The World’s Fragile Economic Condition – Part 2

The world economy can appear to be operating quite well but can be hiding a major problem that causes it to be fragile. My presentation The World’s Fragile Economic Condition (PDF) explains why we should expect financial problems if energy consumption stops growing sufficiently rapidly. In fact, a global sell off in the equity markets, such as we have started to see recently, is one of the kinds of energy-related impacts we would expect.

This is Part 2 of a two-part write up of the presentation. In Part 1 (The World’s Fragile Economic Condition – Part 1), I explained that a large portion of the story that we usually hear about how the world economy operates and the role energy plays is not really correct. I explained that the world economy is a self-organized system that depends upon energy growth to support its own growth. In fact, there seems to be a “dose-response.” The faster energy consumption grows, the faster the world economy seems to grow. The period with fastest growth occurred between 1940 and 1980. During this period, interest rates were rising and workers saw their wages increase as fast as, or faster than, inflation. After 1980, the rate of growth in energy consumption fell, and the world needed to tackle its growth problems with a different approach, namely growing debt.

In this post, I explain how debt (and its partner, the sale of shares of stock) help pull the economy forward. With these types of financing, investment in new production becomes almost effortless as long as the return on investment stays high enough to repay debt with interest and to repay shareholders adequately. At some point, however, diminishing returns sets in because the most productive investments are made first.

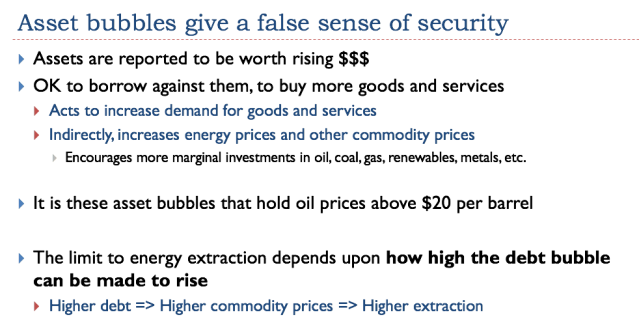

The way diminishing returns plays out in energy extraction is by raising the cost of producing energy products. In order for the sales prices of energy products to rise to match the rising cost of production, rising demand is needed to give an upward “tug” on sales prices. This rising demand is normally produced by adding increasing amounts of debt at ever-lower interest rates. At some point, the debt bubble created in this manner becomes overstretched. We seem to be reaching that point now, especially in vulnerable parts of the world economy.

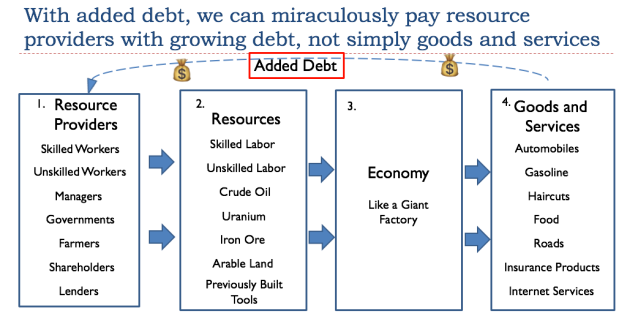

Let’s first look at a slide from Part 1, explaining the way in which the economy works like a giant factory.

As long as energy products are very inexpensive, it is possible for the economy to expand very rapidly. When this happens, the Goods and Services produced in Box 4 are able to grow so rapidly that all of the Resource Providers in Box 1 can be well compensated, simply by using a quasi-barter arrangement, facilitated by the use of money. With this approach, Resource Providers can get adequately paid using the Goods and Services produced in close to the same time period. Something of this nature occurred prior to 1970, when inflation-adjusted oil prices were less than $20 per barrel (Part 1, Slide 26).

