previous session. It is projected to grow by approximately 21% in 2025, which would mark its best performance since 2019. In addition, the Asian index is currently less than 2% away from its all-time peak set in late October. In the commodities market, copper held steady after reaching a new record high on Thursday, while most other industrial metals rose following the Fed's announcement. Gold dipped after three consecutive days of gains, supported by expectations of further monetary easing in the US, while silver reached a record high. Oil rebounded from its lowest closing price in almost two months, and Bitcoin fluctuated within a narrow range around $92,500.

Domestically, the ONS reported this morning that GDP for October contracted by 0.1% month-on-month, defying expectations of a 0.1% increase. This marks the first decline since June, signalling a challenging economic trajectory. The likelihood of achieving the Bank of England’s November Monetary Policy Report projection of 0.3% quarterly growth for Q4 now seems slim. For this to happen, November and December would each need to see monthly growth of 0.45%, a scenario that appears increasingly improbable—especially considering the ONS highlighted Budget-related uncertainties as a cross-industry factor in October. The services sector was particularly underwhelming, shrinking by 0.3% month-on-month. A notable contributor to this decline was the retail sub-sector, which struggled under the weight of pre-Budget anxieties. Additionally, the lingering effects of last month’s hit to motor manufacturing, stemming from the JLR cyberattack, further weakened the services sector as fewer cars were available for sale. Although motor manufacturing showed some recovery, the rebound was modest at best. On a more positive note, health activities provided the largest boost within the services sector. However, this area faces potential setbacks in November and December due to anticipated disruptions from doctors’ strikes. With these challenges piling up, the prospect of a Bank of England rate cut next week seems increasingly likely.

Overnight Headlines

- All BoJ Watchers See Rate Hike Next Week As Hiking Cycle Resume

- Trump Enlists 5 Allies To Counter China On Rare Earths, Tech

- EU Aims To Agree On Long-Term Freeze Of Russian C. Bank Assets

- JPMorgan, Barclays See Fed Grabbing Major Chunk Of Bill Issuance

- Broadcom Shares Slide After Investors Seek Bigger AI Payoff

- Costco’s Profits Beat Estimates As Shoppers Prioritise Deals

- Retail Crowd Is Loading Up On Netflix After $40B Selloff

- China Forces Reckoning In Europe As Trade Boom Turns Existential

- Oracle’s Credit Risk Hits Highest Since 2009 On Earnings

- Fed Board Votes Unanimously To Reappoint Reserve Bank Presidents

- Disney To Invest $1B In OpenAI, License Characters For Sora AI Tool

- Palantir Says Rival CEO Tried To ‘Pillage’ Its Developers

- Canada’s Carney One Seat Short Of Majority After Second Tory Jumps

FX Options Expiries For 10am New York Cut

(1BLN+ represents larger expiries, more magnetic when trading within daily ATR)

- EUR/USD: 1.1550-60 (2.0BLN), 1.1590-00 (1.31BLN), 1.1635-40 (673M)

- 1.1650-60 (481M), 1.1675 (318M), 1.1695-00 (1.02BLN), 1.1710-15 (403M)

- 1.1725 (237M), 1.1750-55 (1.2BLN), 1.1775-85 (635M), 1.1790-00 (1.2BLN)

- 1.1825 (254M). USD/CHF: 0.8000 (351M)

- USD/JPY: 153.95-00 (363M), 154.15-35 (250M), 155.00 (1.5BLN)

- 156.00-15 (798M), 157.00 (230M)

- GBP/USD: 1.3350 (285M), 1.3415 (421M), 1.3435 (359M)

- EUR/GBP: 0.8700 (627M), 0.8740 (412M), 0.8800 (486M)

- AUD/USD: 0.6550 (207M), 0.6620-30 (371M), 0.6635-50 (1.04BLN)

- NZD/USD: 0.5700-10 (483M). USD/ZAR: 16.80 (794M), 16.90 (390M)

- USD/CAD: 1.3780-90 (970M), 1.3800 (652M), 1.3940 (600M)

CFTC Positions as of the Week Ending 7/10/25

- CFTC FX positioning data backlog clears January 20. Upcoming data on December 2, 5, 9, 12, 16, 19, 23, 30, followed by January 6, 9, 13, 16, 20. Normal service resumes January 23.

