U.S. Fall Corn Demand Is Up, But 2023’s Hefty Crop Jumps Stocks

Image Source: Unsplash

Market Analysis

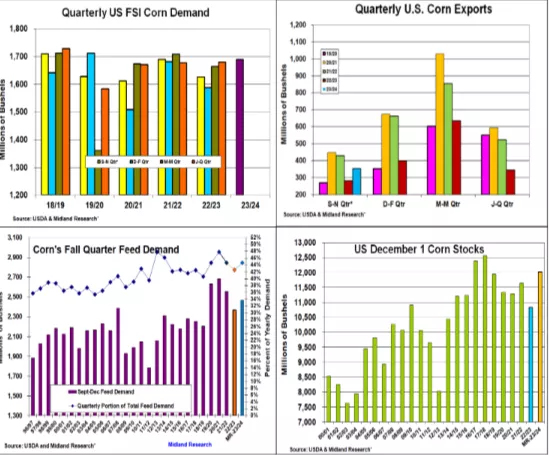

This year’s larger US corn crop & lower cash prices has boosted both the US & overseas demand during the 1st quarter of this crop year. However, 2023’s expanded US plantings and a 10.6% larger corn output substantially increased the available US feedgrain supplies for the coming year. The world’s coarse grain supplies have some current uncertainties. Argentina moisture and prospects have improved, but Brazilian dryness delaying their bean plantings will likely curtail their 2nd-crop corn plantings & dip yields when the growing period is pushed into their dry season.

Declining energy prices & expanding ethanol processing margins strengthen corn’s 1st quarter industrial demand. Strong daily commuter activity & expanding longer-distance family car travel also added to the US gasoline & ethanol demand. Last fall’s ethanol corn usage was up by 5% or 62 million bu to 1.69 million bu of FSI demand. This is like ethanol’s 2021 demand before Russia’s attack of Ukraine jumped gas prices & reduced ethanol use.in 2022.

Like soybeans, last fall’s dry Midwest weather limited the US Mississippi River barge loading capacity & movement during the first month of the 2023/24 export season. Tight old-crop summer supplies keeping US prices strong & Brazil’s safrina corn crop overwhelming their transportation network prompted China to source their corn needs from S America. However, 2023/24’s lower US cash prices did attract other oversea buyers to the US. Last fall’s US quarterly exports rose 71 million to 354 million in the first quarter but remained 77 million below 2021’s fall export pace.

Record beef prices & declining US Plains pasture conditions prompted nearly 1 million feeder cattle to move in the US feedlots last fall. Steady broiler numbers & a recovery in pigs per litter kept market hog numbers unchanged despite a 3% lower breeding herd. This suggests a 103 million fall feed demand. Overall, corn’s quarterly usage may rise by 236 million bu. However, 2023’s 16.5 billion total supply will likely keep this year’s Dec1 stocks at 12 billion bu, 11% higher than 2022 & the highest level since 2018.

(Click on image to enlarge)

What’s Ahead

The upcoming US quarterly corn stocks will show larger supplies than 2022 on January 12. However, S America’s weather & the USDA’s 2023/24 ending stocks will also be factors. Brazil’s northern safrina crop remains vulnerable with the region’s current soybean crop needing to be harvested before 2nd crop corn is planted. Up old-crop by 15% at $4.75-85 March & begin 2024 sales by 15% at $5.08-12 in Dec.

More By This Author:

US Fall Exports Dip, But December Stocks May Slip On Lower 2023 Crop

US/World Limited Stocks Changes Keep South American Output Important

After The Recent Export Surge, US Ending Stocks Aren’t Expected To Change

Disclaimer: The information contained in this report reflects the opinion of the author and should not be interpreted in any way to represent the thoughts of any futures brokerage firm or its ...

more