AgMaster Report - Thursday, Dec. 14

JAN BEANS

(Click on image to enlarge)

Last week, the mkt was ostensibly “under wraps” – anticipating the Dec WASDE on Friday 12-8-23 at 11 am! But that report turned out to be a ho-hum, non-event with #’s little changed from November! The real news -surprise, surprise – was of course the weather in Brazil – which moderated all week as forecasters ended up taking rain “out of the forecast”! This resulted in a short-covering rally from just under $13.00 of over 30 cents! Aiding this upsurge was a steady flow of exports all week in terms of flash sales, Mon Inspections & Thursday sales! The mkt was apparently not convinced that the rains had markedly improved the extreme dryness in N Brazil! The stocks started the year tight were not augmented by a 4.1 BB crop – roughly unchanged from last year! And exports should continue to flourish!

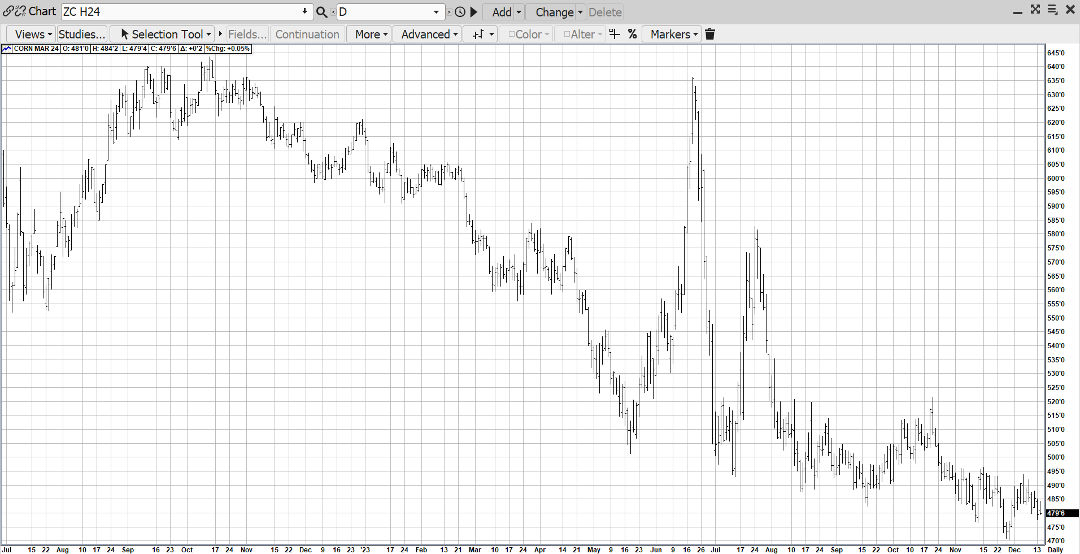

MAR CORN

(Click on image to enlarge)

As is evident from the above chart, Mar Corn has been confined to a tight trading range for several months – even with fundamentals suggesting an uptrend! US Corn is the cheapest anywhere, the US dollar is on a 4 month low, the US farmer is not selling, the crude is sharply higher, the short open interest is sizeable & prices are $1.50 under the summer highs! We feel the 15.2 BB crop is dialed into prices & that adverse South American weather will lower their bean & corn crops – tightening global stocks! It’s only a matter of time before active exports rally corn out of its current range!

MAR WHT

(Click on image to enlarge)

8 consecutive higher closes in Mar Wht spawning a 90 cent rally – signified a trend change in the woebegone wheat mkt to the upside! Fueling the fire were 4 flash sales of wht to China 2 weeks ago! But the mkt got ahead of itself – correcting 40% of that rally last week! Now the mkt is awaiting global crop updates from Argentina & Australia & hopefully more export interest from China!

FEB CAT

(Click on image to enlarge)

In 3 short months, Feb Cat relinquished its entire $33 dollar rally (196 -163) which had taken 12 months to accumulate! Sticker shock & much cheaper alternatives ultimately created demand destruction for the once high-flying market! But we feel the down was overdone – as it often is in commodity mkts, and that the lows last week just under 163 will be seasonal lows! Supporting that contention is the fact predicted production for the first 3 quarters of 2024 is slated to be 5-10% under this year! Plus holiday beef demand should support the mkt thru year-end!

FEB HOGS

(Click on image to enlarge)

Feb Hog’s direction of late has been inextricably linked to China’s Hog Mkt – which since their seminal announcement several weeks ago of hog excess, has been ravaged by mass hog herd liquidation & declining cash prices! It’s been a “double jeopardy” for the US hog producer – as not only is China not buying our pork but they are liquidating part of their supply! However, the “bleeding stopped” yesterday & today, when the mkt challenged the contract lows but was unable breach them – leading to a $4.00 rally today! This seems to confirm the 65.80 low on 11-28-23 is indeed the seasonal low!The mkt has also been aided by positive “outsides” with a record DJI, a sharply lower US $ & a $2.00 higher crude!

More By This Author:

AgMaster Report - Tuesday, Dec. 5

AgMaster Report - Thursday, Nov. 30

AgMaster Report - Wednesday, Nov. 22