Gas And Oil Firms Will Be Cheaper In 8 Weeks – Here’s How To Profit

There is entirely too much optimism over the recent accord to curtail production signed by Russia, OPEC and some tertiary non-OPEC producers. Mexico, a non-OPEC member, attended the meeting and set its production target at 1.94 million barrels per day (bpd) output, which OPEC hailed as solidarity. This was not in solidarity with OPEC! It was because bureaucracy and neglect have meant declining production from the state-owned oil giant Pemex, anyway.

The United States did not attend, nor did Canada. And neither agreed to slow their production. Tellingly, neither did China or Brazil. Why is this important? Well, let’s see… the United States is the most technologically advanced gas and oil producing nation, where companies are able in some areas like the Permian Basin to make a profit pumping oil at $35. Canada has the largest oil sands resources, where oil is effectively mined. It is processed, not drilled for. Assuming breakthroughs in technology allow such mining to keep the environment safe as it is mined, there is no exploration and production risk; it is all right there, out in the open. This, along with its conventional oil reserves, places Canada among the top 4 or 5 nations in terms of oil resources. And China probably has the most shale gas resources of any nation.

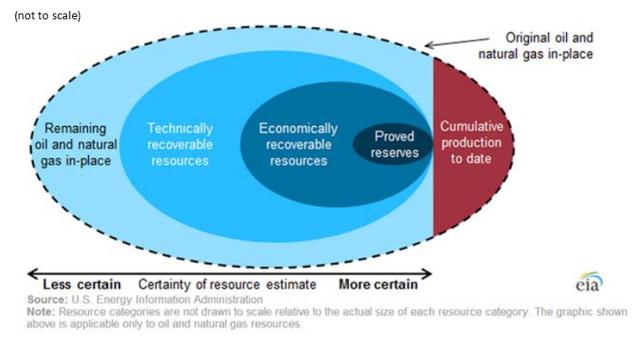

“...Canada is among the top 4 or 5?” “...China probably has the most shale gas reserves ?” What gives here? Don’t we know who has what? Isn’t this “settled science?” Absolutely not. It all depends upon what your definition of “is” is. Or, in this case, proven reserves, probable reserves, potential reserves, technically recoverable reserves, and many other variations on a theme. See the chart below for a good example of the more commonly-used terms.

(click to enlarge)

The US Energy Information Administration (EIA) is the source for the estimate that places China #1 in shale gas resources, with 1 quadrillion, 115 trillion cubic feet (tcf) of wet shale natural gas. That’s a whole bunch. For comparison, Argentina comes in second at 802 tcf, Algeria third at 709 tcf and the USA just fourth at 623 tcf, with Canada and Mexico nipping at our heels for the next two positions.

The EIA also says that the USA is #1 in tight oil (from shale) resources with 78 billion barrels (bbl) followed by Russia at 74 bbl and China at 32 bbl. However, you must always read the fine print when reading such predictions. In this case, the EIA was looking at “unproved technically recoverable reserves.” “Technically recoverable” only means that we have the technology to extract the product. It doesn’t mean it is economically feasible to do so!

That’s why, if you go to 20 different independent sources (as opposed to the hundreds of websites that just publish the EIA’s numbers) you’ll find 20 different estimates. Worse, the 2015 estimate from the same source may be radically different in 2016, even within the same category of technically proven or any other reserves. The landscape changes, as do the reserve predictions, based upon ever-better technologies.

If we are serious about determining who today, not tomorrow, has the wherewithal to deliver the energy and not go broke doing it, we need to look at the proven (or at least proven and probable – “P2”) technically and economically recoverable reserves, those which can be recovered and sold at current market prices.

Who REALLY Sits in the Catbird Seat When it Comes to Energy?

Understanding the above shifts the favorable balance of power away from the Middle East, including Iran, where governments must buy their citizens’ loyalty with massive subsidies and therefore must see the oil or its gas equivalent at somewhere between $60 and $130 a barrel. It also places Russia in a whole new light, given its extreme over-dependence on exporting oil and gas. Russia is economically a third-world nation dependent on selling the commodities its massive land mass provides and a first-world nation in the technical prowess of its people.

China looks very good from an energy standpoint if you look only at its technically recoverable reserves. But to be economic, shale production needs copious amounts of water. China is one of the least secure nations from a water standpoint. Most of their water comes from the Tibetan Plateau, which is why there is no chance, not even a snowball’s chance in hell, that the Chinese autocracy will ever willingly relinquish control of Tibet. You simply cannot separate realpolitik from economics. No matter how much shale gas China has, or doesn’t have, it doesn’t have the water to get it out of the ground economically, at least not in any size.

But China has all that Russian gas coming in, right? If anyone can remember all the way back to November 2014, certain US newspapers opined that Russia, in a brilliant coup, had agreed to sell China 2 trillion cubic feet of gas over a 30-year period. Once again, many bemoaned, them Gawdless Rooskies and Chicoms were getting together to end-around the US. Not really. Did I mention you cannot separate realpolitik from economics? It all depends upon pricing.

