Image Source: Pixabay

In case you haven’t heard, precious metals, particularly gold, have risen sharply this year. Of course, whenever any asset class experiences a more speculative melt-up, investors are quick to rationalize why “this time is different.” In stocks, it is about “artificial intelligence” and “data centers.” The cryptocurrency community believes all fiat currencies will fail and everything will move to the digital asset. But when it comes to gold, the voices have grown loudly, claiming the reasons for the rise are debasement of the dollar, de-dollarization, and soaring debt levels.

For example, Bloomberg lumped all three worries into one article.

“Beneath the surface of the short-term ups and downs of financial markets, a longer-term repricing of multiple assets may be underway as investors seek to protect themselves from the threats posed by runaway budget deficits.

Those who believe in it are pulling away from sovereign debt and the currencies they are denominated in, fearful their value will be eroded over time as governments avoid tackling their massive debt burdens and even seek to add to them.Further fuel is coming from speculation that central banks will face increasing political pressure to hold down interest rates to offset what governments owe — and in the process fan inflation by continuing to crank out cash.“

The problem with the Bloomberg article is that it was unresearched and just a recycling of already prevalent myths. In this article, we will go through each gold myth and present the data behind the analysis.

Myth 1: Central Banks Are Hoarding Gold to Get Out of Dollars

This gold myth is repeated across media outlets and investor circles. It suggests that the global financial system is rapidly moving away from the U.S. dollar, and a recent “chart crime” by Statista further adds to the crowd’s conviction. To wit:

“Central banks have crossed a symbolic line: their combined gold reserves now exceed their U.S. Treasury holdings for the first time in nearly three decades. The crossover underscores a gradual diversification away from dollar-denominated securities and toward hard assets.”

The problem with this chart is that it is only a function of price differences. Yes, bond prices have declined in recent years as rates have risen, and gold prices have increased. However, what Statista wants you to believe is that this represents a significant change by Central Banks to buying gold and selling Treasuries, which, in reality, is not the case. As shown below, the actual change in gold as a percentage of foreign reserves has primarily been a function of price increase. Over the last 5 years, Central Banks have only increased the amount of gold they own by roughly 5%. In other words, they have not switched significantly to buying gold.

They have also not been selling Treasuries to “get out of US dollars.” Instead, while they have been adding to gold holdings as the price has increased, they have also bought Treasury bonds in record amounts, with foreign holdings now exceeding $9 trillion.

The reality is that while Central Banks have accumulated some gold over the last 5 years, it isn’t a function of “fleeing the dollar.” Instead, they are rebalancing their reserves, adding gold as a form of diversification, particularly if the dollar is weaker than their own currency, not as a replacement. In a recent survey by the World Gold Council, only a minority of central banks said they plan to reduce their U.S. dollar exposure, and even fewer intend to sell U.S. Treasuries. Most still see the dollar as the most liquid and stable reserve currency globally. The interest in gold is more about risk management than ideology.

There are also the practical constraints. Gold is hard to store, expensive to transport, and doesn’t pay interest. Furthermore, gold offers no yield, so they depend solely on price changes to protect their reserve balances when holding the asset. Most critically, Central banks can’t swap extensive holdings of U.S. Treasuries for gold without triggering a liquidity crisis in global markets. While there has been a modest increase in the demand for gold, mostly from speculators, it’s incremental with respect to Central Banks and is not signaling the collapse of the dollar system.

History supports this. Even during the Cold War, when ideological lines were clear and distrust in Western systems was high, countries didn’t entirely abandon the dollar. Gold served as a partial hedge, not a full replacement. Today’s environment is no different. Central banks aren’t dumping dollars; they manage risk across a broader portfolio.

Myth 2: The Death of the Dollar and Fiat Currencies Is Here

The claim that fiat currencies are on the verge of collapse, and that the dollar is finished, is primarily ideological. It’s popular with hard money advocates and gold bugs, but this gold myth has no historical or institutional basis.

First of all, fiat currencies don’t die in a day. Legal systems, state power, military force, tax policy, and institutional trust underpin them. If the dollar were truly being debased, you’d see a very different set of outcomes:

- Capital fleeing U.S. assets (stocks, bonds, gold, cryptocurrencies)

- A collapse in Treasury demand.

- A breakdown in global trade settled in dollars.