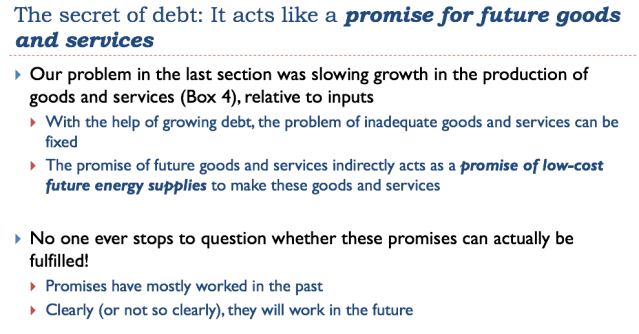

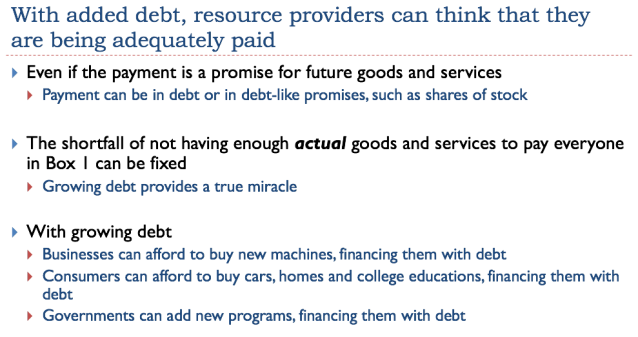

If the growth of the economy slows, so that not enough Goods and Services are being created by the economy to use this approach, it is possible to work around the problem by adding debt. Adding debt makes it possible to substitute promised future Goods and Services for not-yet-produced Goods and Services.

Added debt makes it seem like more goods and services are available to pay resource providers.

Selling shares of stock acts very much like debt, because the funds provided by these shares also provide access to goods and services that others have already produced. In the case of the sale of shares of stock, the promises are for future dividends, capital appreciation, and partial ownership of the company.

Growing debt looks like it can solve all problems. No wonder that Keynesian economists found it so useful. But the return must remain high enough to repay debt with interest.

Borrowing money generally comes with the requirement that the amount borrowed be repaid with interest. If the energy purchased using debt allows the economy to grow fast enough, there is no difficulty in repaying debt with interest. If energy is very inexpensive (equivalent to oil cost less than $20 per barrel in inflation-adjusted price), this payback system generally works, because a large amount of energy can be purchased for a small quantity of debt.

If the price of the energy rises, much more debt is required for the same amount of energy produced. For example, if oil is $80 per barrel, the affordability is much lower. It takes four times as much debt to pay for a barrel of oil. Repayment of debt with interest becomes more difficult.

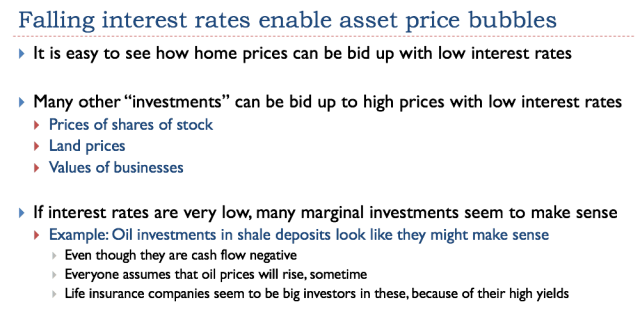

In Part 1, we observed that US long-term interest rates have been falling almost continuously since 1981. This situation of falling interest rates led to falling mortgage payments for a given amount borrowed. Because of the lower monthly payments, homes became more affordable; in other words, there tended to be more potential buyers for homes at a given price level. Indirectly, the increased affordability of home ownership tended to raise the resale value of homes. It also encouraged the building of additional homes.

Building homes indirectly requires the use of many different types of commodities. Metals are used in pipes and in wiring. Wood is used for framing. Concrete is often used for the basement. Oil is needed to haul these goods to the site where the home is to be built. Thus, indirectly, falling interest rates tend to raise commodity prices.

Many assets are purchased with debt. If interest rates are very low, purchasing these assets becomes more affordable. The sale of shares of stock provides another way of raising capital for a company. In the case oil-producing companies, purchasers of shares of stock often think, “If extraction costs are rising, surely oil prices and other energy prices will rise as well.” This belief allows the price of shares to stock to be bid up to a high level.

When asset prices rise, economists sometimes refer to the “wealth effect.” Homeowners feel richer if their homes are worth more, and they can borrow more against them. Owners of shares of stock feel richer if their shares of stock have higher values. Owners of pension plans are happy when stock prices are high, because it looks as if these shares can be sold, allowing the plans to meet their pension obligations.

If the debt bubble stops growing, then the commodity price bubble cannot continue to grow. In fact, it may abruptly “pop.” This is what happened in the second half of 2008, when oil prices dropped precipitously, from $147 per barrel to the low $30s.

