Treading Water

“Sex is like a fish out of water, there is a lot of flopping around and gasping for air.” – Gary Shandling

The markets were much like Gary Shandling’s view of sex during this holiday-shortened week. There was a lot of flopping around to eventually wind up back where we started. We starting out trading this week with a break of the 100-dma on concerns of Italy and an Italian bank debt crisis. On Wednesday, such was no longer a concern as Fed rate hike odds for June plunged keeping rates “lower for longer.” But Thursday saw another plunge as the current Administration revived concerns over international “trade wars.” Then Friday came with a stronger than expected employment report which was reason enough to rally traders once again.

I’m worn out just writing about it.

The good news is that we did gain a VERY small bit of ground over Friday’s close, but not much.

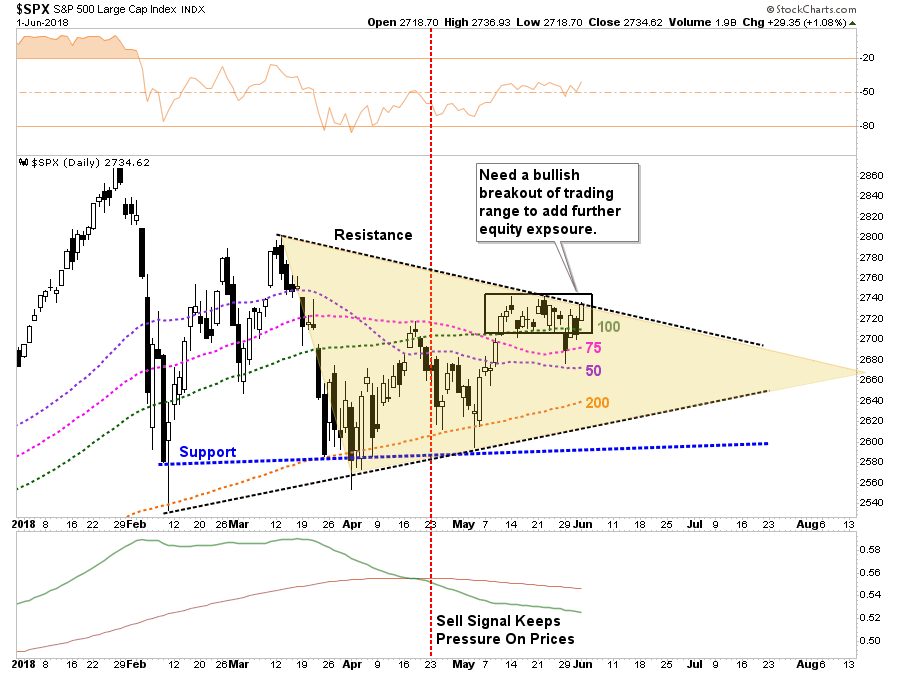

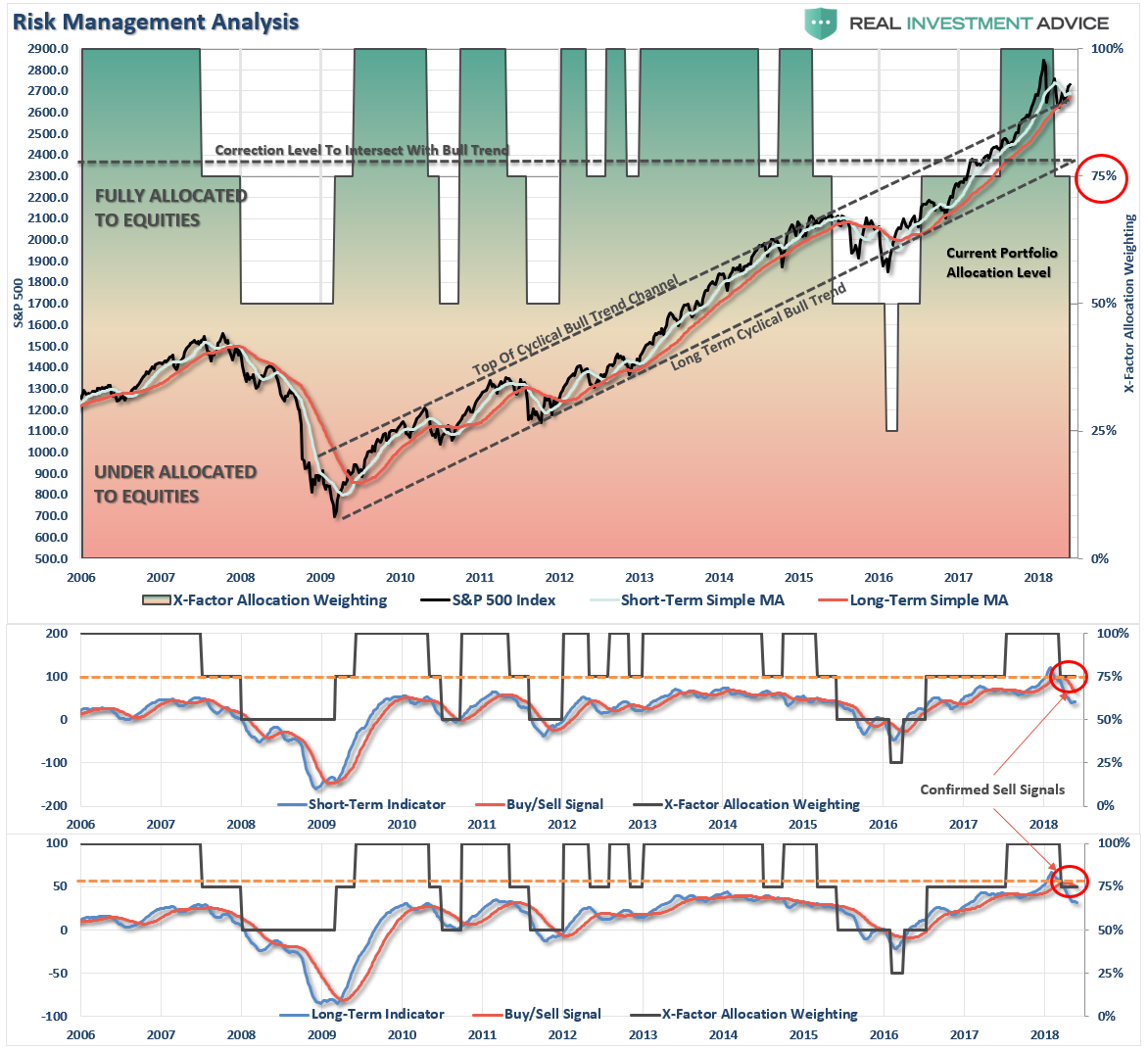