Instead, we see the opposite. The U.S. dollar remains the default unit for global trade, cross-border settlements, debt issuance, and central bank reserves. Treasury demand remains robust, as shown above, and the dollar is still used in 80% of global transactions and represents nearly 60% of international reserves. Central banks, sovereign wealth funds, and institutional investors continue to hold and accumulate U.S. assets. So, while media pundits scream about a “loss of trust,” global capital continues to support the dollar,

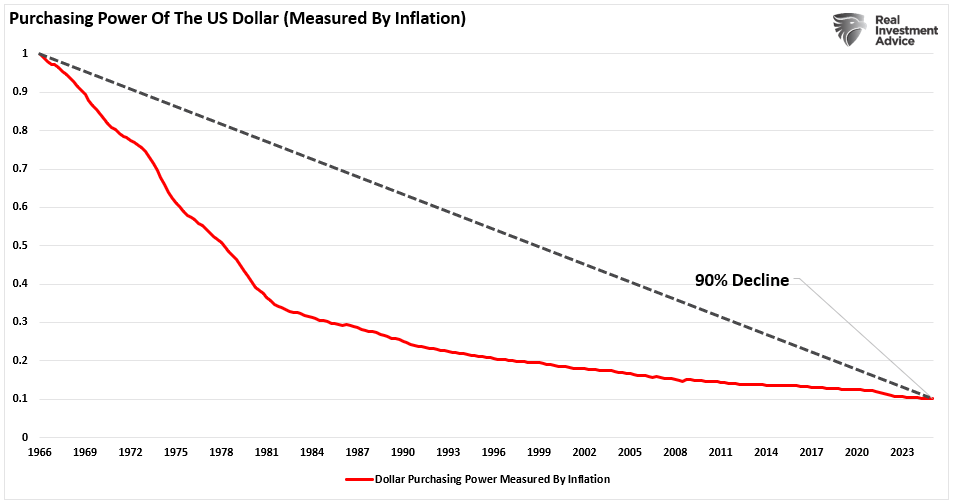

When people say the dollar is “dying,” they often conflate two things. First, they mistake a decline in purchasing power for systemic collapse. Inflation erodes the value of money, but it doesn’t mean the monetary system is failing. Yes, if you have held dollars in a “coffee can” since 1960, you have certainly lost purchasing power due to inflation over time. That is because the economy has grown sharply since then, leading to high standards of living.

However, this is why we “invest” dollars into assets that consistently produce above-inflation rates of return over time. The chart below illustrates the returns on investments in stocks and gold since 1960. It is easy to see which has been a better long-term hedge against the loss of purchasing power. In fact, as shown, gold failed to outperform inflation until 2006.

(Click on image to enlarge)

Second, they assume that any new currency alternative, whether gold, the yuan, or a digital asset, will instantly replace fiat. The evidence doesn’t support that. For example, the Japanese Yen and the British Pound have gained exposure in foreign exchange reserves in recent years, along with the Chinese Yuan, as those economies have prospered. However, they still only make up a minor share of the total. The euro remains burdened by fragmentation and political dysfunction and has declined in recent years. In other words, no single currency or system is poised to replace the dollar.

Even gold, which served as a reserve asset in the past, lacks the infrastructure to become a dominant medium of exchange. Gold-backed systems require convertibility, centralized control, and strict monetary discipline, which is politically difficult in modern economies dependent on flexible credit and fiscal spending.

I am not arguing that fiat currency systems do not face challenges. They do, especially from inflation and debt. But those pressures create adjustments, not extinction.

Myth 3: Gold Is Surging Due to the Debt and Increased Money Supply

This narrative gets traction every time gold moves higher. Commentators argue that rising U.S. debt levels and persistent budget deficits erode confidence in the financial system, prompting investors to seek refuge in gold. The argument is straightforward: more debt equals more risk, resulting in increased gold demand. The problem remains the same as with all the other myths: the data does not support it.

Gold prices are not directly tied to government debt levels. If they were, gold would have surged in the 1980s and 1990s when debt-to-GDP ratios climbed steadily. Instead, gold stagnated for nearly two decades. The connection is more nuanced. Gold tends to respond to changes in interest rates, inflation-adjusted returns, and perceived instability. Not debt ratios in isolation.

But there is more to this story. U.S. debt-to-GDP ratios have improved in recent years after surging during the COVID crisis when federal debt peaked near 121 percent of GDP in 2020. As of 2024, it has declined to roughly 118 percent, according to data from the Congressional Budget Office. While that number remains historically high, the trend has moved lower, not higher. Part of that decline is due to stronger nominal GDP growth. The U.S. economy has expanded faster than expected, driven by resilient consumer spending, corporate profits, and job growth. If GDP continues to grow, debt levels become more manageable. A larger economy can support a larger debt load without triggering market panic or inflation.

