Why Haven't Oil Prices Gone Up?

Image Source: Unsplash

War in the Middle East, blockade of major shipping routes, the slowing of the “energy transition!” In the past any one of these would have been enough for a bull market in oil. But here we are with WTI around $75. What’s going on?

The answer, as is almost always, supply and demand. Let’s start with demand. Over the past ten or so years, I have found it harder to get reliable forecasts of fossil fuel consumption. Many of the government forecasters around the world seem to be using “hope” (often called “officially stated”) forecasts rather than reasonable ones. More recently, even the international organizations lide the IEA have fallen into this trap (There was a good article on this in the Feb 14 WSJ.). So I will use private sector forecasts. The private sector also has motivation to shade things, but they have their own money behind the numbers. So they also have an incentive to be accurate.

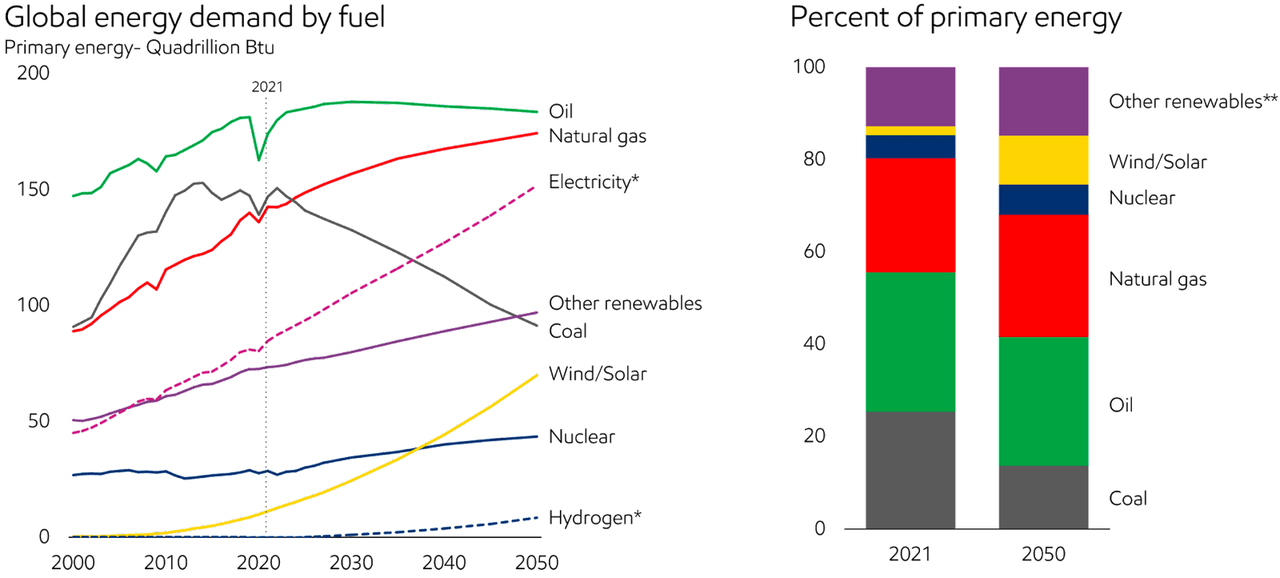

I’ve looked at a few of these forecasts and they are pretty similar. Here’s one from Exxon (XOM):

Fossil Fuel Demand Forecasts (Exxon-Mobile)

You can see that oil consumption peaks right about now and then only slowly tails off. Natural gas is on a sharp ramp up as it replaces coal in thermal generation. So the world will continue to need about the same amount of oil as now, and more gas, for a long time.