There wasn’t any “bad news", so to speak, so the “mediocre” news is that despite the solid rise in the markets from Tuesday’s low, we remain very range bound between the 100-dma and the closing highs over the last couple of weeks as shown below. The tan shaded area is the current consolidation process from the March highs.

The daily “sell signal” continues to keep us more cautious on the market currently. More importantly, we are watching the erosion of the gap between the 50-dma and the 200-dma very closely. A negative cross of those two averages has historically been indicative of more extended difficulties for the market.

Importantly, our current equity exposure remains under strict guidelines:

- Overweight cash in portfolios as the “risk” of a failure has not been absolved as of yet,

- Positions are carrying a “tighter than normal” stop-loss level, and;

- We will quickly add negative hedges as necessary on any failure of support.

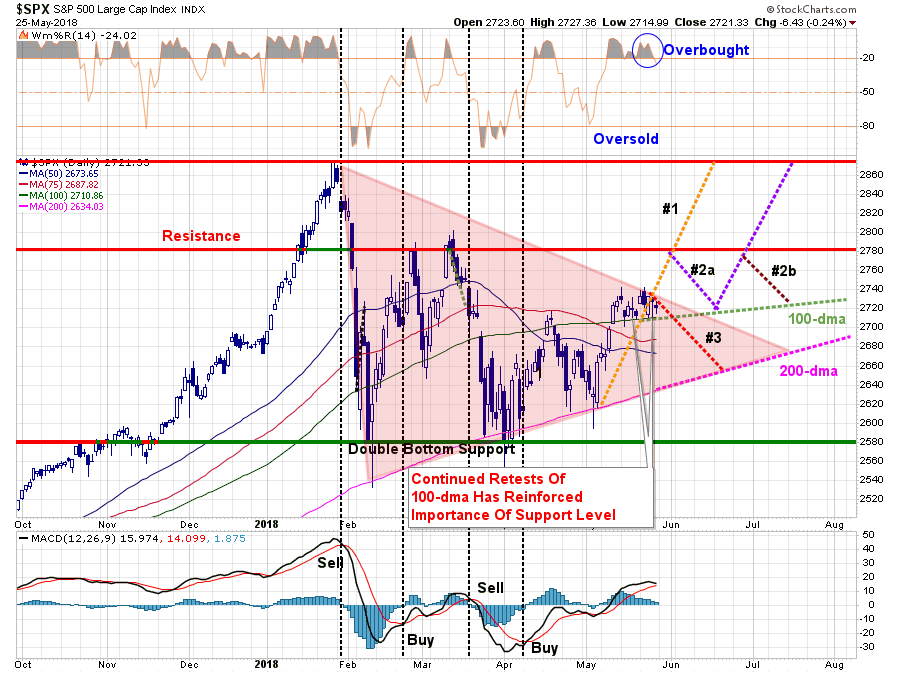

In last week’s missive I updated our “pathway analysis” for the current changes to date.

