Image Source: Pixabay

Happy 2026! We bet you imagined the start of the new year would be much quieter. You’re not alone. But we believe that we’ve only had a taste of what’s to come. Too many issues have been smoldering beneath the surface or behind the curtain for too long. Well-known issues that should have been on the table for discussion long ago—and yet have been repeatedly ignored.

What can we expect in 2026? Above all, developments that do not correspond to the current consensus. We are still a long way from having analyzed everything down to the last detail – and yes, we are already nervously biting our nails. Nevertheless, our initial conclusions point to five developments that are surprising, contradict expectations, and perhaps only appear logical at second glance:

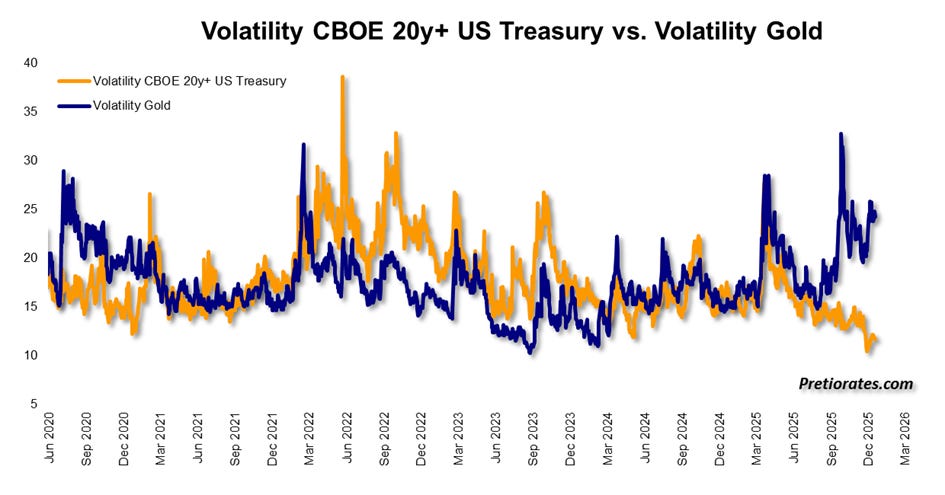

1. Where is the volatility in bonds?

For obvious reasons, the volatility of gold and bonds tends to run fairly synchronously. Gold has fluctuated significantly in recent months, sometimes erratically – a classic signal of impending major changes. After all, uncertainty is the key selling point for gold.

And bonds? They continue to sleep soundly. Volatility in government bonds is at a multi-year low. But we strongly doubt that this hibernation will last…

(Click on image to enlarge)

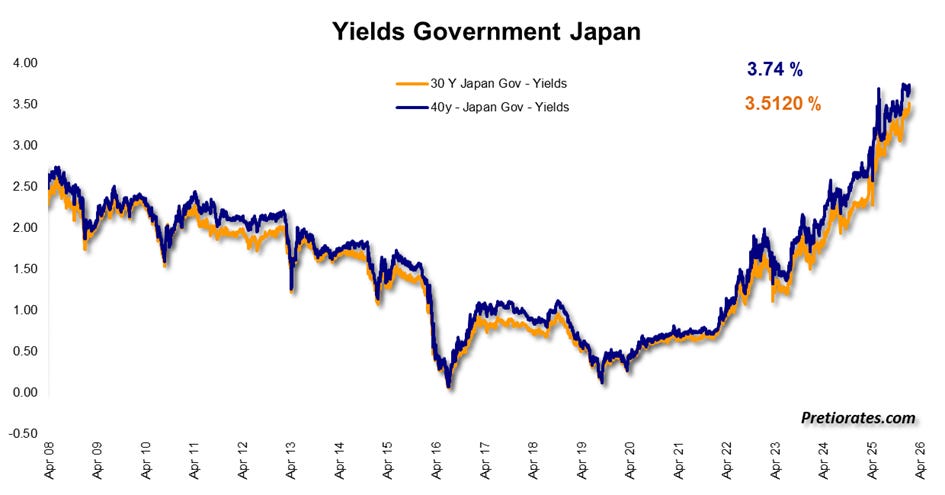

2. Rising interest rates in Japan are causing turmoil in the financial markets

And where might volatility in the bond market first reawaken? We have already discussed the yen carry trade several times. No one knows the exact volumes, but we are probably talking about trillions. For years, money was borrowed at ridiculously low interest rates in yen and invested elsewhere with higher returns.