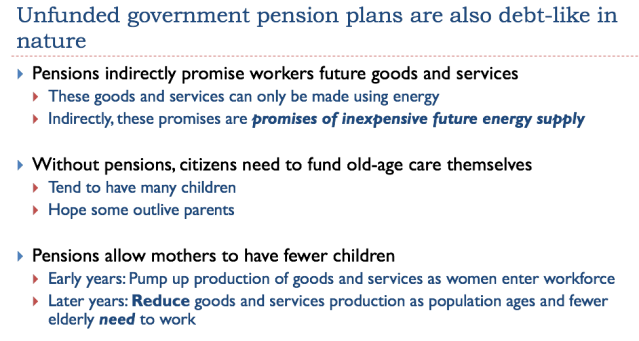

Government pension plans such as Social Security are not treated as debt because they are not guaranteed, but they act in much the same way as debt.

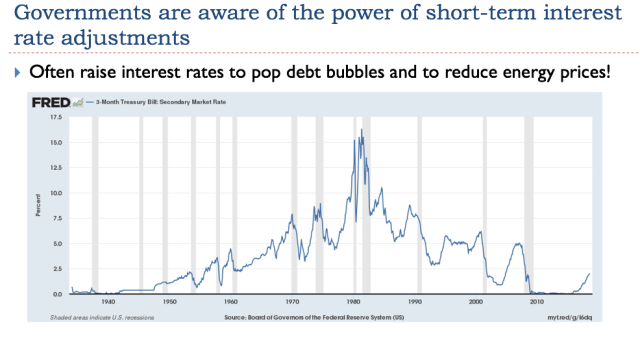

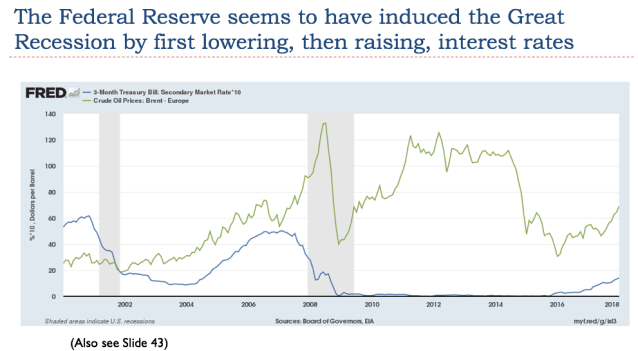

The gray bars on Slide 45 indicate recessions. These recessions often seem to be intentionally caused. If a person looks closely, it is possible to see that in most cases, increases in US short-term interest rates preceded recessions. In fact, if a person looks at the minutes of the Federal Reserve Open Market Committee, it is sometimes clear that the Open Market Committee raised interest rates to intentionally pop asset bubbles in order to “reduce volatile food and energy prices.”

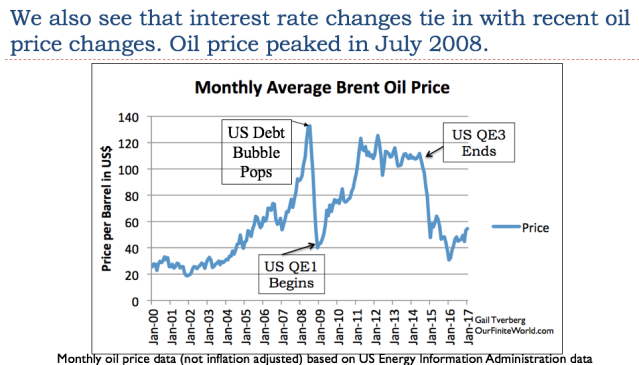

The huge interest rate spike to 18% in 1981 on Slide 43 corresponds with the big drop in oil prices on Slide 44. Interest rates were so high that buyers could no longer afford new homes or factories. Prices seem to have been brought down by falling demand.