“As shown by the reddish triangle, the ongoing consolidation process continues. Eventually, this will end with either a bullish or bearish conclusion. There is no “middle ground” to be had here.

- Pathway #1 – a breakout to the upside on heavy volume that pushes the market through resistance at 2780 and back to old highs. (Probability 20%)

- Pathway #2a and #2b – a breakout to the upside which fails resistance at 2780. The market then either a) retests the 100-dma and then is able to push to old highs, or, b) fails at 2780 a second time and continues the consolidation process through the summer. (Probability 50%)

- Pathway #3 – the market breaks down next week on continued geopolitical worries, economic data or some unexpected catalyst and retests the 200-dma. (Probability 30%)

I have increased the more “bearish” probability from 20% last week to 30% this week given the potential triggering of a short-term “sell-signal.” (Lower panel) If the market struggles next week, a triggering of that signal will increase the downward pressure on equity prices.

We will continue to hold our cash position until the market makes some determination as to its direction.”

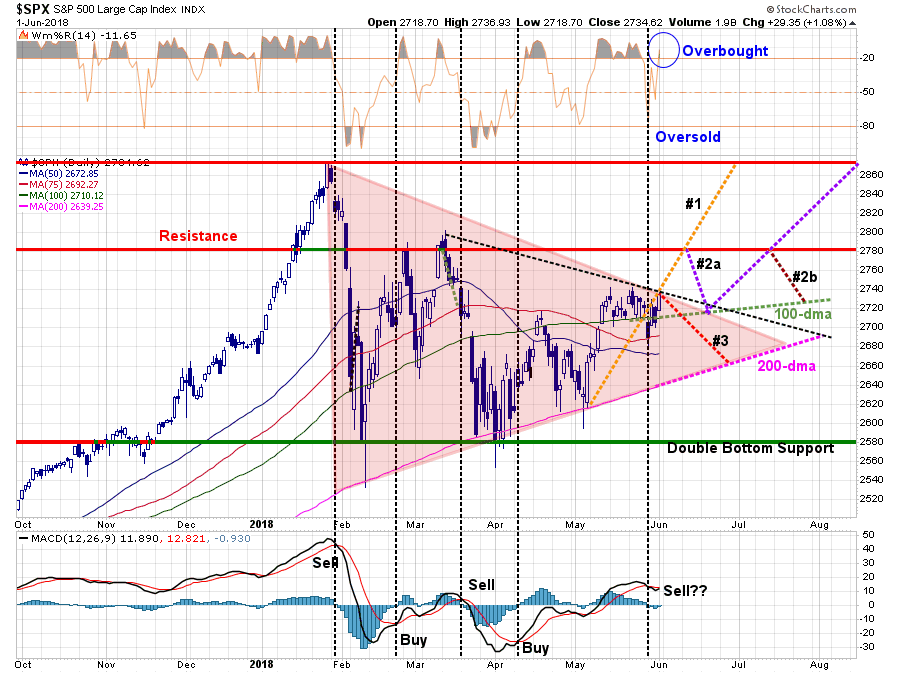

While nothing has changed from last week in terms of “risk versus reward", the sideways action last week continues to elongate our pathways within the current consolidation process. As shown below the pathways are being pushed further out which coincides with a late summer conclusion and the end of the “seasonally weak” period.

The analysis of the pathways remains the same this week, in terms of the probabilities for the next potential move, I have added the blacked dashed line from the March highs which provided resistance to the market’s advance on Friday.

Despite the improvement of the markets on Friday, there has been little done to solve the issues that plagued the market this week.

- Italy is still a problem

- The elected officials in both Spain and Italy are not particularly “EU” friendly with both recent appointments primarily anti-establishment officials.

- The “Trade War” is just starting to heat up with tariffs begin levied on multiple countries and products.

- China is still a “wild card” in the current negotiations.

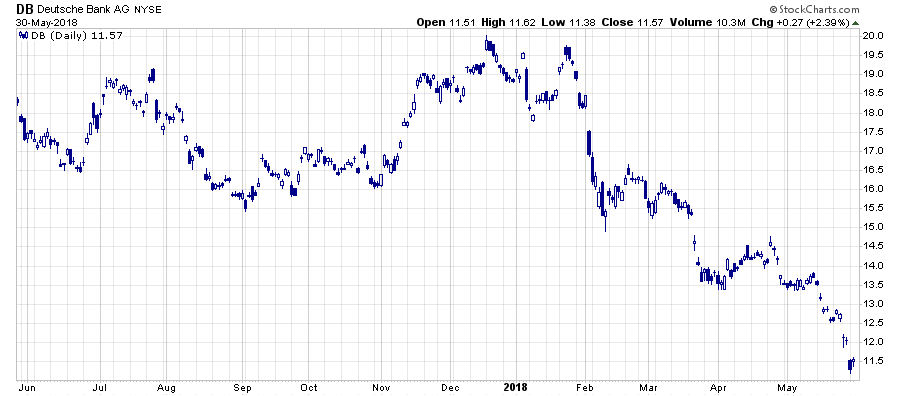

- Deutsche Bank, as discussed below, is a major issue of concern.