With interest rates rising in Japan, this game is over. Cheap money is being withdrawn, loans must be repaid – and this capital is being withdrawn primarily from other government bonds around the world. Even the thrifty Japanese themselves will probably prefer to invest in their own country again in the future when interest rates rise...

(Click on image to enlarge)

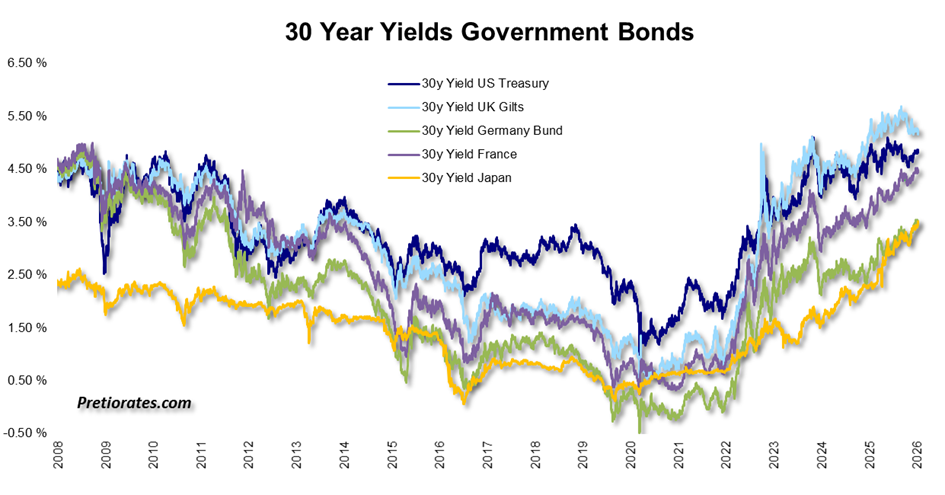

3. Government debt is coming into the spotlight – initially in Europe

We don’t need to say much about political developments. Europe is becoming less and less influential on the global political stage, but many national leaders continue to present themselves as great statesmen – and behave accordingly in fiscal terms.

The bill is likely to come due soon, as interest rates continue to rise. Whether France, the most heavily indebted country, is affected first or, surprisingly, Germany, is hardly relevant. The debt virus is likely to spread rapidly, as all countries are closely intertwined – including the UK, despite Brexit.

(Click on image to enlarge)

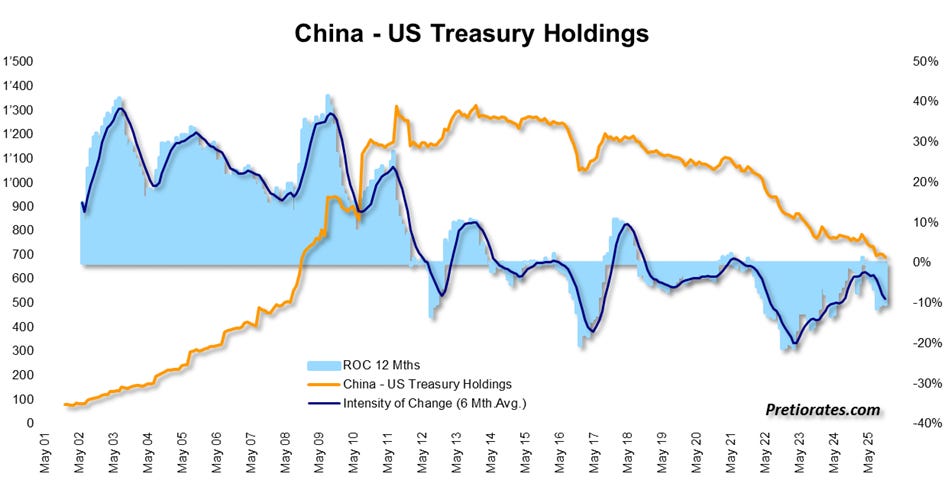

This could unleash an unexpected dynamic with capital fleeing: Where to? Obviously to the US – where else? The consequence: The US, itself heavily indebted, can once again postpone its problem, China’s accelerated reduction of US Treasuries remains inconsequential, and the US dollar benefits additionally from the flight from Europe.

