Why The Wheat ETF Spiked On Monday

The Impact Of War And Sanctions

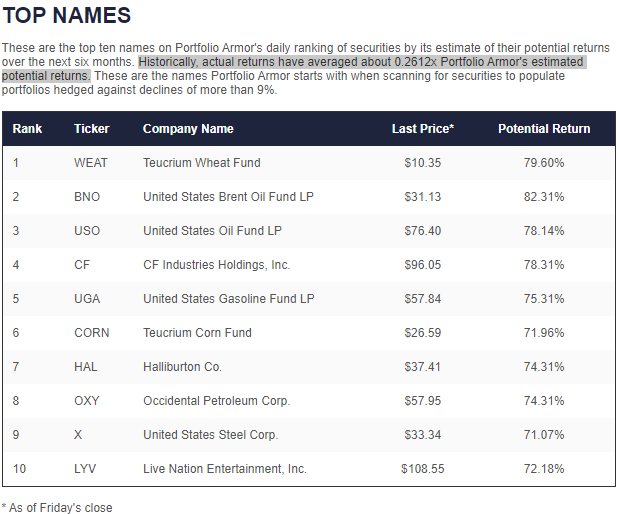

In a post earlier this month (Sanctioning Ourselves), I mentioned how our system's top names reflected the impact of Russia's invasion of Ukraine and the subsequent U.S.-led sanctions on Russia:

As regular readers know, our system doesn't consider the macro picture when selecting its top names. Instead, it gauges stock and options market sentiment to estimate which securities are likely to perform the best over the next six months. Nevertheless, that bottoms-up approach is painting a clear macro picture when you look at our most recent top ten.

Screen capture via Portfolio Armor on 3/11/2022.

Our number one name on Friday was the Teucrium Wheat Fund (WEAT), and two other agricultural names made the list: the Teucrium Corn Fund (CORN) and nitrogen fertilizer producer CF Industries Holdings, Inc. (CF). Fully half of our top ten were oil and gas names including Haliburton Co. (HAL), Occidental Petroleum Corp. (OXY), and the United States Gasoline Fund LP (UGA). Overall, our nine of our top ten names are bets on food and energy getting more expensive over the next six months.

Wheat Fund Spikes On Monday

Shares of the Teucrium Wheat Fund spiked 6.41% on Monday, and it was again the top name in our system on Monday night. The reason for the spike may have been an article over the weekend by the New York Times's Brazil bureau chief, Jack Nicas, arguing that the war in Ukraine might cause a global food crisis. Nicas summarized the key points of his article in the Twitter thread below.

Russia and Ukraine account for 30% of the world’s wheat exports, 17% of corn, 32% of barley & 75% of sunflower seed oil. Russia also exports about 15% of the world's fertilizer.

— Jack Nicas (@jacknicas) March 20, 2022

Now all of that food and fertilizer are stuck.

My story on a looming crisis:https://t.co/mIuWPkqDD9

And all of them will be bidding on an even smaller supply because China is buying much more than usual.

— Jack Nicas (@jacknicas) March 20, 2022

China just revealed that flooding delayed a third of its wheat crop, and now the upcoming harvest "can be said to be the worst in history,” said China’s agriculture minister.

The war in Ukraine is exacerbating humanitarian crises elsewhere.

— Jack Nicas (@jacknicas) March 20, 2022

Aid workers in Afghanistan say it is making it more difficult to feed the 23 million Afghans — more than half the population — who already don't have enough to eat.

More from @Tmgneff: https://t.co/Dp3t64OOfd

Brazil, the world’s largest producer of soybeans, purchases nearly half its potash fertilizer from Russia and Belarus. It has just three months of stockpiles left.

— Jack Nicas (@jacknicas) March 20, 2022

Now farmers are using less, if any, and the soybean crop, already hit by a drought, is likely to be even smaller.

In Case The Wheat Fund Pulls Back

Ideally, negotiations between Russia and Ukraine lead to peace soon. If so, it's possible that the dynamic driving wheat prices higher could reverse, causing shares of WEAT to drop. Here's a way you can hold WEAT now while limiting your downside risk in the event that happens.

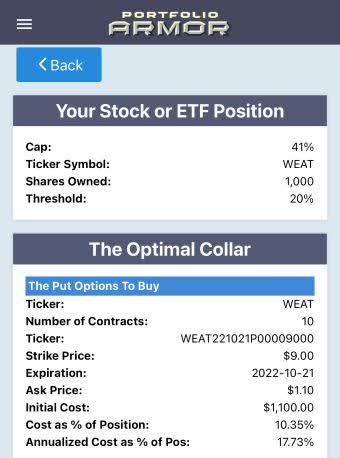

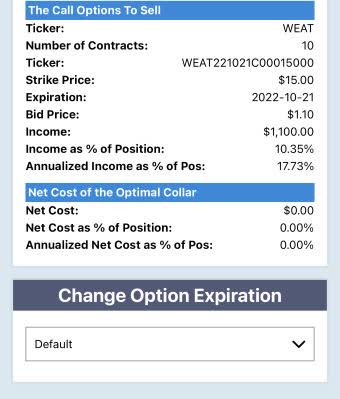

As of Monday's close, this was the optimal collar to hedge 1,000 shares of WEAT against a greater-than-20% drop by late October, while not capping your possible upside at less than 41% by then.

Screen captures via the Portfolio Armor iPhone app.

Since the income generated from selling the call leg was equal to the cost of buying the put leg, the net cost of this collar was negative. To be conservative that cost was calculated assuming you bought the puts at the ask and sold the calls at the bid (the worst end of the spread in each case). Since, in practice, you can often buy and sell options at some price between the bid and ask, you likely would have received a net credit when opening this hedge on Monday.

In either case, your maximum upside would have been slightly more than twice your maximum drawdown.

Disclaimer: The Portfolio Armor system is a potentially useful tool but like all tools, it is not designed to replace the services of a licensed financial advisor or your own independent ...

more