- Fed continues to tighten monetary policy despite signs rates are already becoming problematic.

I suspect these issues will likely bubble to the surface again over the next several weeks.

With the daily short-term “sell signal” registered on Thursday, and remaining so on Friday, it keeps our allocations on hold until next week. While we have removed a bulk of our hedges, for now, we will be quick to add them back should the market begin to show signs of further deterioration.

As noted above, we are still giving a 70% weighting to a more bullish outcome for our holdings. While there are those who wish to focus on the other 30% and proclaim we are bearish, I assure you we are not.

However, when it comes to investing, and the financial markets, nothing is a certainty. Disregarding the potential for a negative outcome layers excessive risk into portfolios which can damage long-term returns. As I penned previously:

“It should be obvious that an honest assessment of uncertainty leads to better decisions, but the benefits of Rubin’s approach, and mine, goes beyond that. For starters, although it may seem contradictory, embracing uncertainty reduces risk while denial increases it. Another benefit of acknowledged uncertainty is it keeps you honest.

‘A healthy respect for uncertainty and focus on probability drives you never to be satisfied with your conclusions.It keeps you moving forward to seek out more information, to question conventional thinking and to continually refine your judgments and understanding that difference between certainty and likelihood can make all the difference.’

We must be able to recognize, and be responsive to, changes in underlying market dynamics if they change for the worse and be aware of the risks that are inherent in portfolio allocation models. The reality is that we can’t control outcomes. The most we can do is influence the probability of certain outcomes which is why the day to day management of risks and investing based on probabilities, rather than possibilities, is important not only to capital preservation but to investment success over time.

As I have stated before, as a portfolio manager, I am neither bullish or bearish. I simply view the world through the lens of statistics and probabilities. My job is to manage the inherent risk to investment capital. If I protect the investment capital in the short term – the long-term capital appreciation will take of itself.

For those that wish to remain ‘reading impaired,’ there is always “hope” as an investment strategy.”

The market continues to tread water currently. The current question is whether it can keep its head above water until it is rescued, or will fatigue finally drag it under.

Why Deutsche Bank Is Important…

I penned this on Friday, but it is important to understand.

On Tuesday, the market tumbled on concerns over Italian debt. (A problem, by the way, I discussed a couple of years ago.) However, on Wednesday, the market reversed course and apparently the crisis was over. Make no mistake, nothing was fixed or resolved, investors just chose to ignore the problem under the belief that Central Bankers will unite in some form of bailout.

It isn’t just Italian debt, which is magnitudes larger than Greece’s debt crisis, but it is also Spain, and a host of other smaller European countries that continue to ramp up debt in hopes that economic growth will someday bail them out. However, sustained economic growth has failed to appear.

As long as interest rates remain low, and negative in some cases, debt can continue to be accumulated even with weaker rates of economic growth. More importantly, as long as rates remain low, the banking system can continue to play the “hide-the-debt game” through derivatives, swaps and a variety of other means.

But rates are rising, and sharply, on the shorter-end of the curve.

Historically, sharply rising rates have been a catalyst for a debt-related crisis. As long as everything remains within the expected ranges, the complicated “math” behind trillions of dollars worth of financial instruments function properly. It is when those boundaries are broken that things “go wrong” and quickly so.

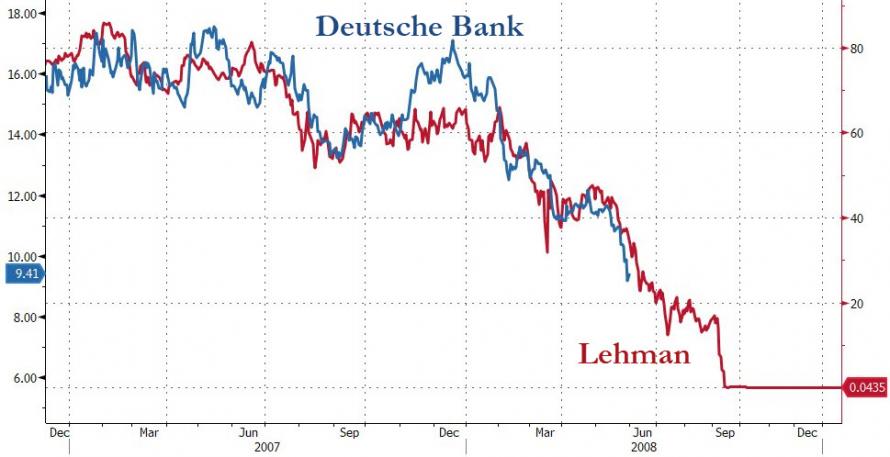

People have forgotten that in 2008 a major U.S. financial firm crashed as its derivative based exposure “blew up". No, I am not talking about Lehman Brothers, the poster-child of the financial crisis, I am talking about Bear Stearns.