(Click on image to enlarge)

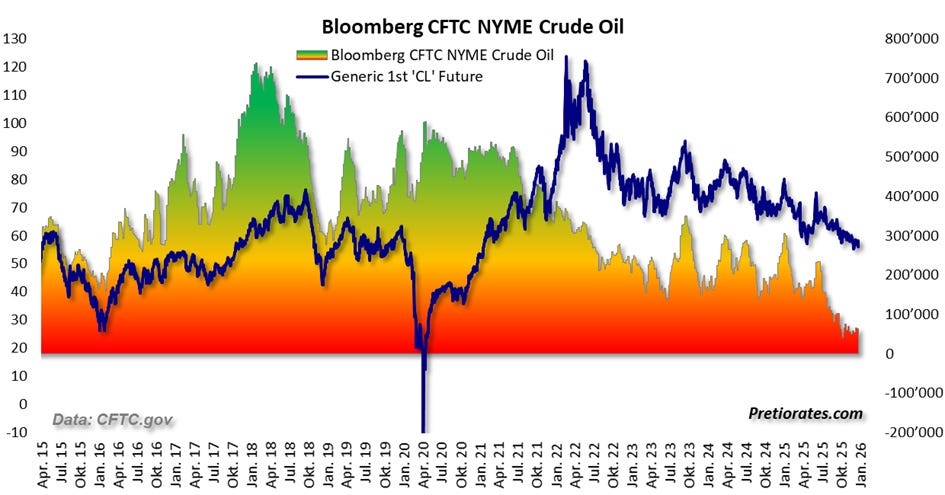

4. From Ashes to Energy: Oil’s Comeback

The US government has brought about regime change in Venezuela. No, it hasn’t – it has merely removed the head of state. The regime itself continues to exist and is effectively back in the saddle with the vice president.

US oil stocks jumped by around 10%, but these gains are likely to evaporate quickly. Corporations such as Chevron, Exxon, and Occidental will first demand comprehensive assurances before investing. And even then, it will take years for the infrastructure to be rebuilt and for higher production to be possible.

At the same time, there are increasing indications of possible new attacks on Iran – initial preparations are reportedly underway.

What is remarkable is that hardly anyone is currently bullish on oil. Once everyone has sold, there will be no buyers left. And if the geopolitical fuse is lit, the oil price is likely to react accordingly. Just as an aside: China sources a large part of its oil from Venezuela and Iran. Will they stand idly by and watch?

(Click on image to enlarge)