- CFTC Positions (Week of October 28th):

- - S&P 500 CME net short: +21,626 contracts (458,504 total)

- - S&P 500 CME net long: +7,029 contracts (906,817 total)

- - CBOT US 5-year Treasury net short: +130,976 contracts (2,404,926 total)

- - CBOT US 10-year Treasury net short: +64,407 contracts (910,930 total)

- - CBOT US 2-year Treasury net short: +34,053 contracts (1,312,475 total)

- - CBOT US UltraBond Treasury net short: -2,057 contracts (297,053 total)

- - CBOT US Treasury bonds net short: -12,678 contracts (15,103 total)

- - Bitcoin net short: -543 contracts

- - Swiss franc net short: -27,858 contracts

- - British pound net short: -20,262 contracts

- - Euro net long: 107,333 contracts

- - Japanese yen net long: 68,115 contracts.

Technical & Trade Views

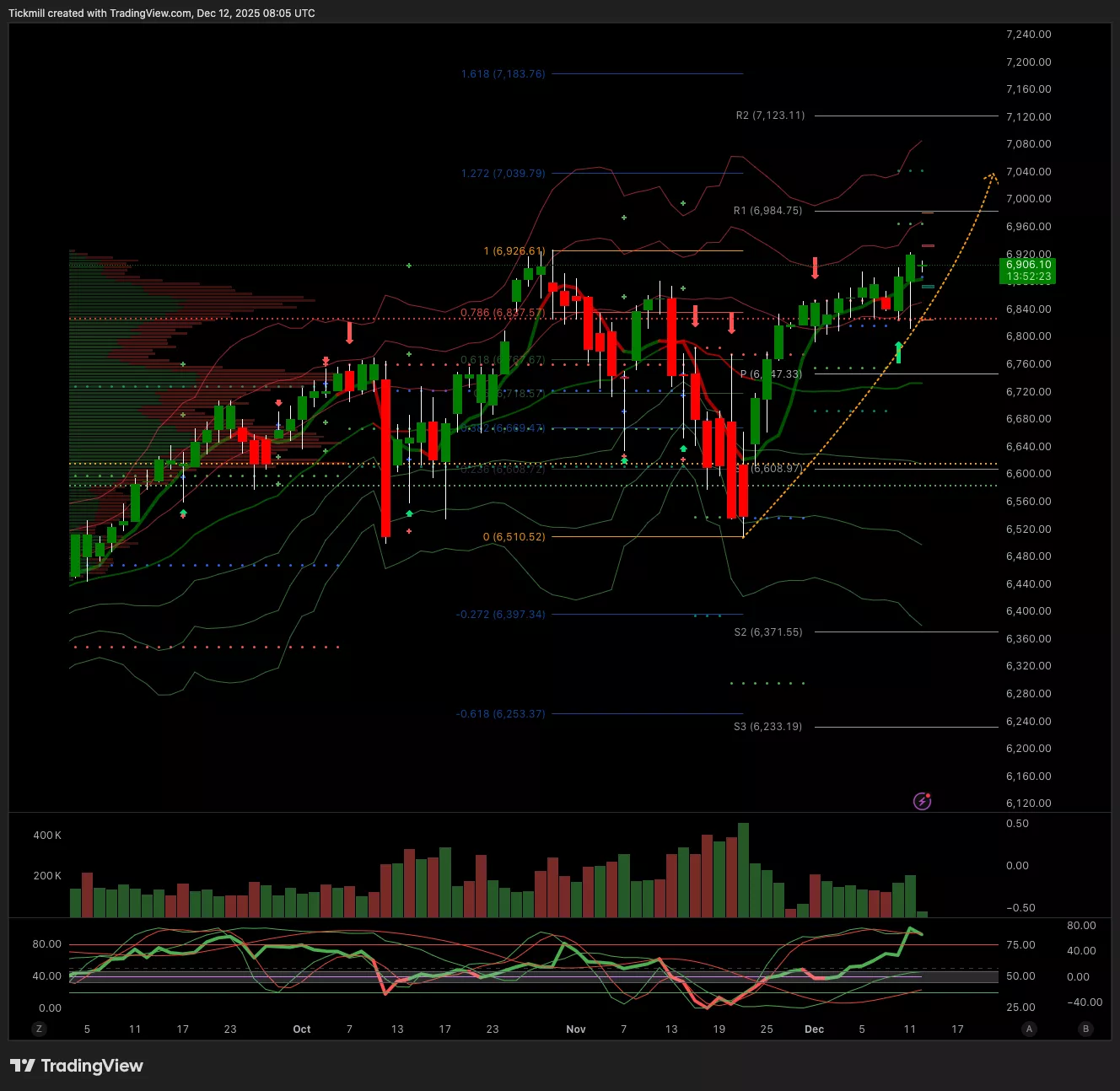

SP500

- Daily VWAP Bullish

- Weekly VWAP Bullish

- Above 6890 Target 7030

- Below 6850 Target 6770

EURUSD

- Daily VWAP Bullish

- Weekly VWAP Bullish

- Above 1.17 Target 1.1780

- Below 1.1650 Target 1.16

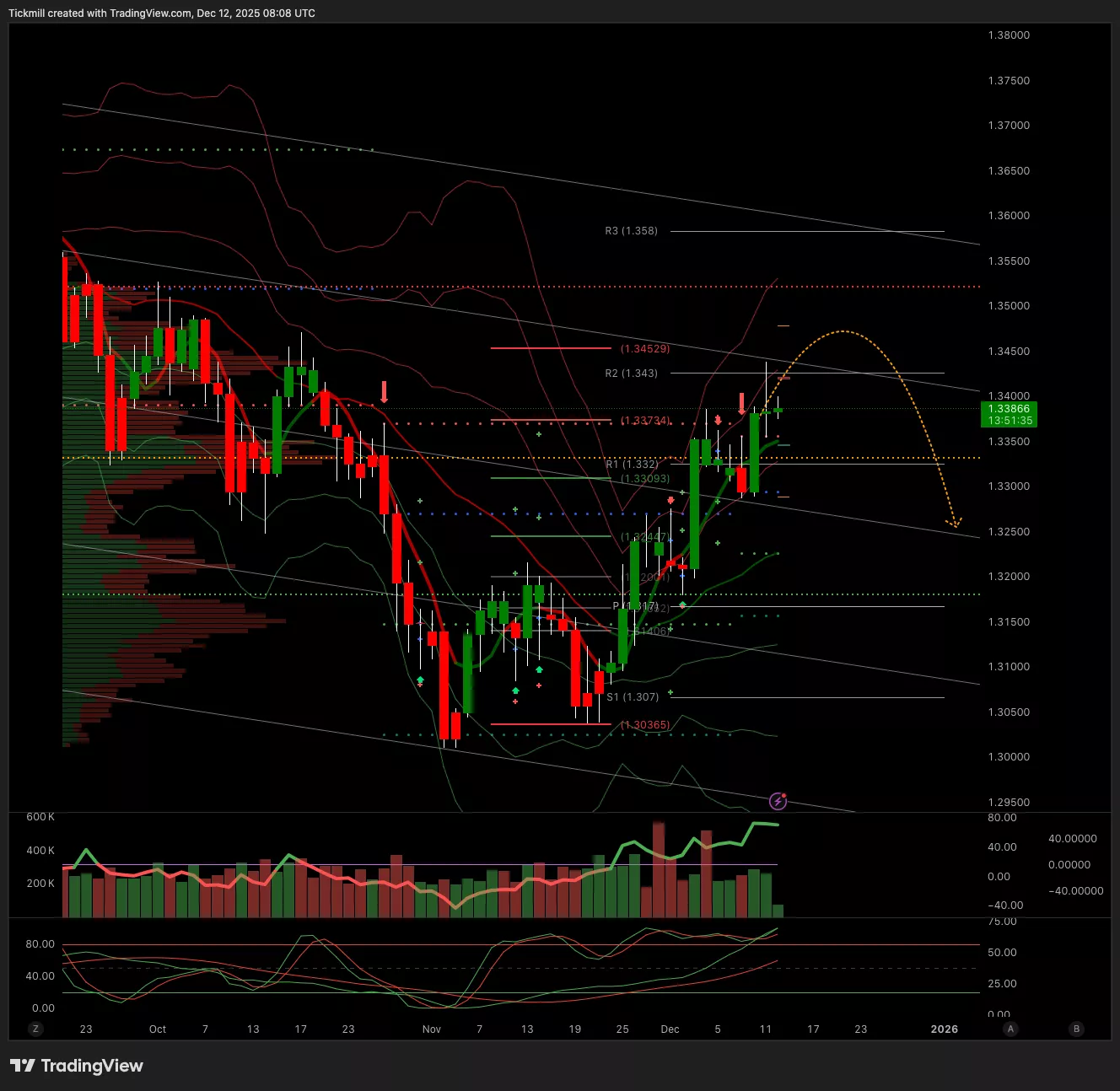

GBPUSD

- Daily VWAP Bullish

- Weekly VWAP Bullish

- Above 1.3330 Target 1.3435

- Below 1.3280 Target 1.3228