In just 365-days, Bear Stearns stock went from $159 to $2, with about half of the loss occurring within a few weeks.

Bear Stearns was the warning shot for the financial markets in early 2008 that no one heeded. Within a couple of months, the markets dismissed Bear Stearns as a “non-event” and rallied to a higher level than prior to the event, and almost back to highs for the year.

Remember, there was “nothing to worry about” at the time, even though the Fed was increasing interest rates, as the “Goldilocks economy” could handle tighter monetary policy. Sure, housing had been slowing down, mortgage delinquencies were rising, along with credit card defaults, but there wasn’t much concern.

Today, we are seeing similar signs.

Interest rates are rising, along with delinquencies, defaults, and a slowing housing market. But no one is concerned as the “Goldilocks economy” can clearly offset these mild risks. And no one is paying attention to, what I believe to be, one of the biggest risks to the global financial markets – Deutsche Bank.

Deutsche Bank is clearly showing signs of financial trouble. More importantly, it is magnitudes larger, in terms of derivative-based exposure, than Bear Stearns and Lehman Brothers combined. Bear Stearns and Lehman Brothers were not banks and did not hold deposits. As such, they posed significantly less risk to the financial system.

As Doug Kass recently noted:

“The collateral risks to Europe are large – most notably to ECB and to Germany. In it’s extreme it could mean Italy separates from the rest of the EU. To me, as I have written in the past, Deutsche Bank is particularly exposed.

But, to this observer, who has consistently warned about Deutsche Bank being the next Black Swan and the imbalances in the European banking system (particularly in Italy), the risks of a possible negative multiplier effect on other European financial intermediaries and on the region’s economic prospects is profoundly real.”

Oh, and just one last chart. During 2007, and into 2008, the S&P 500 traded sideways in a 150-point range. That range was extended to 300-points before the crash actually occurred.

It was believed to be just a “pause that refreshes.”

Since January of this year, the S&P 500 has been trading in a 300-point range (similar in percentage terms to the period preceding Bear Stearns).

It is also believed to just be a “pause that refreshes.”

Here is a chart from Zerohedge showing the overlay.

“And finally, there’s this – probably nothing though…”

15-Risk Management Rules

This is probably a good time to review the 15-risk management rules we employ in our process. These rules are not new, or different, but they have been learned, and relearned, over my 30-year career.

Why? Because I am human and every so often I let my emotions get the better of me. I hold a position too long, don’t honor a stop as I should, or try to second guess my own analysis. Inevitably, more often than not, I am retaught one of the following lessons and reminded why they are important.

While our fundamental, economic and price analysis forms the backdrop of overall risk exposure and asset allocation, the following rules are the “control boundaries” for all specific actions.

- Cut losers short and let winner’s run. (Be a scale-up buyer into strength.)

- Set goals and be actionable. (Without specific goals, trades become arbitrary and increase overall portfolio risk.)

- Emotionally driven decisions void the investment process. (Buy high/sell low)

- Follow the trend. (80% of portfolio performance is determined by the long-term, monthly, trend. While a “rising tide lifts all boats,” the opposite is also true.)

- Never let a “trading opportunity” turn into a long-term investment. (Refer to rule #1. All initial purchases are “trades,” until your investment thesis is proved correct.)

- An investment discipline does not work if it is not followed.

- “Losing money” is part of the investment process. (If you are not prepared to take losses when they occur, you should not be investing.)

- The odds of success improve greatly when the fundamental analysis is confirmed by the technical price action. (This applies to both bull and bear markets)

- Never, under any circumstances, add to a losing position. (As Paul Tudor Jones once quipped: “Only losers add to losers.”)

- Market are either “bullish” or “bearish.” During a “bull market” be only long or neutral. During a “bear market” be only neutral or short. (Bull and Bear markets are determined by their long-term trend as shown in the chart below.)

- When markets are trading at, or near, extremes do the opposite of the “herd.”

- Do more of what works and less of what doesn’t. (Traditional rebalancing takes money from winners and adds it to losers. Rebalance by reducing losers and adding to winners.)

- “Buy” and “Sell” signals are only useful if they are implemented. (Managing a portfolio without a “buy/sell” discipline is designed to fail.)

- Strive to be a .700 “at bat” player. (No strategy works 100% of the time. However, being consistent, controlling errors, and capitalizing on opportunity is what wins games.)

- Manage risk and volatility. (Controlling the variables that lead to investment mistakes is what generates returns as a byproduct.)