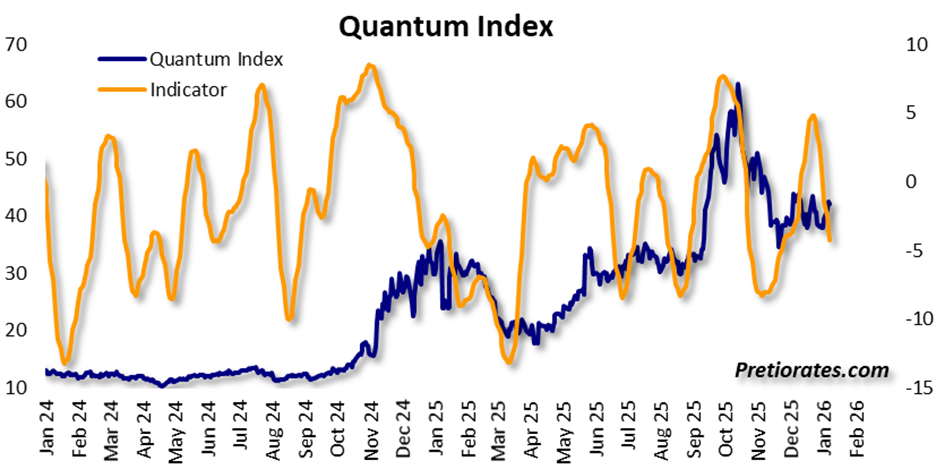

5. The AI bubble will not burst – because quantum computers are entering the stage

We admit it openly: in purely mathematical terms, the investments made by many AI companies seem absurd. At first glance, they will never pay off. But AI will change the world more than the internet ever did. And who still remembers internet pioneers like AOL, Netscape, AltaVista, or MySpace?

Pioneers go bankrupt in most revolutions. This was already the case with computers before the internet. Who still remembers Commodore, NCR, Honeywell, Digital Equipment?

The AI race is not about a single company winning all the gold medals. It’s about which country provides the companies that are at the forefront. Those who are not involved have already lost.

When the computing power of quantum computers is added to artificial intelligence in 2026, the pace will increase dramatically once again. In 2024, quantum computing was still considered science fiction. In 2025, it seemed realistic for the first time. In 2026, it should become clear that the topic is reality – and an acute security policy problem.

(Click on image to enlarge)

Quantum computing and AI together will bring about incredible things. Along with all the positive effects, unfortunately there will also be some not-so-great ones. If you haven’t looked into quantum computers yet, we recommend Julia McCoy’s YouTube channel.

Finally, a quick look at the price of silver:

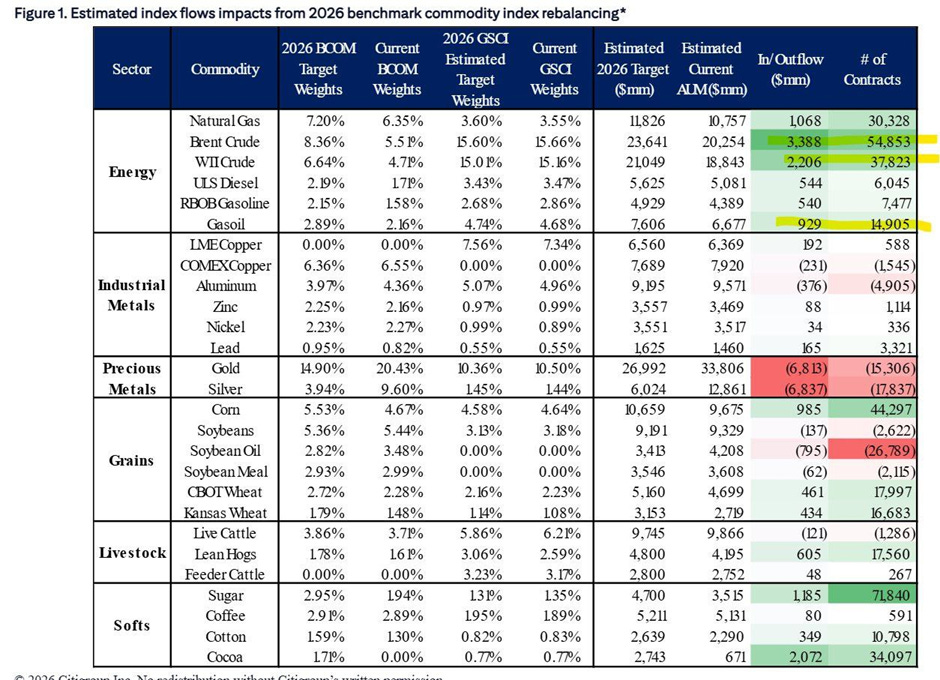

The rebalancing of the two commodity indices, Bloomberg BCOM and Goldman Sachs GSCI, has begun and will continue until January 18. Several hundred billion dollars in assets are based on these benchmarks. Due to the sharp rise in gold – and silver in particular – precious metals have achieved a massive overweight in portfolios, which will now be reduced within about ten days. Citigroup estimates that around 17,837 futures contracts will have to be sold in the silver market alone.

