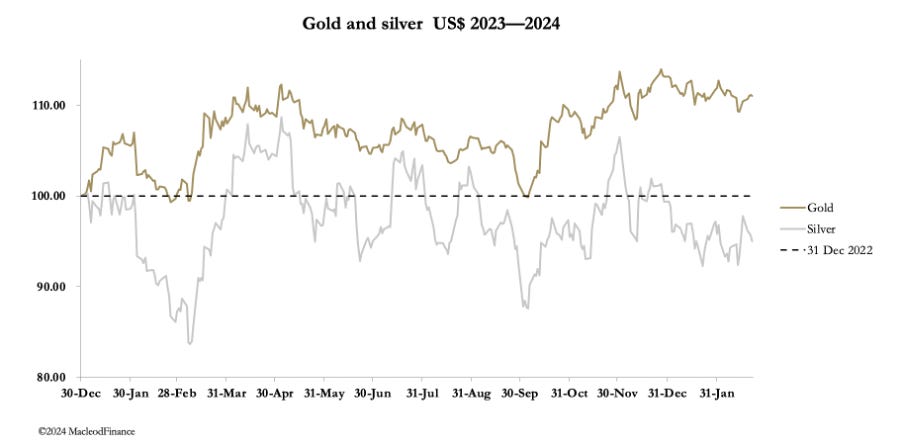

In subdued trading, gold was little changed on the week, while silver eased. In European trade this morning, gold was $2019, up $4 from last Friday, while silver was $22.64, down 77 cents. Comex volume in gold was low, while in silver it was good, reducing to moderate levels in the latter part of the week.

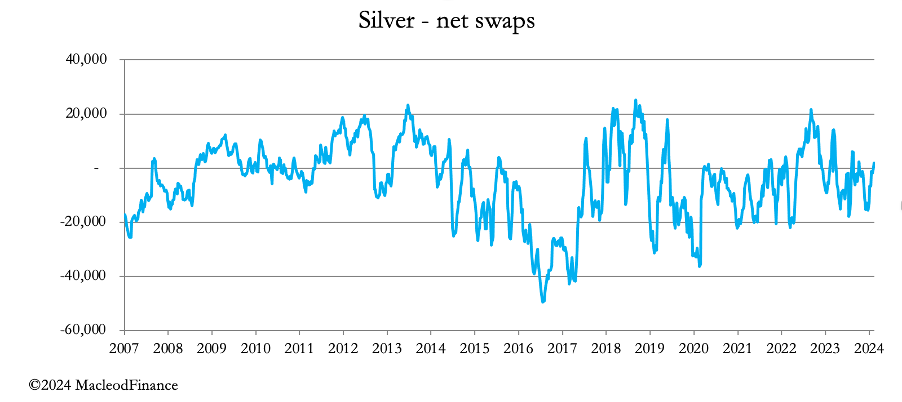

Technical conditions for gold and silver differ radically. In silver, Comex’s Producers & Merchants category is net short of over 31,000 contracts, representing 155 million ounces. This is because over 50% of mine production has silver as a secondary metal to copper, zinc etc., so it makes sense to hedge price volatility. With this category taking the short side, it permits the Swaps to job a more even book, reflected in the chart below.

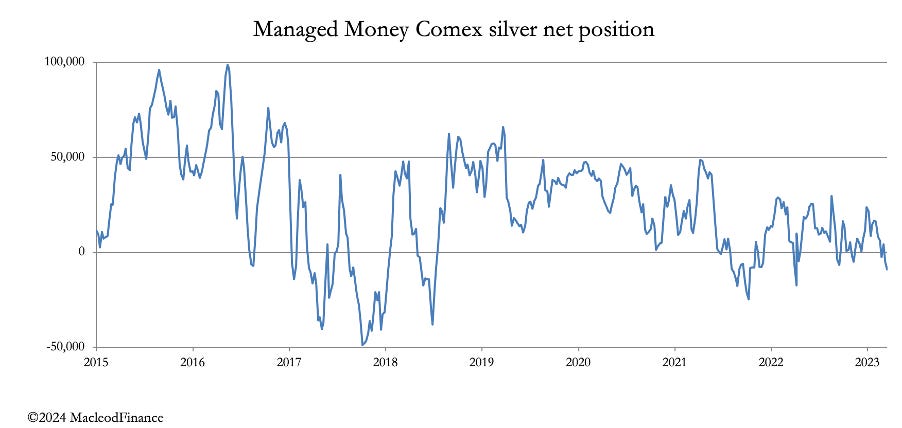

In fact, on the last Commitment of Traders figures (13 February), Swaps were net long of 1,822 contracts, while the hedge funds (Managed Money) were net short of 8,983 contracts.

We can see how this category can easily go even more short, historically as much as 50,000 contracts. So while hedge funds going net short and the Swaps going net long is a good oversold indicator, it is too early to say that silver’s price will find support at current levels. Accordingly, traders would be wise to await further developments.