Everyone approaches money management differently. This is just how we do it.

Market & Sector Analysis

Data Analysis Of The Market & Sectors For Traders

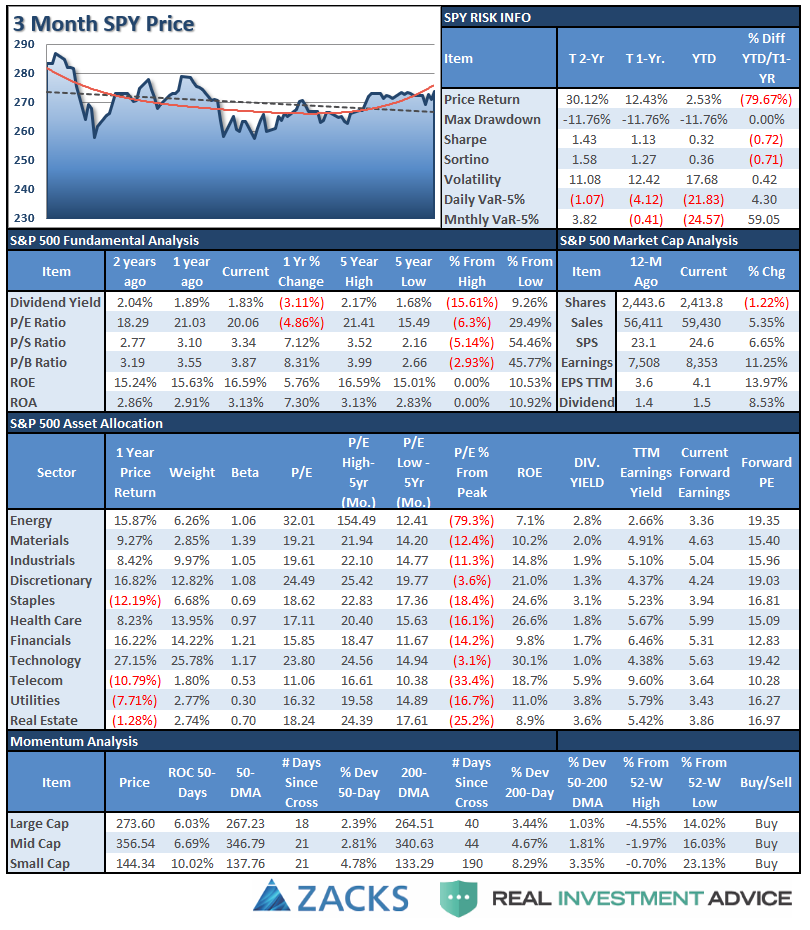

S&P 500 Tear Sheet

Performance Analysis

ETF Model Relative Performance Analysis

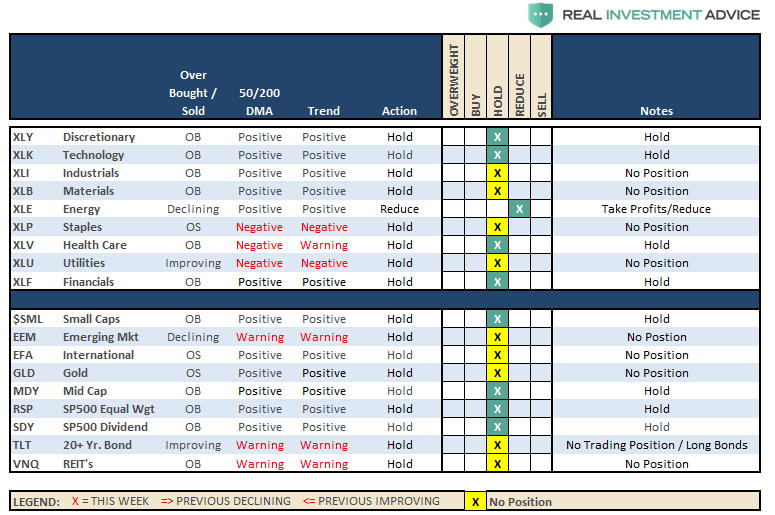

Sector & Market Analysis:

As noted above, the consolidation continues. As earnings season comes to its conclusion, the market will turn its focus to the economic and geopolitical backdrop which has been less optimistic as of late. We remain invested but our caution levels remain elevated.