(Click on image to enlarge)

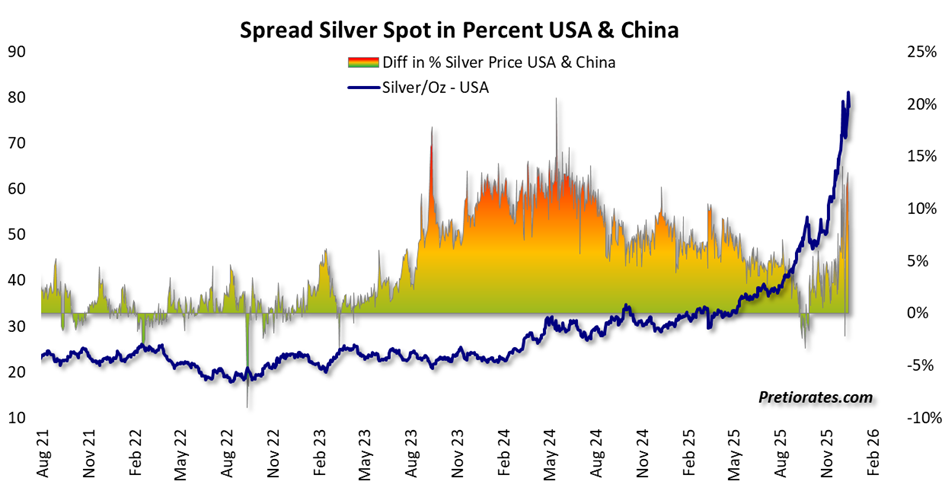

This rebalancing could create short-term selling pressure on precious metals worldwide. However, we do not believe this will be a simple trade – after all, this effect has long been known to all professional market participants. In addition, silver continues to fetch around 10% more in Shanghai.

(Click on image to enlarge)

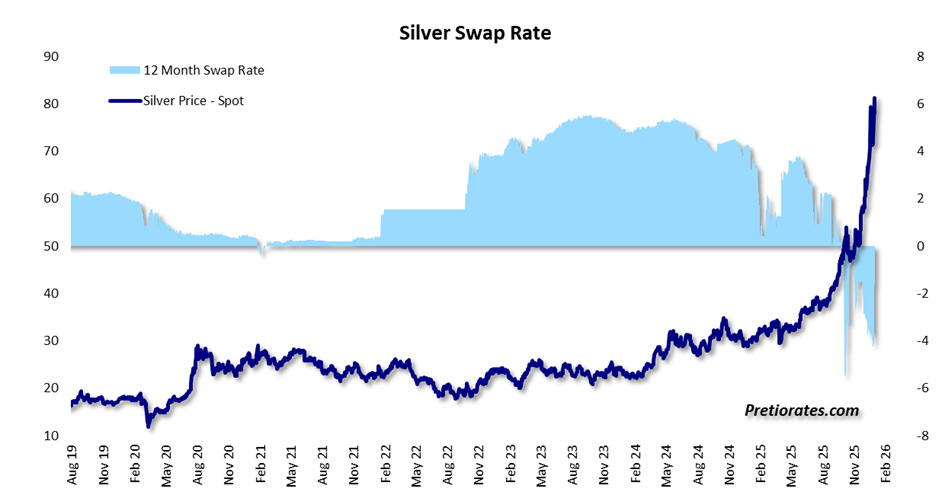

A well-deserved consolidation in precious metals would nevertheless be conceivable – many investors have been waiting for this for some time. However, the physical shortage of silver is unlikely to change much. As long as lease rates in London remain high and swap rates remain negative, the medium to long-term outlook for silver in particular remains clearly positive. This is because they indicate that there is hardly any physical silver available on the market.

(Click on image to enlarge)

More By This Author:

Silver Delta Hedge

Noise, Myths And Mechanics In The Silver Market

When Silver Runs Hot And Platinum Smells Opportunity

Comments

Log in or sign up to join the conversation.