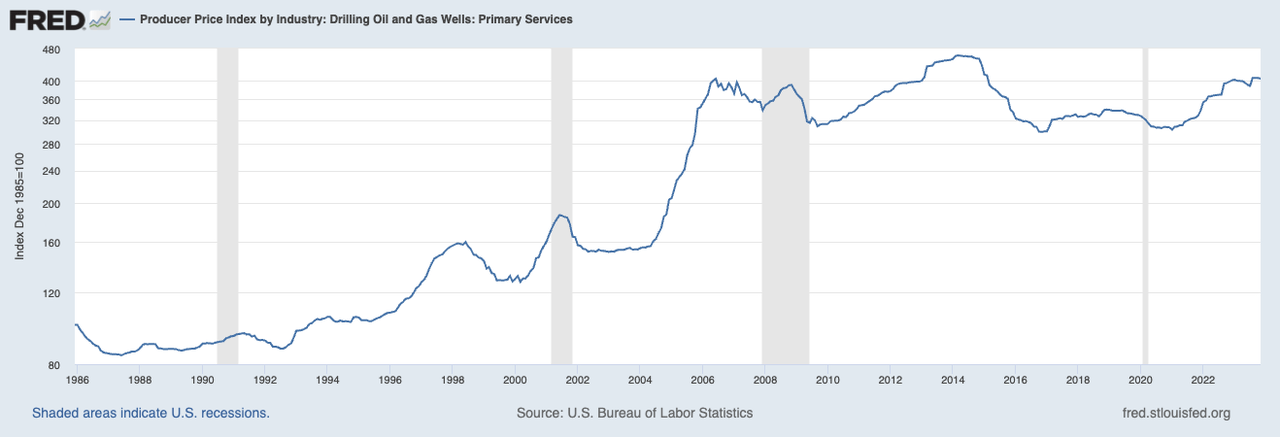

What about supply? Here’s where it gets interesting. At least in the US and Canada, the actual cost of getting oil out of the ground has been declining. Prices are made at the margin, and the US is now the marginal supplier of oil. Let’s start with the US PPI for oil drilling:

US Oil Well Drilling PPI (BLS)

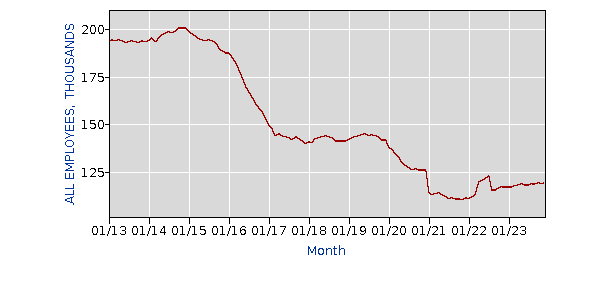

You can see that prices of drilling services (costs for oil drillers) have barely budged since 2005. Meanwhile, overall prices (CPI) have risen 54%. This is also shown in the number of employees in the oil and gas drilling industry:

Bureau of Labor Statistics

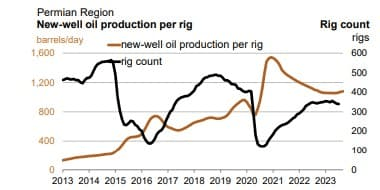

New well production per rig has also increased:

New-Well Oil Production / Rig (US Energy Information Agency)

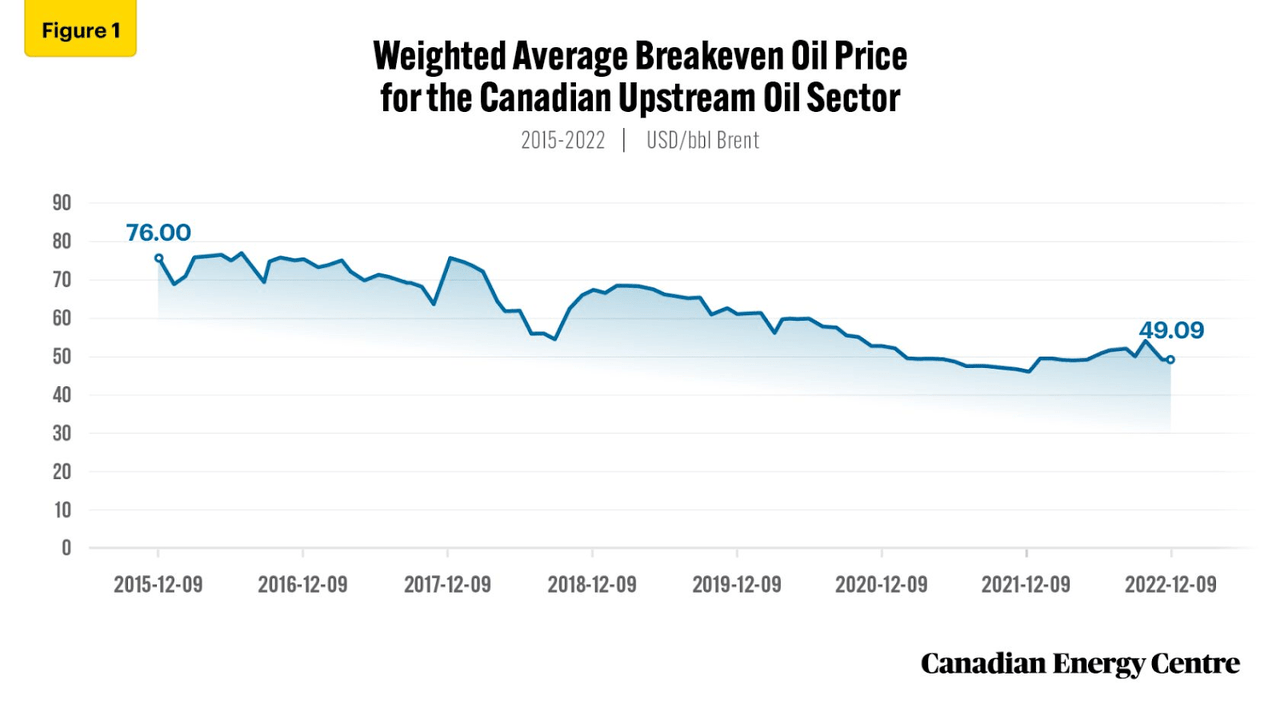

Finally, here’s a graph from the Canadian Energy Centre on Canadian costs.