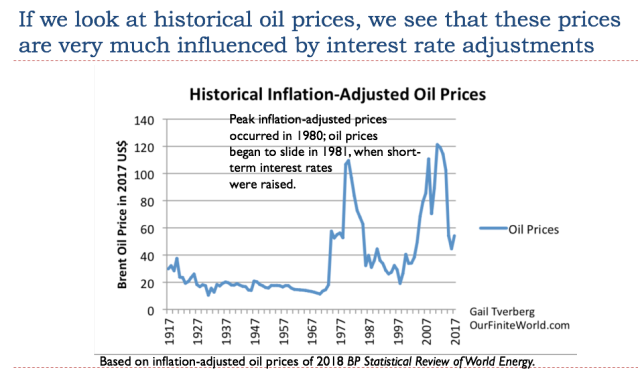

If we look at recent oil prices, we can also see that they also depend very much on interest rates. In my paper, Oil Supply Limits and the Continuing Financial Crisis, I show that the US debt bubble popped precisely when oil prices hit a peak in July 2008. That is when US consumer credit and mortgage debt started falling.

On Slide 45, QE stands for Quantitative Easing. This was a program that allowed lower long-term interest rates in addition to lower short-term interest rates. Thus, it gave the Federal Reserve (and other central banks) the power to reduce interest rates to an even greater extent than was possible by reducing short-term interest rates alone.

The Federal Reserve seems to have been instrumental in causing the Great Recession, as well. Slide 46 shows a larger scale of the same information about oil prices and short-term interest rates shown on Slide 43. There can be several years between the time interest rates are raised and the resulting recession occurs, so most people miss the role that intentionally raising short-term interest rates plays.

Also, high oil prices also tend to have an adverse impact on the economy because energy prices rise, but wages do not rise at the same time (Part 1, Slide 28). Consumers are forced to cut back on discretionary goods when the cost of necessities (such as the cost of commuting and the cost of food) rise.

In fact, it seems to be the combination of rising energy prices and increased interest rates that leads to recessions.

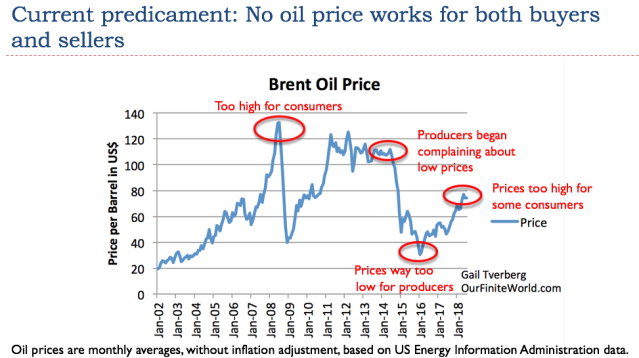

On this chart, I show some of the comments heard about oil prices. In mid-2008, it was clear that high oil prices were becoming a problem, especially for those with subprime mortgages, living in homes that were distant from their work. By early 2014, we started hearing that oil prices had been too low for oil producers in 2013. Because of the unprofitability of oil production, some oil producers were cutting back on investment in new production. See my post, Beginning of the End? Oil Companies Cut Back on Spending.

Now, it is fairly clear that no oil price will work for both producers and consumers. Today’s Brent oil price of about $80 per barrel is both too low for producers and too high for some consumers. Consumers who are particularly affected are those whose currencies are falling relative to the dollar, such as consumers in Turkey and Argentina. Even countries with more modest decreases, such as China and India, are cutting back on automobile purchases. This change will affect future oil demand.

If, by some chance, oil prices should spike to a high level such as $100 per barrel, the affordability problem pretty much guarantees that oil prices will fall back fairly quickly. This issue, by itself, makes it impossible to believe that oil prices will increase endlessly.

I should mention, too, that we are also at a point where no interest rate works for everyone. Those buying new homes and new cars need low interest rates, in order for these goods to be affordable. Pension plans, on the other hand, need high interest rates, in order to meet their pension promises. There is no one interest rate that works for every purpose.

Thus, we have a combination problem: no interest rate works for everyone, and no set of energy prices works for everyone.

The Federal Reserve is now in the process of raising short term-interest rates (see Slide 43). It is also selling the QE securities that it previously acquired to reduce long-term interest rates. If buying these QE securities lowered long-term interest rates, selling them should raise long-term interest rates. Raising both short- and long-term interest rates sounds like a formula for creating a huge number of debt defaults and lowering prices of shares of stock. It is likely that these actions will also start a major recession.

