Scrooge McSquirrel; Monetizing Polarization; A Convex Play On Gold

Summary

- The 🐿️ is not a gold bug. Read elsewhere for doom porn.

- Whether or not one sees the ‘yella fella’ as a hedge against inflation, deflation, geopolitics, the implosion of the fiat money system or the zombie apocalypse matters very little to us.

- Ironically, the fact that gold is such a divisive and polarizing (almost religious) topic is precisely what creates an asymmetric investment opportunity.

- Waiting for “The Big One” in terms of an outsized precious metals price move is a full-time job (a religious calling even) for some. We have no idea if now is the time and do not want to rehash the big-picture macro arguments. However, we note some interesting developments.

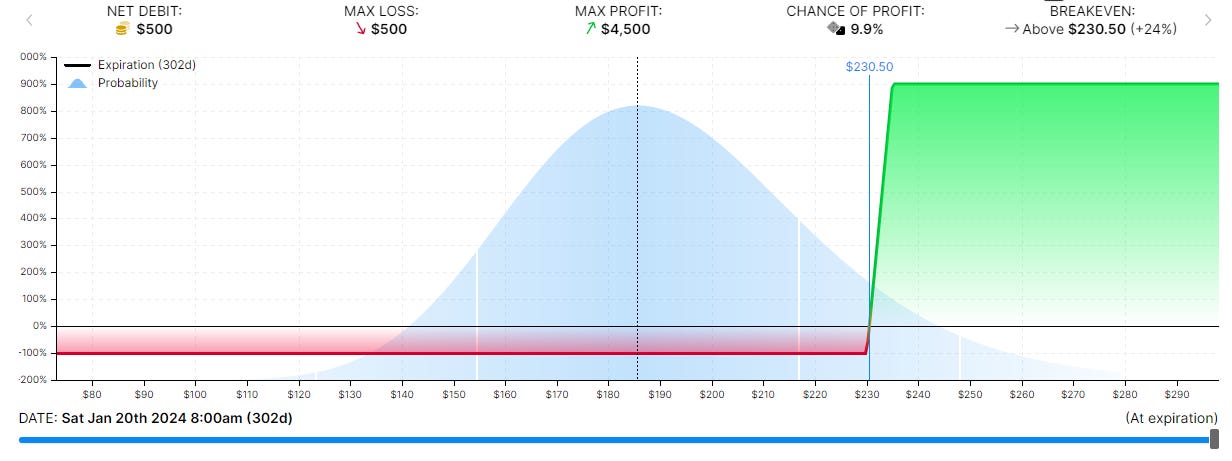

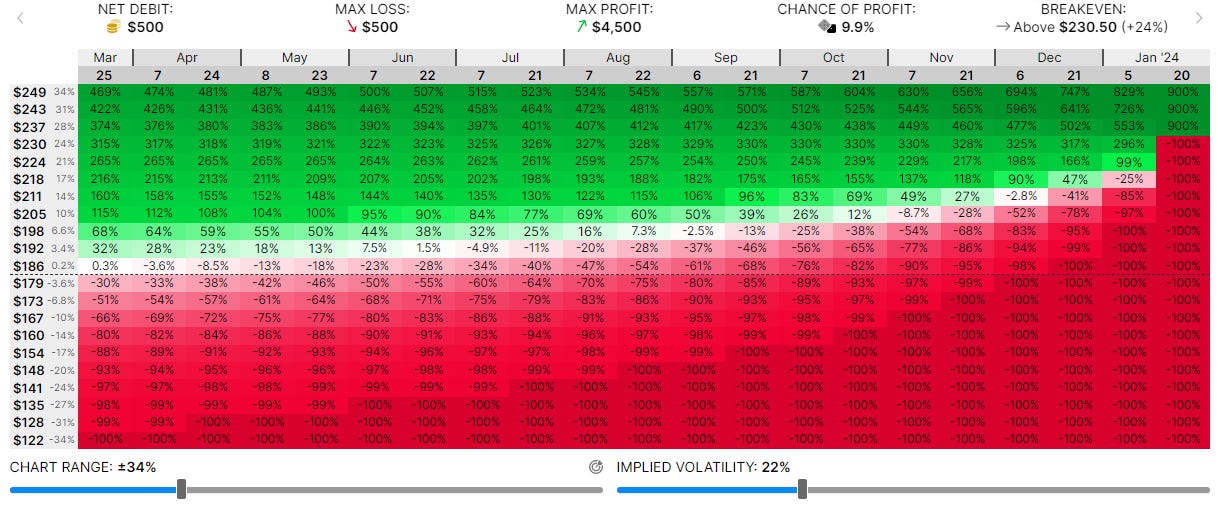

- We have taken advantage of the ‘smile’ in GLD’s implied volatility curve to purchase a US$230/US$235 bull call spread (i.e., a US$5 spread/max payoff in the event that gold has appreciated by c.26% or more by 19th January 2024) for US$0.50 of net premium.