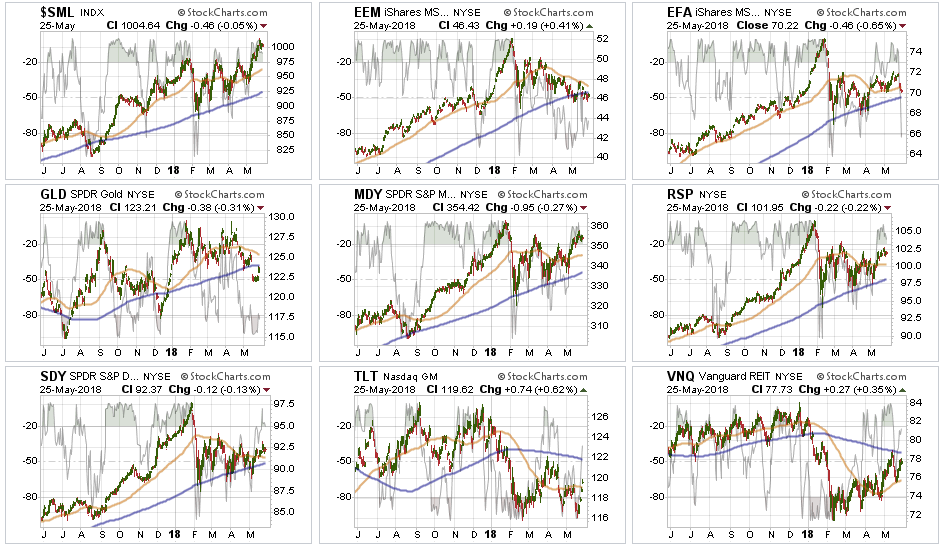

Discretionary stocks have been leading the market as of late. However, as we noted last week, pay close attention to the price compression currently forming. A downside break could lead to a rather sharp decline, so taking some profits from the sector remains advisable.

Energy led the decline last week as oil prices pushed fell back below $70/bbl. We got a bit of a bounce in the sector last week which is likely a good opportunity to harvest profits currently. As stated last week, we are likely not done with the correction yet particularly if the dollar continues to strengthen.

Technology is currently testing a double top from March of this year. A breakout here could be bullish for the sector, a failure will potentially be more problematic. We continue to carry an overweight position to the sector and will look to broaden exposure if a breakout does occur.

Financials, Industrials, Materials, and Health Care held above their respective 50-dma’s again last week and continue to consolidate. Materials and Health Care are currently the least attractive of the group with their respective 50-dma’s below their 200-dma’s. Remain underweight these two sectors for now.

Staples continue to languish and under-perform. We are still watching the sector for a sector rotation play, but it still remains too soon to add staples just yet. We are watching closely particularly as we move further into the summer months.

Utilities had a nice rally last week back above its 50-dma as money rotated into the Utilities (and Bonds) on a “risk off” trade. We remain out of the sector for now, but the rally last week has caught our attention. We need some confirmation of sustainability and we will continue to watch for an opportunity.

Small-Cap and Mid Cap continue to lead performance overall. After small caps broke out of a multi-top trading range, we now need a pull-back to add further exposure. While Mid-cap stocks have not broken out to all-time highs, a pullback that doesn’t violate support will also provide a better opportunity to increase exposure. After a strong push over the last few weeks, rebalance back to core weightings and look for a more opportunistic entry point in the future.

Emerging and International Markets remain lackluster in terms of performance currently. We previously removed our holdings in these markets and remain domestically focused at the moment. We will continue to monitor performance for an opportunity if it presents itself. Emerging markets, in particular, continue to lag due to a rising dollar and weak economic growth globally. Industrialized International is performing better but not by much. Remain domestically focused to reduce the drag on overall portfolio performance.

Dividends and Equal weight continue to hold their own and we continue to hold our allocations to these “core holdings.”

Gold as noted last week, gold failed to hold important support at the 200-dma. We currently do not have exposure to gold and have been out for a long time. We previously suggested that “if you are already long the metal hold for now. $123 on GLD is a hard stop and profits should be harvested on any failed rally back to the 200-dma.” Gold rallied and failed at the 200-dma. Take profits on positions, and lower your stop to last week’s bottom at $122.

Bonds and REITs – were the big winners last week. Just about the time you see articles declaring the “bond bull” dead, it is usually time to start buying interest rate sensitive sectors. We remain out of trading positions currently, but remain long “core” bond holdings mostly in floating rate and shorter duration exposure. REIT’s are much more interesting now with a break back above their 200-dma. With the sector back on a “buy signal” short-term we will look for an opportunity to add REIT’s back into our portfolios.

The table below shows thoughts on specific actions related to the current market environment.

(These are not recommendations or solicitations to take any action. This is for informational purposes only related to market extremes and contrarian positioning within portfolios. Use at your own risk and peril.)

Portfolio/Client Update:

Nothing much changed as of last week, as markets still remain tightly range bound. The weakness in the market hasn’t violated any support, and we are still looking for an opportunity to average into our positions.

However, as stated in the main missive above, we are acutely aware of the rising geopolitical, economic and rate risks that are currently prevalent in the market. The recent pickup in price volatility has historically not been a good intermediate-term indicator of more bullish future price action.