–

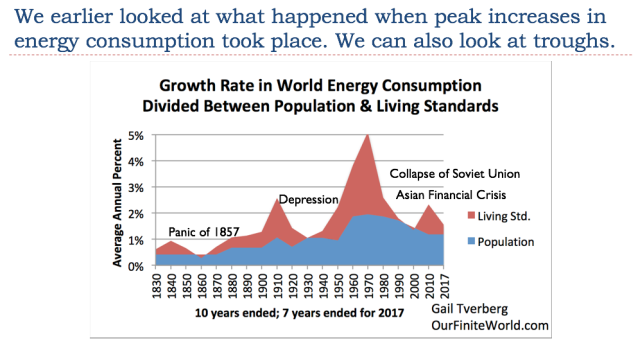

On Slide 50, “earlier” refers to Slide 16 in Part 1 of this presentation. From Part 1, we remember that the first small peak refers to the California gold rush; the second larger peak about 1910 refers to “Electrification and Early Farm Mechanization.” The third peak about 1970 refers to the “Postwar Boom.” The last small peak refers to the expansion made possible by China’s growth, and the growth of other Asian countries.

Slide 50 shows that the troughs refer to periods that were bubble collapses, or the collapse of the central government of the Soviet Union. Slide 51 (next) gives details with respect to these low periods. These were bad times for economies: depression, debt collapses, and periods with significant wage disparity. They were not periods with high energy prices.

Clearly, none of these low periods was a good period for the economy. While we can see that there was low energy consumption during the periods, the primary reason for this low energy consumption was the collapse of a debt bubble or of a government.

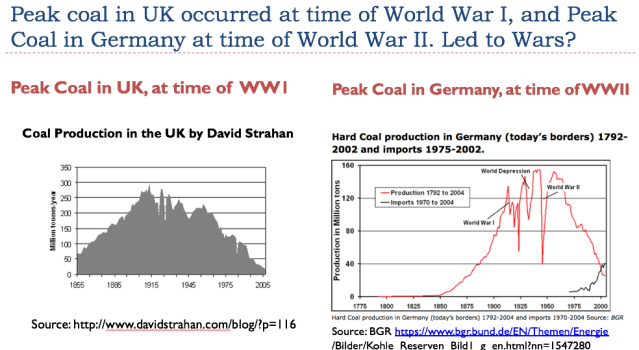

Peak coal occurred in the United Kingdom in 1913, and World War I began shortly thereafter, in 1914. When peak coal occurred, wages for workers were very low, because diminishing returns had made the operation of coal mines increasingly expensive, but those purchasing coal could not afford higher coal prices. Thus, mining companies could not afford to pay workers adequate wages. World War I gave an alternative employment opportunity for coal miners and others with low wages.

Entering World War I was a very successful strategy for the UK. The fact that the UK was on the winning side allowed the UK to retain its role as the holder of the reserve currency. In this position, it was fairly easy for the UK to borrow the funds needed to obtain coal and other energy imports.

Germany seems to have encountered peak coal about the time World War II began. Was this an attempt to cover up Peak Coal? We don’t know for certain, but the timing certainly looks suspicious.

In both of these cases, low energy supply seems to have led to fighting, rather than high prices.

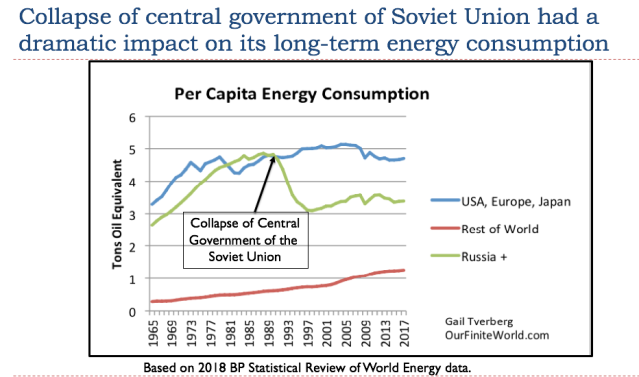

The collapse of the central government of the Soviet Union seems to be an indirect impact of the long term low oil prices in the 1981-1991 period. The high oil prices of the 1970s had encouraged the Soviet Union to ramp up oil production. Once the US raised interest rates and oil prices fell, there were no longer funds for investing in new oil production. The Soviet Union was dependent on oil exports. It was able to continue for quite a few years with low prices, but eventually its central government collapsed. Over the long term, consumption has continued to be much lower, reflecting the permanent loss of industry.