- To the 🐿️, this looks like an attractive set-up from a risk-reward perspective given the current macro backdrop. This is however clearly a highly speculative position. We have sized appropriately.

- Final Thought. Diving into a pool of gold coins like Uncle Scrooge McDuck is a really really bad idea.

Background

Let me clear something up at the outset. The 🐿️ is not a gold bug. You will never find the words “End the Fed!” or “proud Austrian economist” in my Twitter or LinkedIn bios. Sure, I have concerns about the monetary ‘end game’, when we find out the true implications of decades of fiat money printing. Having said that, let's be honest, none of us really know what that looks like. Read elsewhere for speculation and doom porn on that front.

My mates and I used to snigger about “boomer” gold bugs. But we all get older, and this same circle of friends now avidly debates the pearls from Fred Hickey’s monthly “High Tech Strategist” as soon as it hits our inboxes (pro tip: Fred’s letter is mainly about precious metals miners these days, not tech).

Anyway, the best thing about gold bugs is that they are not nearly as irritating as bitcoin maximalists. With one exception (YouTube link).

It’s hard to believe that my great mate Krakie’s famed debate with that particular ‘exception’ took place nearly a decade ago, during the last time Putin was conducting “special military operations” in Ukraine. Please watch the video. The ‘debate’ goes ad hominem from minute 1 and is hilarious. And because I am such a good friend, here is what they both look like these days 👇😉.

At the risk of accusations of apostasy, I am going to say that the investment case for gold is a bit of a chameleon. However, whether or not one sees the ‘yella fella’ as a hedge against inflation, deflation, geopolitics, the implosion of the fiat money system or the zombie apocalypse matters very little to us. Ironically, the fact that gold is such a divisive and polarizing (almost religious) topic is precisely what creates an asymmetric investment opportunity.

The Theory

A link for those that do not get the Jennifer Anniston reference.

A core hypothesis for maintaining an allocation to gold in your portfolio is as an insurance policy against extreme events. The theory goes that this allocation to gold will be valuable on the morning after the zombie apocalypse when the rest of your financial assets are a smoking pile of charred debris.

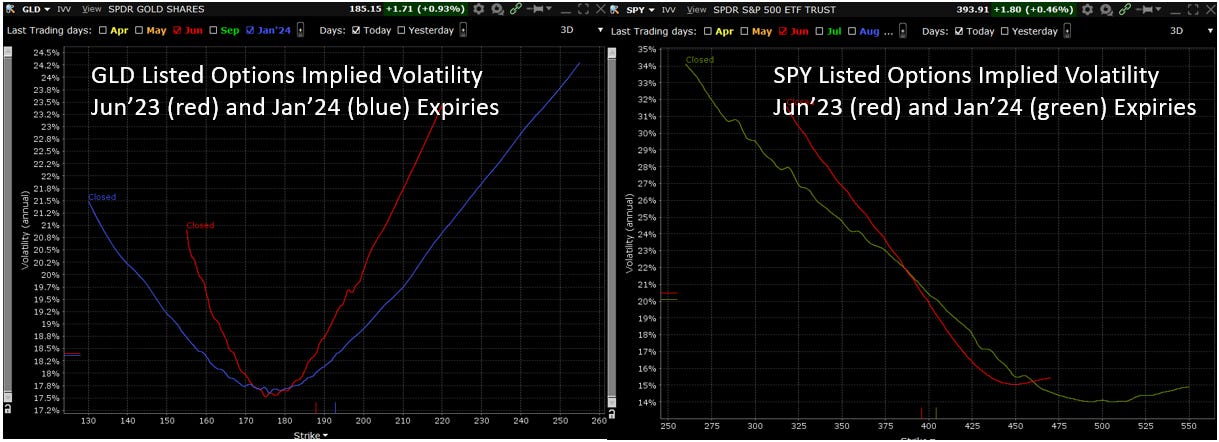

The charts below show the implied volatility (effectively a measure of cost) of listed options of the GLD (gold, on left) and SPY (S&P500, on right) ETFs. Strike prices of the option on the x-axis, implied volatility on the y-axis. As you can see the shapes of the curves for the two ETFs are very different.