At this point, the Russians demand “x” and the Chinese are only willing to pay “X minus Y.” Russian monopolies need to satisfy the State because they only exist at the pleasure of the State. Ditto Chinese monopolies. So if there’s no give in this give and take, who benefits? That would be US and Canadian producers. An early harbinger of this may be that the largest suppliers of LPG to China are already US companies, more nimble and more capable of controlling their costs, pricing and, indeed, their destiny than are the Russian and Chinese monopolies. I imagine we’ll see a day when Russia lowers its prices or China increases its deals with the US, Canada, and Australia. Their rising consumption and attempts to wean themselves from coal leave them no other choice.

Energy firms in the US and Canada, along with those from nations like Australia , the UK and Norway, have huge advantages over lumbering state-owned behemoths that must satisfy the state’s demand for income. Companies in the US can negotiate leases with separate individuals who own the rights to what lies sub-surface on their property. Some will always be ready to deal; that is never the case when one arm of The State is negotiating with another arm of The State.

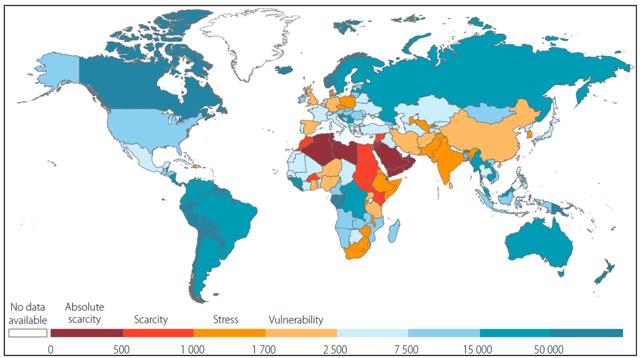

The US and Canada are home to the most advanced and most numerous independent operators as well as the drilling contractors with the most experience, expertise and advanced technology. We have an amazing pipeline and distribution capability that will only get better as we continue to develop our infrastructure. And finally, we have water. If a nation like China truly wants to increase production by hydraulic fracturing, they need water.

I’ve spent 30 years analyzing renewable and non-renewable energy, but another area of research and writing has been about water. Welcome to the New World, i.e. the Western Hemisphere. Led by Canada, the entire Western Hemisphere is blessed with fresh water. So is the Lucky Country, Australia, and neighbor New Zealand — as is Russia and all of Scandinavia. Canada gets about 88,000 cubic meters of water (or some 88,000,000 liters per inhabitant) of “total renewable water resources” every year. Even the much more populous USA gets nearly 10,000 cubic meters per person. China? Thanks mostly to Tibet, all of 2,000 cubic meters or so.

(click to enlarge)

So What’s All This About The OPEC Deal Collapsing?

Prices can be held artificially high for only so long. OPEC and Russia are hoping it lasts long enough to enter into long-term contracts with buyers with deep pockets who are willing to stand by their deal if prices collapse. Good luck with that!

Gas pricing and oil pricing today, have always been, and always will be about supply and demand. On the supply side, hydraulic (“operated by the pressure of a fluid”) fracturing has multiplied U.S. production by an order of magnitude. Canada has all the water it needs to develop the oil sands — and is an honest partner that stands by its commitments. Mexico has opened its offshore areas to US and multi-national players. It’s a new day, a new dawn for North American energy firms. Supply is increasing in the most stable, nearest-to-home parts of the world. Demand, beyond a few successful economies, is not keeping pace.

What OPEC and Russia came up with is a temporary fix to their long-term problems; a bureaucratic, statist plan to try to disrupt true market dynamics. Worse, it depends upon honor among thieves. History bodes against them: OPEC members have consistently cheated their within-OPEC competitors. And now, there are 11 non-OPEC nations, most run as socialist and/or autocratic enterprises, whose economies are sick and will be sicker unless world gas and oil demand outstrips world supply. Non-OPEC signatories like Evo Morales’s Bolivia and “The Sultan’s” Brunei control their nations with whatever they have and for most, what they have is oil or gas. This keeps their otherwise-restive populations at arm’s length and allow the Friends of (Fill in the Blank) to live the good life. Production caps will last until the first one of these feels the pain of not having enough vigorish to distribute in the form of subsidies and bought-and-paid-for loyalty.

The worst is likely yet to come for many of these autocrats of the negotiating table. 99% of the charts and research on “who has the oil” tell us Venezuela, with just under 300 billion barrels (bbl) of proven reserves, is the world’s luckiest nation when it comes to oil resources. But you now know there is a huge difference between proven reserves and a nation’s ability to technologically and economically get that oil out of the ground. Economically, Venezuela is a basket case. Ever since the United Socialist Party of Venezuela, under the reign of Hugo Chavez, took control of the government in 2002, the country has gone backwards. It will take years before any outside firm will be willing to take the country’s word that they will be repaid for fronting all exploration and production costs on their own.