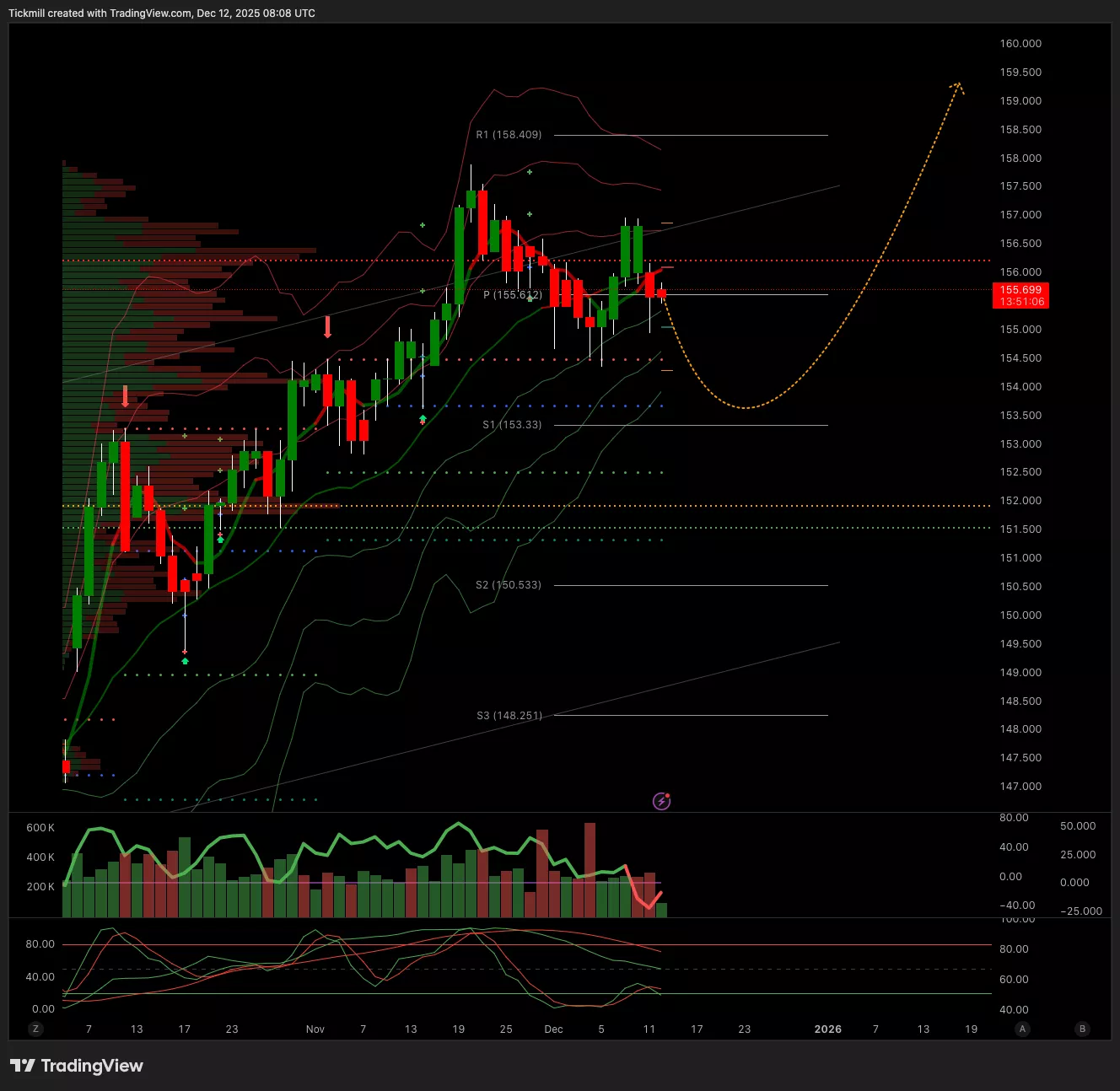

USDJPY

- Daily VWAP Bearish

- Weekly VWAP Bullish

- Above 155.69 Target 157.79

- Below 155.36 Target 154.59

XAUUSD

- Daily VWAP Bullish

- Weekly VWAP Bullish

- Above 4274 Target 4319

- Below 4215 Target 4151

.webp)

BTCUSD

- Daily VWAP Bullish

- Weekly VWAP Bearish

- Above 90.8k Target 95.7k

- Below 89.4k Target 86.2k

More By This Author:

Daily Market Outlook - Thursday, Dec. 11

Daily Market Outlook - Wednesday, Dec. 10

The FTSE Finish Line - Tuesday, Dec. 9

Comments

Log in or sign up to join the conversation.