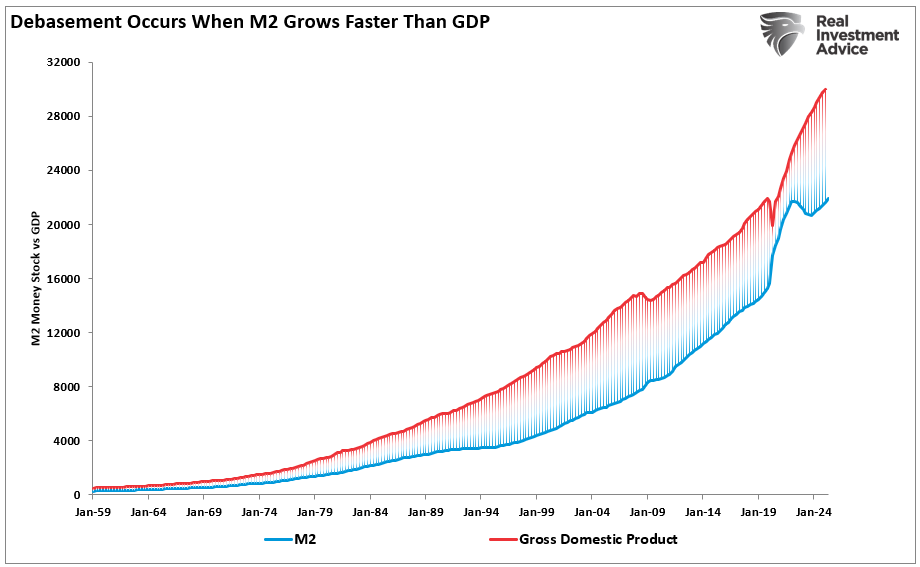

The other side of the debt argument is that an increased money supply leads to higher gold prices. Again, the data doesn’t support that claim either. As we discussed previously:

“It’s easy to point to M2 charts and scream “debasement. “ However, the money supply must grow as the economy grows. If it doesn’t, deflationary risks emerge. Therefore, the key is whether money creation exceeds economic growth in a sustained way. Since 1959, the money supply has grown in alignment with economic growth.”

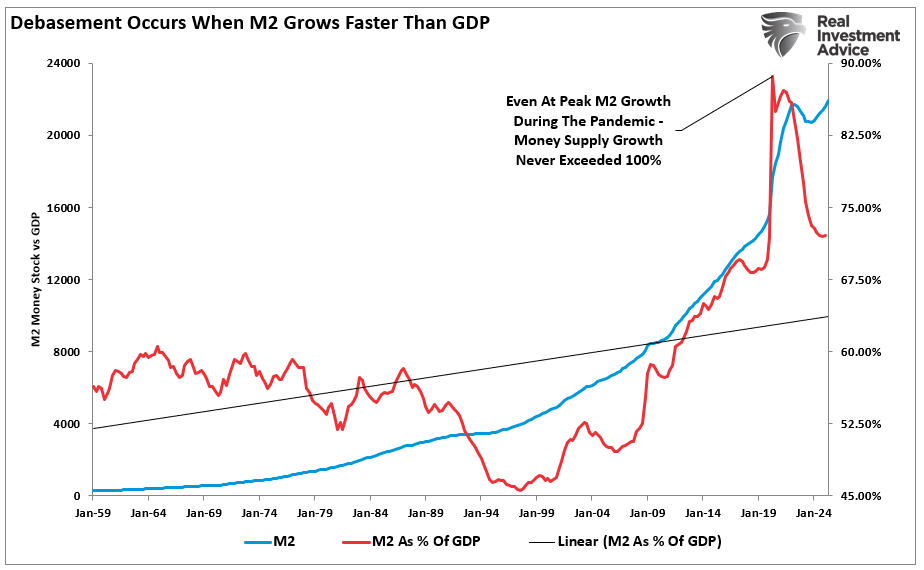

“A better way to assess this is by comparing M2 to GDP. Historically, the two have tracked closely. Even during the COVID shock, M2 as a percentage of GDP remained below 100%, meaning money supply growth was broadly aligned with economic output. Today, that ratio is falling, not rising.”