(Click on image to enlarge)

The GLD curves are a ‘smile’. The SPY curves are a ‘smirk’. Source: Interactive Brokers - Implied Volatility Viewer

Explaining the potential reasons for this distinction is an essay in its own right, but the simplest explanation in layman’s terms is as follows:

- Long holders of equities are happy to ‘pay up’ for insurance against extreme downside moves in the value of their portfolio. They also often sell call options (upside exposure) in order to enhance the yield on their holdings.

- Conversely, long owners of gold own it 100% in order to retain exposure to the extreme upside event. They would never sell out-of-the-money call options in order to clip a bit of current income from the sale of option premium. As a consequence, call options on gold get (relatively) more expensive the further out of the money you go. ‘End of the world’ insurance is expensive.

The ‘smile’ of gold’s implied volatility is what creates the opportunity. You can opt to take exposure to part (but not 100%) of the upside move in the gold price via a bull call spread.

In such a spread, you are long an out-of-the-money call option and short a further out-of-the-money option to the same expiry. Because of the ‘smile’, the net option premium you pay is handsomely subsidized by the ‘short call’ leg and so ends up being a small fraction of the spread between the two strikes. We illustrate this with real numbers in the implementation section below.

Why now?

Waiting for “The Big One” in terms of outsized precious metals price moves is a full-time job (a religious calling even) for some. I have no idea if now is the time and I do not want to rehash the big-picture macro arguments. However, we do know the following:

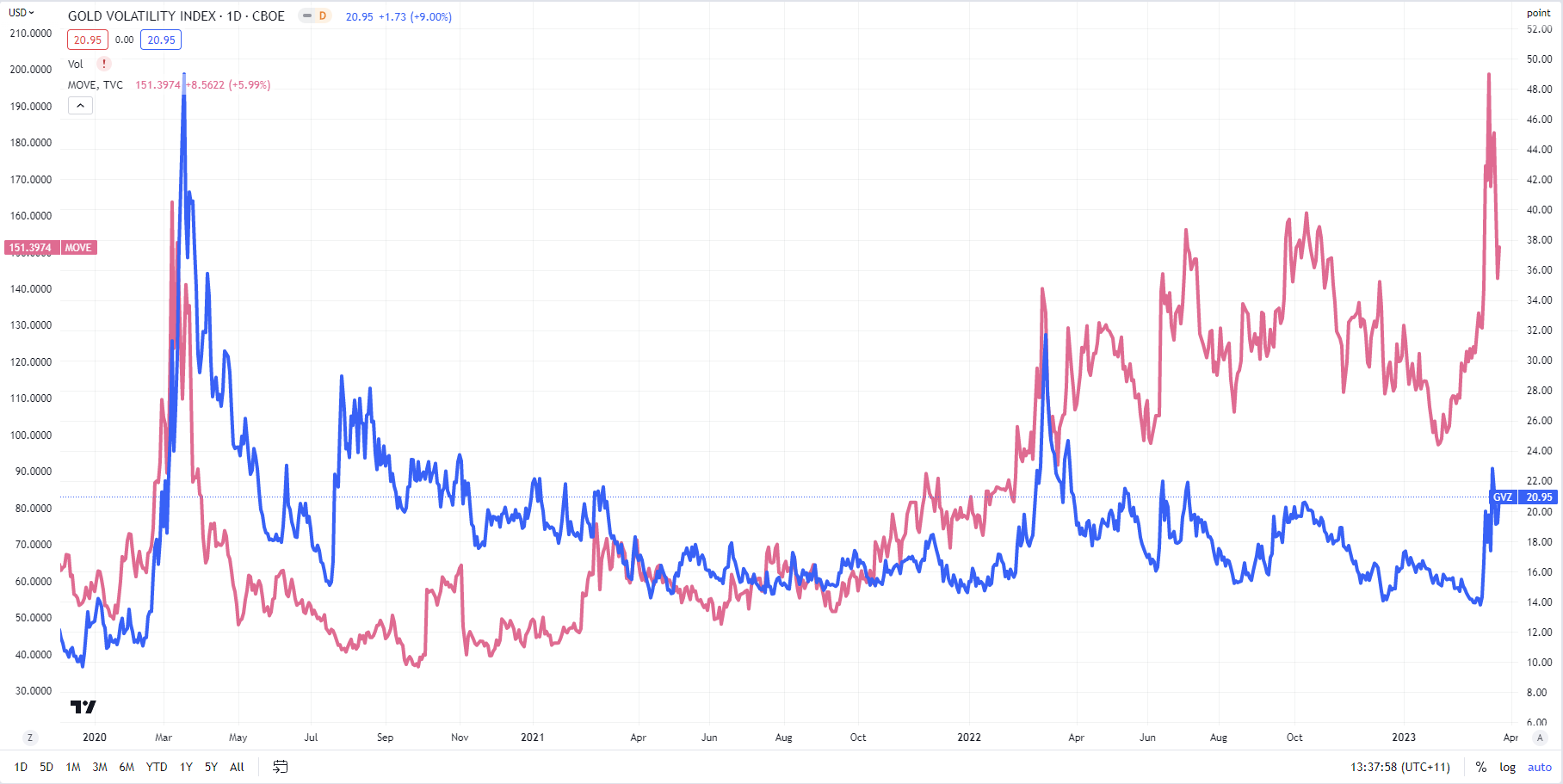

The financial system feels a little shaky in the wake of the collapse of Silicon Valley Bank and Credit Suisse’s shotgun wedding with UBS. The US treasury market is showing signs of extreme stress. Gold has noticed.

(Click on image to enlarge)

US Treasury Volatility (MOVE, pink) vs Gold Volatility Index (blue). Source: Tradingview.

The geopolitical soup is pretty hot and the “bad guys” are in a desperate hunt for alternatives to US dollar hegemony. Physical gold has backed currencies in the past. A long shot, but people are talking about it on the ‘doom porn’ sites.

Image credit: Piyush Gupta

The biggest gold buyers of all, the world’s central banks, possibly as a function of the previous point, are in the market with a vengeance - with a notable acceleration in 2022 after the start of the Ukraine war.