The world’s second-largest owner of proven reserves, according to the consensus, is Saudi Arabia. Where to begin here? Of Saudi Arabia’s 10 million plus barrels per day of production, they expend 1 million on desalination. (In the 1970s there was a subterranean reservoir the size of Lake Erie under the Saudi Arabian desert. The Kingdom bled it dry trying to prove they could become self-sufficient in agriculture, producing wheat at 3 times what the market would pay.) Now they have launched a bold new campaign to reinvent themselves yet again. But every person they educate or give an opportunity to raises those people up and places them closer to parity with the extended royals. The Saudis fear this more than they fear low oil prices. Better to keep buying loyalty with subsidies.

I could go on with the travails of many of these producing nations. I think by now you see why I believe the “deal” reached at the end of 2016 will last every bit as long as other previous ones. You can’t replace the law of supply and demand. Instead let me share with you what I believe is the most realistic appraisal of who really has the most oil reserves in the world. And also has more than we currently know in natural gas. And the most that is technically and economically retrievable.

Rystad Energy is an independent energy consultancy based in Norway but has offices in the UK, Singapore, Russia, Brazil and the US. I have followed their work with great interest since 2010 or so. Their conclusions may well shake up what we know, and don’t know, about real reserves.

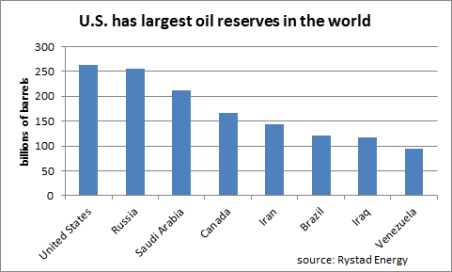

Before I provide their conclusions, please note that they aren’t even assessing whether these reserves are economically viable, or even proven. Even standing on their own as just “reserves” they conclude, as you can see from this chart, that Venezuela is a distant 8th in total reserves — and that the USA is really the top dog globally. Rystad estimates that the U.S. holds 264 billion barrels of oil, more than half of which is located in shale. That is more oil than is found in Russia, and considerably more than Saudi Arabia.

Rystad disagrees with the EIA estimate of Venezuela’s reserves of 298 bbl’s, noting that there simply has not been enough work done to verify that those reserves are actually there. They are based upon outdated and likely wildly optimistic projections that if something is found at point A on the periphery and point B in the middle and point C at the other periphery, that all in between must be exactly like those three points. Seismic technology has shown the folly of such linear thinking! Instead, Rystad estimates that Venezuela only has about 95 billion barrels, which includes Rystad’s estimate for as-yet-undiscovered oil fields.

Moreover, Rystad notes accurately that there is no global standard to measure oil reserves from one country to another. Some countries report proven reserves, using conservative estimates from existing oil fields. Others (like Venezuela,) include “undiscovered” reserves!

Rystad has done the heavy lifting and applied a similar set of metrics to all countries. It doesn’t matter whether their metrics are the ones that will be used in the future if better ones are found as technologies change. Theirs is the first apples-to-apples comparison, rendering the process both more transparent and more accurate. Too many “authoritative” reports like BP’s Statistical Review, which many analysts rely upon, are nothing more than a compilation of what the host nations say.

You say you want to see more jobs created in America? Rystad’s research concludes that Texas alone could have 60 billion barrels of oil. By the way, Rystad’s rankings change when reviewing only the “proved and probable” category, also called 2P. In this case, Saudi Arabia comes out on top with 120 bbl’s and the entire US is dropped to 40 bbl’s. I am personally far more optimistic. I debunked the Peak Oil argument in a paper 30 years ago — it applies to individual wells, not to the entire planet. So far I’ve been correct. And I imagine, as our seismic and 4-D mapping improve, as do our recovery techniques, it will be the same story for the next 100 years, by which time solar and wind will have made a strong addition to the energy production picture.

Is There Anything Special To Buy?

My readers must be tired of me saying, “Yes, but not yet.” Let me amend that statement to “Not yet, but yes.” I have made the case in previous articles that OPEC members cheat. Russia cheats. Every tin-horn autocrat with oil in his backyard will cheat as long as he can get away with it. So I am still biding my time. I still spend hours every day poring over articles, research, 10-Ks, and such to make certain I understand the energy business inside and out.

Nothing has changed in my opinion that US and Canadian firms are the companies I most want to invest in. Nothing has changed in my belief that the mid-tier firms are likely to offer the best combination of cash flow, survivability, agility and alacrity.

My short list is therefore comprised of the following firms I will buy when the time is right. I believe that time is likely to be in this quarter as the OPEC-Russia-et al agreement falls apart and oil prices decline temporarily at the end of heating season in the Northern Hemisphere. I may place smaller orders above these prices but here are my new “if I can steal them here, I will” prices as well. All are GTC.

BUY AMERICAN: 300 APC at 48, 500 DVN at 33, 550 RRC at 29, 1500 SWN at 9.60, 2000 CHK at 6.

BUY CANADIAN: 500 CNQ at 25, 400 IMO at 30, 1200 ECA at 10.50 and 500 SU at 28.

BUY MULTI-NATIONAL: 200 CVX at 90, 200 XOM at 78, 350 TOT at 43, and 300 RDS-B at 44. < >

Disclaimer: I do not know your personal financial situation, so I encourage you to do your own due diligence on issues I discuss to see if they might be of value in your own investing.(Or, ...

more