Image Source: Pixabay

“I used to think that if there was reincarnation, I wanted to come back as the President or the Pope or as a .400 baseball hitter. But now I would like to come back as the bond market. You can intimidate everybody.” James Carville, Advisor to Bill Clinton

President Trump is trampling everywhere, threatening tariffs, cutting back on immigration, and, more importantly, raising the specter of an ever-deepening budget deficit. Investors have expressed relatively mild interest in the tariff issues as it relates to inflation. The stock market continues to hold up well, the US dollar index remains elevated, and long-term interest rates remain steady, post-election. Now, the next test will be at budget time, this spring, when the US Federal government puts out its call to the bond market to finance which, assuredly, will a historically large deficit. Investors remain decidedly uncertain as to whether to worry about a return to inflation from deficit spending or to a recession from major cutbacks.

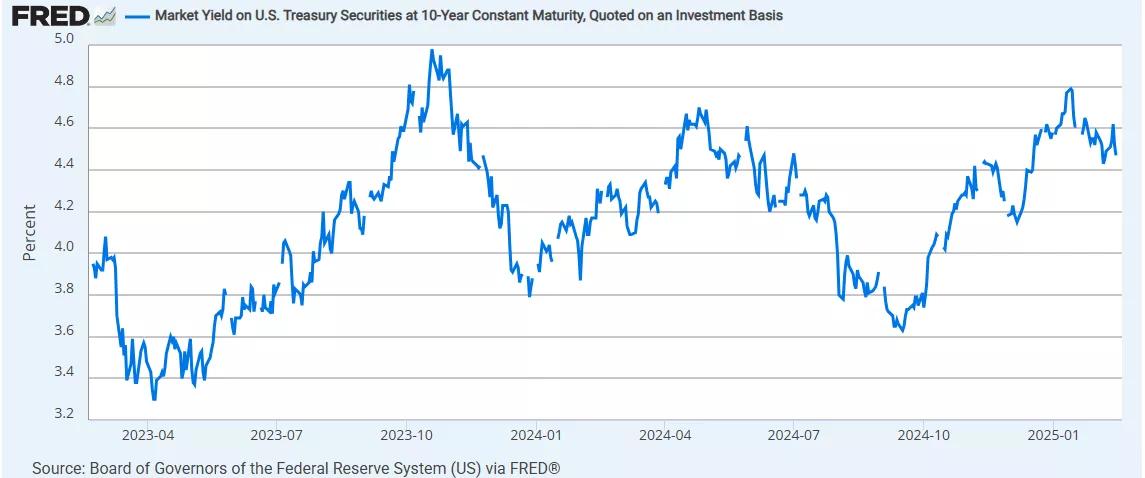

The cross currents are unmistakably been felt in the bond market. The yield on the benchmark 10-year Treasury bond shot up more than 100 bps, hitting 4.8%, 3 months post Trump’s election. Simply put, the anticipated inflation from US tariffs, running at a high 25% raised the prospect of an across-board increase in producer prices. Bond investors bided up yields and sought immediate protection against inflation. Perhaps the market did overreact a bit, nonetheless, the 10-year rate is hovering around 4.6%. The impact of this rate level is being felt throughout the economy, especially in the home mortgage market which continues to experience sagging demand. Nonetheless, the Fed has made it clear, on more than one occasion, that it is in no hurry to lower its policy rate, taking a very careful “wait and see” approach.

(Click on image to enlarge)

Now, all eyes are on the size and depth of the US fiscal deficit. Confusion reigns at the moment. On one hand, the Administration has adopted a slash and burn approach taken towards Federal government employment levels and programs. On the other hand, huge tax cuts are been drafted in Congressional planning committees.

Current estimates by the Congressional Budget Office, call for government spending to exceed revenue by $1.9tn, or 6.1 % of US GDP for the year. The US continues to run one of the world’s highest budget deficit ratios, well in excess of its long-term average of 3.8%. These estimates do not include any proposed Trump tax cuts or spending plans yet to be fleshed out. Legislators are preparing tax cuts that would generate as much as an additional $ 4.5tn increases in the US debt ceiling.

The US Treasury market has shown great resilience in absorbing a near doubling in size over the past decade. Many observers turn to this past performance as a sign that the market will, once again, hold up well and take on ever greater debt loads without affecting interest rates.

As so often cited, the quip by Nobel prize winner, Herbert Stein, “if something cannot go on forever, it will stop”. Not a trivial observation, but one that will be considered as this Administration attempts to do the near impossible, namely reduce the US deficit.

More By This Author:

Steel And Aluminium Tariffs Are Bound To Fail A Second Time AroundTrump Clearly Blinked, Backing Off On Tariffs Against Canada And Mexico

The US-Canada Trade War Starts In Earnest: The Risks To The US Are Substantial

Comments

Log in or sign up to join the conversation.