Canadian Energy Centre

The net of all this is that the extraction cost of oil has come down. Published costs are all over the map, largely because of different definitions of what “cost” is. After reading various reports, here’s what I believe full cost is:

US shale $55 per bbl.

Canada (total) $50

Brazil $49

Nigeria <25

Will this decline continue? Technology forecasting is always difficult, and I’m only going to say “probably”. The majors are investing huge amounts of money into buying up smaller company shale properties. These companies have access to the latest data, and they wouldn’t be making these investments if they thought they couldn’t make money on them. Also, technology changes often play out over a long period of time, so the odds are on the side of progress.

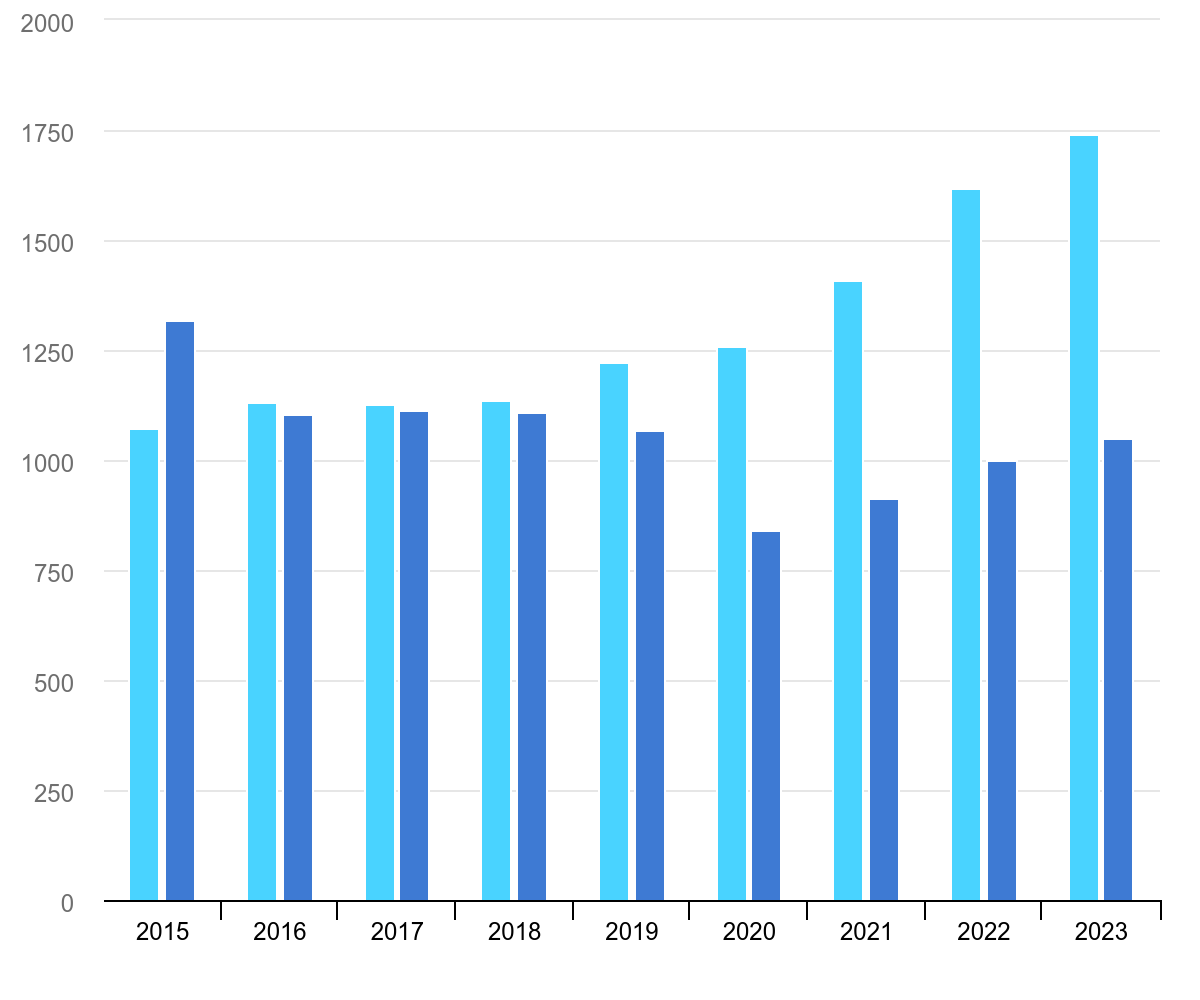

It’s worth noting that worldwide investment in oil and gas has never really recovered from the crisis of 2020. Here’s a chart from the IEA. The dark blue bars are fossil fuel investment; the light blue bars are “clean energy”

Worldwide Energy Investment (IEA - World Energy Investment 2023)

What does this mean for listed oil companies? First, their costs are declining. That’s good. But since the marginal supplier (the USA) is the one whose costs are declining, that means lower selling prices. That’s bad. On this basis it should be roughly neutral.