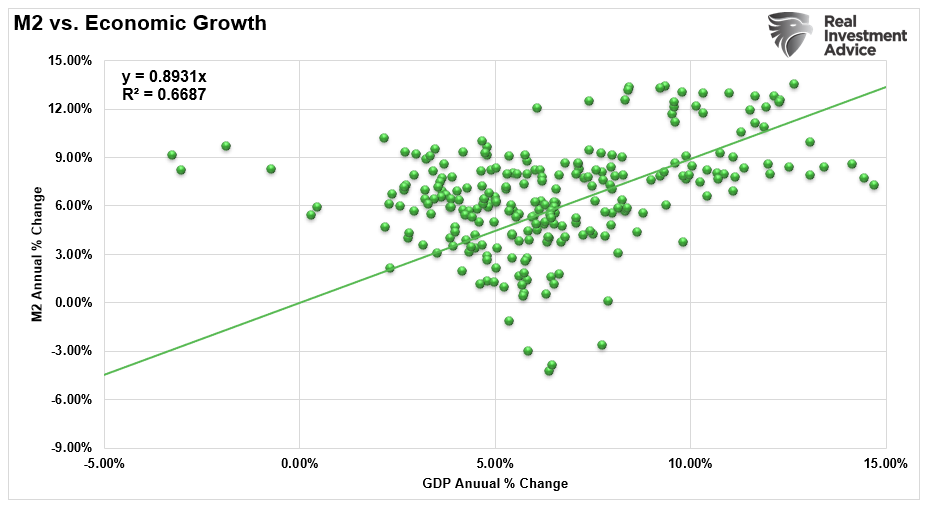

“The reality is, as you would expect, that the growth rates of M2 and the economy are highly correlated.”

Most importantly, markets understand this. Bond yields, although volatile, have not spiked in a disorderly manner and have been declining, not rising, over the past year. Treasury auctions continue to attract buyers, and, as noted above, foreign demand for U.S. Treasuries remains robust. You’d expect widespread U.S. government asset sales if debt drives the gold rally. That isn’t happening. This was a point made by Bloomberg’s Joe Weisenthal in Maybe ‘Debasement’ Isn’t The Best Way To Put it,

“It’s not true that all real assets are surging in price. For instance, real estate is not doing particularly well. This is the ultimate “hard” asset, and yet, prices are barely going up. Now, you might say that homes are weird, because mortgage rates are high, and so forth. But on the other hand, one of the premises of the debasement trade is that rates are being kept artificially low. So in theory, there should be a lot of demand to borrow at these levels. But apparently not so much.

And speaking of rates, the 10-year yield is now trading close to its lowest levels of the last 12 months. If you weren’t paying attention, you’d think that bonds have been some terrible investment, and that rich countries are losing control over the long end of the curve. But the chart says otherwise. 2025 has been an excellent year for Treasuries.”

The reality is that gold’s surge is a speculative price-chase feeding frenzy supported by these “myths” to rationalize and justify paying increasing asset prices. But such is always the nature of a speculative feeding frenzy, whether in gold, stocks, or cryptocurrency.

What This Means for Investors

While it is true that gold has performed well in recent years, it also experiences prolonged periods of underperformance. Gold does the same, like stocks, which cycle through bull and bear markets. As with all investments, it is crucial to manage the risk of ownership accordingly. The current trend is not guaranteed to continue, and given the extreme technical deviations, it is almost a certainty that it will not.

(Click on image to enlarge)

As a gold investor, our advice is to discard the “gold myths” and focus on what ultimately matters.

- A strong U.S. dollar rally. Gold is priced in dollars, which is also a flaw in the debasement trade. Gold becomes more expensive for foreign buyers when the dollar strengthens against other currencies, reducing demand.

- U.S. economic growth continues to surprise to the upside. This will reduce the debt-to-GDP ratios and attract more foreign capital into U.S. dollar-denominated assets.

- Widening interest rate differentials. If interest rate differentials widen in favor of the dollar, it could trigger a broad-based move back into dollar-denominated assets, hurting gold.

- A continued decline in inflation. Gold often benefits from fears of rising prices, even if it’s not a perfect hedge. If headline CPI numbers continue to fall and inflation expectations decline, the urgency of owning gold as a protective asset may fade. Disinflationary forces, such as tighter credit, falling commodity prices, or global growth slowdowns, could reduce the inflation risk premiums embedded in gold.

- A drop in bond yields. A drop in yields, especially real yields, can hurt gold under the right conditions. Gold tends to do well when real yields are negative or falling. However, if bond yields fall because growth is weakening and investors flee to safety, gold may not benefit. In that environment, Treasuries often outperform as the preferred risk-off trade. Gold could lag.

- Investor sentiment is a significant driver of gold prices. If market psychology shifts, due to improving macro data, reduced geopolitical stress, or even a broad equity rally, flows into gold ETFs and futures can reverse quickly. Momentum fades. Positioning unwinds. A shift in narrative is often all it takes to break the trend.

Gold is not immune to market cycles. It’s a volatile asset driven by shifting narratives and capital flows. If you’re buying gold today, understand what’s supporting the price, and what could shake that support loose. Treat gold as a hedge, not a core growth asset.

Manage your exposure accordingly, and leave the “gold myths” at the door.

More By This Author:

Dow Theory: A Concerning Divergence Or Artifact?Liquidity Concerns Put An End To QT

Rebasing The Dollar: Another Look At The Debasing Narrative

Comments

Log in or sign up to join the conversation.