Source: VisualCapitalist.com

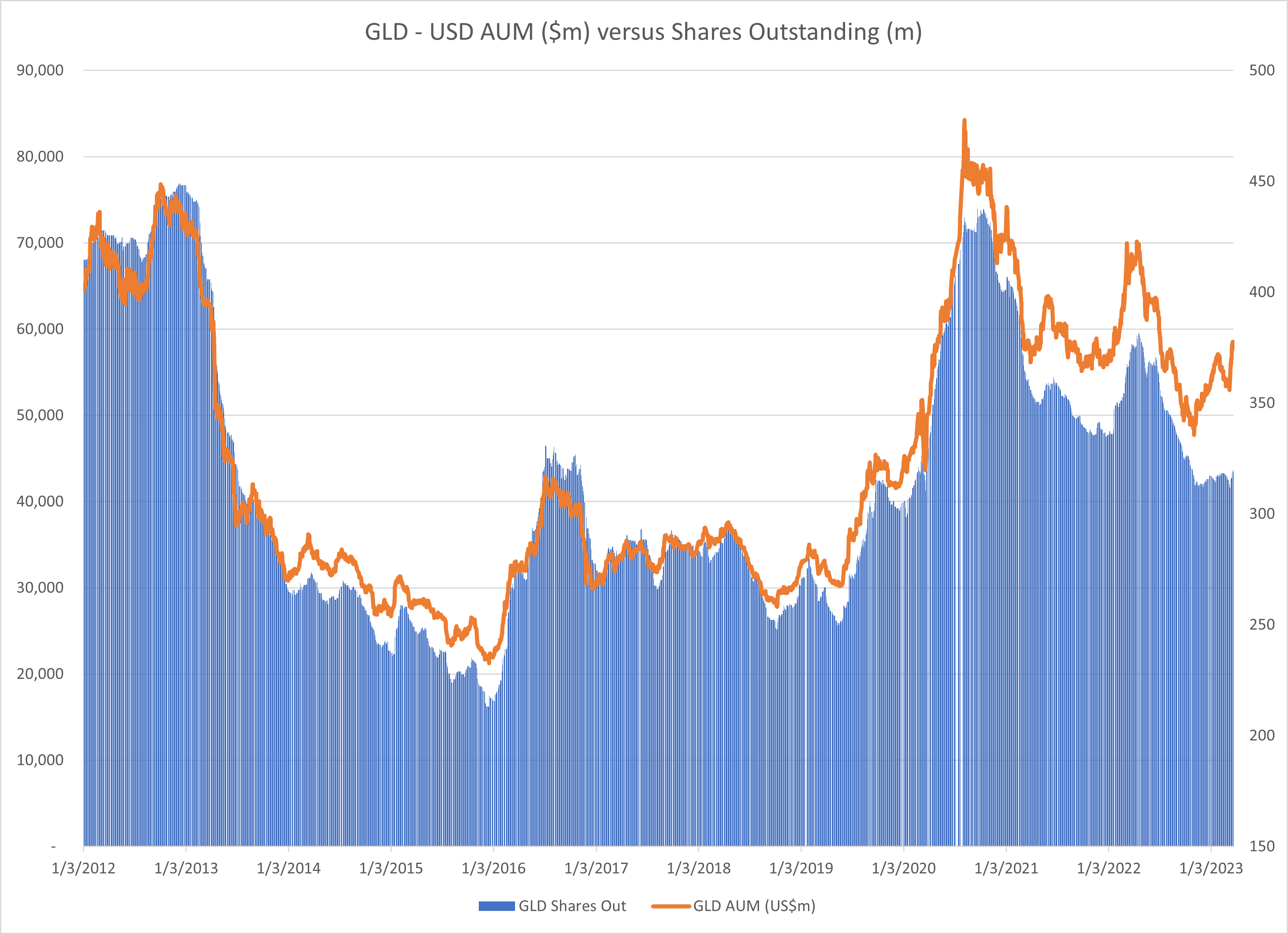

Investment demand may be back. Barely perceptible in the chart below, but outflows from the GLD ETF have finally stalled out and have started to reverse. We have seen inflows in the past couple of months (US$520m in the second week of March alone).

(Click on image to enlarge)

SPDR Gold Trust (GLD). Assets under management and total shares outstanding. Source: Koyfin.

Gold has already been doing a pretty good job as a store of value in the past year. In particular, if you are Australian, British, or Japanese.

(Click on image to enlarge)

Gold (XAU) as a cross-currency versus USD (blue), EUR (turquoise), JPY (green), GBP (orange), and AUD (purple). Source: Tradingview.

Is the fourth time a charm? Will gold break into the uncharted territory of new all-time highs?

(Click on image to enlarge)

GLD ETF weekly chart. Source: Tradingview.

On the daily chart, the trendlines are almost fully restored following the February correction. In the short time frame, however, this chart does look overbought (with extreme relative strength readings).

(Click on image to enlarge)

GLD daily. Source: Tradingview.

To my mind, the biggest downside risk right now is a return of the “US Dollar Wrecking Ball” that we saw in 2022 - the scenario in which all assets (equities, rates, credit, and commodities) sell off simultaneously as people scramble to raise US dollar cash. Impossible to discount but less likely now that any continued monetary tightening by the central banks will be at a more subdued pace and scale than what we saw last year.

(Click on image to enlarge)

DXY (weekly chart). Source: Tradingview.

Implementation

As indicated above, we are implementing this Acorn via a bull call spread on GLD, the SPDR Gold Trust. This ETF is backed by physical gold and is highly liquid. The ETF also benefits from very actively traded listed options.

We have taken advantage of the ‘smile’ in GLD’s implied volatility curve to purchase a US$230/US$235 bull call spread (i.e., a US$5 spread/max payoff in the event that gold has appreciated by c.26% or more by 19th January 2024) for US$0.50 of net premium.

(Click on image to enlarge)

GLD weekly chart, annotated with $230/$235 spread (pink box). Source: Tradingview.

As ever, we have saved the structure on OptionStrat. You can study the structure in detail and toggle the assumptions via this link.

Payoff at Maturity

(Click on image to enlarge)

Illustrative Payoff over time

(Click on image to enlarge)

To the 🐿️, this looks like an attractive set-up from a risk-reward perspective given the current macro backdrop. This is however clearly a highly speculative position. We have sized appropriately.

Final Thought

Sorry to be a killjoy, but as a responsible 🐿️, it is only fair that I remind you that diving into a pile of gold coins is a really bad idea. If this is something you did not know instinctively, then I suggest that you head the words of James Kakalios, Ph.D., a professor of physics at the University of Minnesota.

“The question really isn’t whether someone could swim in a mass of gold. They could not. It’s more a matter of how badly they’ll be injured in the attempt. Gold is a very dense material. Diving and swimming into it, even with lubricant, might be analogous to trying to shove your hand into a deep bowl of M&Ms.”

Am glad we cleared that up.

More By This Author:

CoCo Pops: Only Half Price? Some Thoughts On Bank Capital

Squirrel In The Matrix

Ben Graham’s Electric Car

If you act on anything provided in this newsletter, you agree to the terms in this disclaimer. Everything in this newsletter is for ...

more

Good araticles and cute photos. What's tthe significance of the Blind Squirrel name though?

Thanks Ayelet! Even a blind squirrel finds an acorn (a good trade) from time to time! 🐿️👍

Lol, love it!