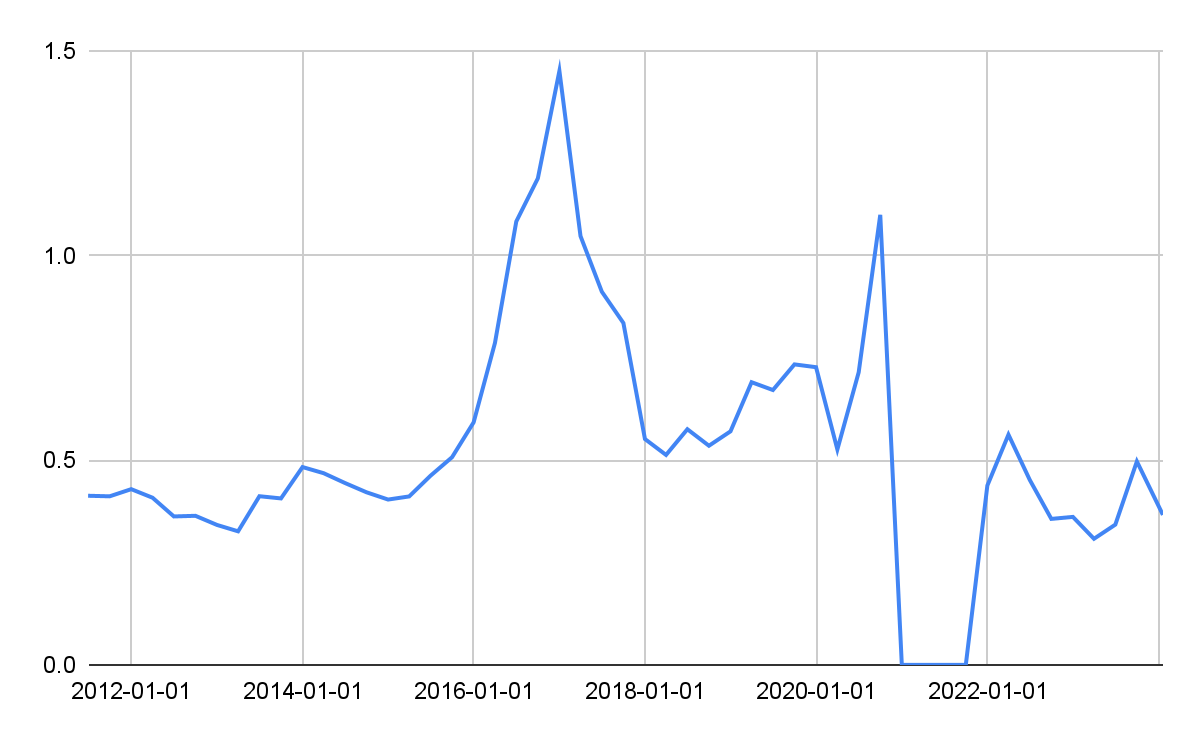

But there’s another issue at play here. OPEC+ is not likely to take continuing lower prices lying down. At some point they are possibly going to reassert their market power. This could lead to another price war. Now I’m not forecasting when this will happen or even if it will. But the threat of it is going to hang over the market for some time. This will lead to lower multiples for oil equities. We are already seeing this. Take XOM for example, a great barometer of energy equities. It is trading at a multiple of 41% of the overall market. Here’s a graph of XOM's PE multiple versus the overall stock market PE:

XOM PE / SP500 PE (Author's Calculations)

The break in the curve around the pandemic is because XOM was losing money then. XOM’s PE is only 41% of the overall market. That seems like good value, but I expect that to continue to be low.

Here's how I am playing this. I believe the dividends of the majors are safe, so I hold a smallish position for income. But the big play will be if OPEC brings down the hammer. This would lead to a repeat of what has happened many times in the past - much lower oil prices for a year or so. Given the long term pessimism for fossil fuels, this would probably lead to much lower oil equities. That is the opportunity I am waiting for.

More By This Author:

Disclaimer: This is for education only. I am not recommending anyone follow me in any trading/investing I do. If you follow someone else's trades without doing your own research, you will ...

more

Great read, very thorough.

Agreed.