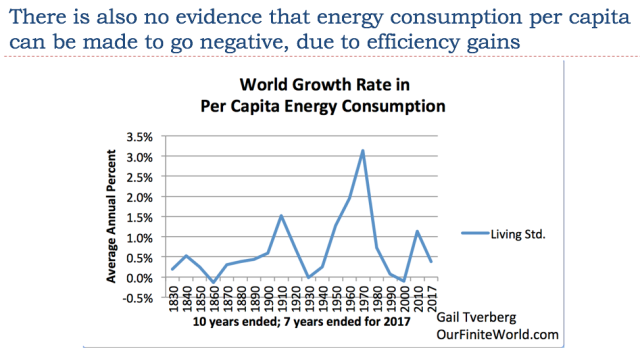

Slide 55 is a graph of the “peaks” on Slide 50. If we listen to mainstream economists (including Paul Romer and William Nordhaus, who recently received the Nobel Prize in economics), improved technology can allow the world economy to become increasingly efficient, and thus overcome the problem of diminishing returns. Slide 55 shows that over a period of nearly 200 years, this has never happened in the past. The troughs represent collapses of one kind or another. These low periods did not represent sustainable situations.

The problem is that diminishing returns leads to the need for very different techniques to work around new problems. For example, if there are diminishing returns with respect to extracting fresh water from wells, the first alternative is to dig deeper wells. Efficiency gains can somewhat help offset the cost of deeper wells. But once the problem advances to the point where desalination is needed, plus remineralizing the water with the correct minerals after desalination, the cost of fresh water becomes much higher. It becomes impossible for improved technology to work around the very large increase in costs that diminishing returns seems to cause.

We haven’t been able to work around diminishing returns with increased efficiency before; we are likely kidding ourselves if we think we can do so now.

–

–

The point that should be emphasized is that the reason why the United States economy now looks fairly good is because we are at the top of a debt bubble. This bubble is partly the result of world’s long running low interest rates, and partly because of the United States’ recent tax cuts. Thus, the situation today is a lot like 1929 before the debt bubble collapsed, or a lot like 2007 before the economy derailed. Things look good, but they won’t necessarily stay favorable for very long.

Separate Additional Conclusions for Various Audiences

At this writing, I have actually given variations on this talk three different times, to different audiences. The first audience (which is the one I mentioned at the beginning of Part 1) was a meeting of about 100 property-casualty actuaries. These actuaries help determine rates and financial statement amounts for lines of insurance such as automobile, homeowners, and medical malpractice. The specialized conclusions I added for that audience were the following:

–

The second version of my talk was given at the 2018 Bermuda International Life and Annuity Conference, to a group of 300+ insurance executives of various kinds. This talk was called Energy Economics: Is a Discontinuity Ahead? This audience was especially interested in my talk because interest rates are central to the operation of pension plans. If interest rates do not rise, this is a major concern for this group.

The conclusion slides to that presentation were the following:

–

The third version of the presentation I gave was to a group of followers of Peak Oil theory. This presentation was somewhat shorter and slightly rearranged. The title of this presentation was How the Energy System Really Works and What Seems to Be Going Wrong.

Its short conclusions’ sheet mentions the following dangers:

Disclosure: None.

This is interesting and points out many problems, but is not as dire as the article implicates right now. The issue is the continuation and exacerbation of existing trends. As we can see in the US, be it Democrats or Republicans, without both to keep them in check they both inflate the deficit in different ways. This may be one reason mid term elections will put Democrats back into the House. Sadly, the Republican's argument that they are fiscally prudent has failed miserably under Trump who advocated getting rid of deficit spending if elected.

Europe is even worse with Greece and Italy ruining their concept of fiscal prudence, but even then, it looks like they will wallow along for a few more years until no one can save them.

On the energy front, oil prices have risen enough for the big companies to increase production in the US again. The smaller indebted oil companies will eventually need to be bought out to cover their debt loads which would have been tolerable if they built now instead of 3 years earlier. There is certainly fiscal solvency in big oil, especially Exxon. So I am not as concerned as the author about oil drilling growth coming to a standstill. I am more worried about the issue of the Middle East which is as unstable as it always led by Iran. This is the biggest worry on the global energy front and is the major reason why other fuel sources need to be developed today.

Long term, climate change and the fact that the Mideast doesn't have unlimited suppliers of oil will come into play. Thus, owning Exxon or Chevron makes sense today. I am glad both are getting into other energy plays and will inevitable be the biggest power companies, no matter what power is used in 10 years from now.