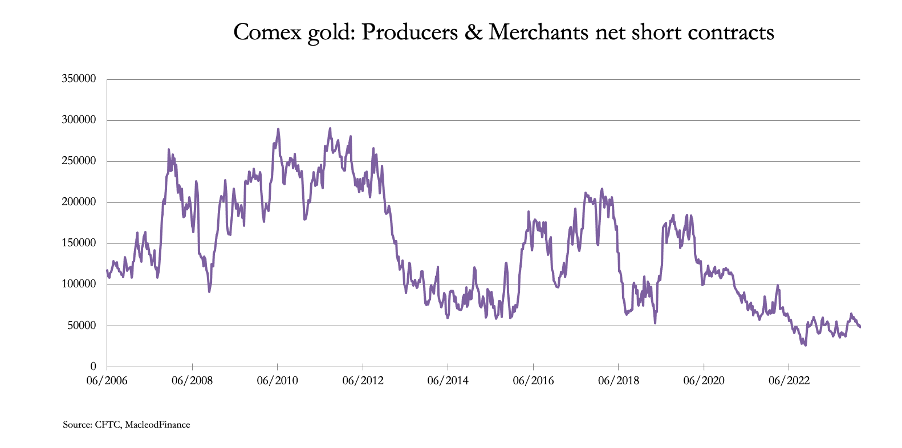

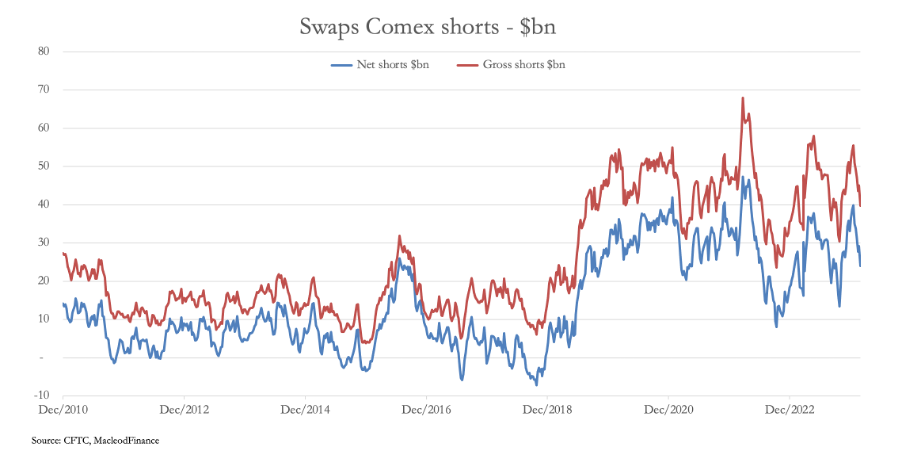

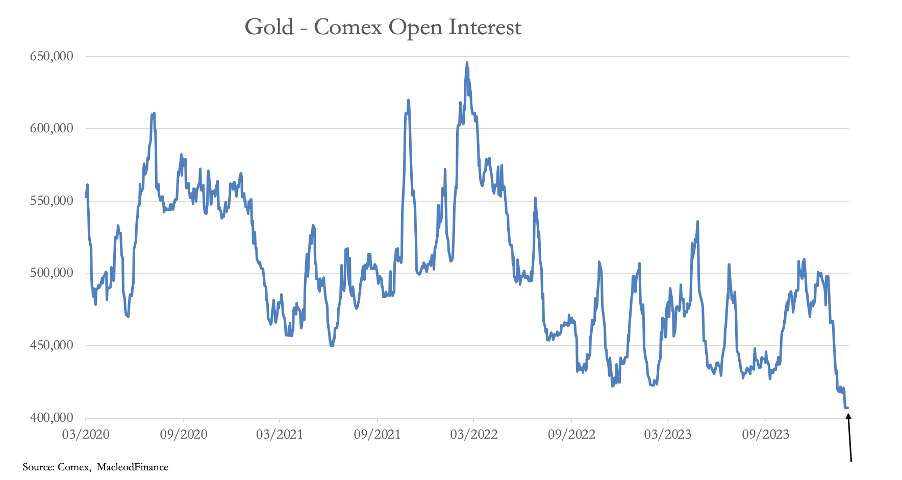

Meanwhile, the position in the Comex gold contract is markedly different. The Producer & Merchant category here is barely net short, compared with the past. With underlying credit and monetary developments likely to guarantee gold’s value, they are in no hurry to hedge. This is plain to see in my next chart.

This leaves the burden of the short side to the Swaps, which is why they cannot close down their short positions:

As can be seen, despite the collapse in Open Interest, gross Swap shorts are $40bn between 23 traders (averaging $1.74bn each) and the longs are $15.75bn between 24 traders (averaging $66 million).

Open interest in this contract has virtually collapsed, which is next.

On this basis, we can say that gold is more oversold than silver, so relative volatility aside, it is the safer hold for traders confirmed perhaps by this week’s relative weakness for silver.

In terms of fundamentals, gold appears to be at a crossroads, as US dollar market expectations are for interest rates to hold up for longer than previously expected. The urgency for a reduction in US interest rates on debt management grounds is widely admitted. But the Fed is dragging its heels, and there are worrying signs of persistent inflation. After all, record US Government budget deficits are continuing to feed currency debasement, and therefore consumer price inflation is unlikely to ease from here. If anything, it can be expected to rise, with dollar oil prices having risen 10% since 6 February.

With US Treasury yields also continuing to rise (the 10-year UST note yields 4.345% this morning, having risen from 3.75% on 27 December) Keynesian money managers will be thinking of the interest rate penalty as a headwind for gold.

In conclusion, it is too early to say that for gold a short-term bottom has been found, and a test of the 12-month moving average at $1965, or even lower trend line support currently at $1880 cannot be ruled out. This technical chart is next.

Of course, technical analysis is not infallible, and those with wealth to protect from a rapidly evolving credit crisis would be wise to ignore it and use this current weakness to accumulate physical gold.

More By This Author:

Massive Bear Squeeze Likely In Gold

Informed Accumulation Of Gold Bullion

It Is Vital To Understand The Legal And Practical Role Of Gold

Comments

Log in or sign up to join the conversation.