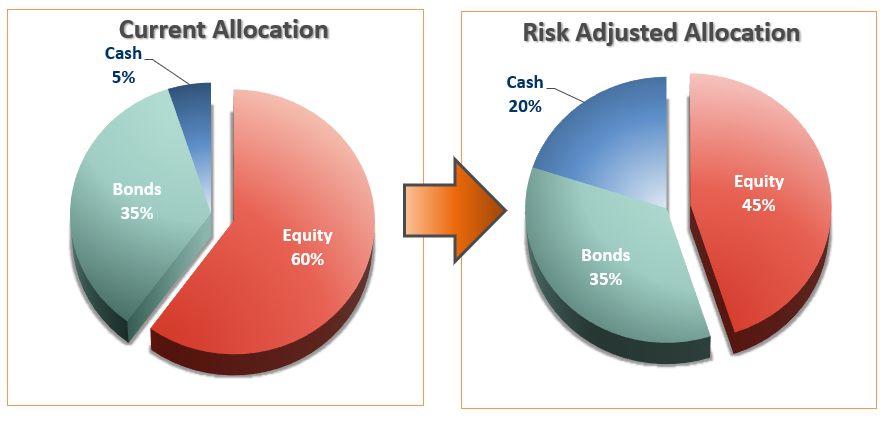

As such we continue to carry an overweight position in cash, we remain underweight in equities and market weight in fixed income.

We have also taken action to shorten our bond-duration, add floating-rate holdings and minimize rate-related risk as much as possible.

We remain keenly aware of the intermediate-term “sell signal“ and we will continue to take actions to hedge risks and protect capital until those signals are reversed.

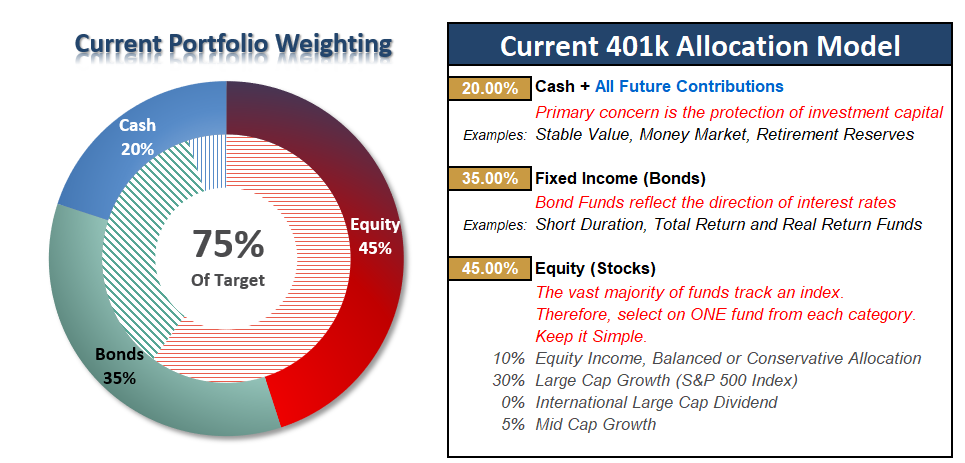

THE REAL 401k PLAN MANAGER

The Real 401k Plan Manager – A Conservative Strategy For Long-Term Investors

There are 4-steps to allocation changes based on 25% reduction increments. As noted in the chart above a 100% allocation level is equal to 60% stocks. I never advocate being 100% out of the market as it is far too difficult to reverse course when the market changes from a negative to a positive trend. Emotions keep us from taking the correct action.

Back Where We Started

Another week where nothing changed much in the market. This has been a similar refrain over the last few weeks as the market continues to consolidate within a very defined range.

I wish I had more to say, but the reality is that “sell signals” on a longer-term basis remain intact currently which keeps cash levels elevated. Until the market breaks out of the current consolidation process, and gives some evidence of the ability to push higher, we suggest continuing to remain more cautiously allocated in the near term.

Since 401k plans have limited options, and restricted trading, we work from a more macro, risk-adjusted, allocation structure. For new readers, our current advice remains the same as we have posted over the last several weeks:

“Currently, our model remains underweight equities at the moment as we have to respect both of the ‘sell signals’ that currently remain intact as shown above. We also try to remain cognizant of the ‘trading restrictions’ that exist in most 401k-plans. Over the last couple of months, we have been recommending to reduce equity allocations as follows.”

“If you have already reduced equity exposure, just sit tight this week and let’s see what happens.”

This week, the instructions continue to remain the same.

- If you are new to reading the newsletter or have NOT taken any previous actions or are overweight equities in your plan – Do nothing.

- If you are slightly underweight equities in your plan – move to the RISK ADJUSTED allocation model.

- If you are very underweight equities in your plan – move 50% of the way toward the RISK ADJUSTED model.

I know, it’s boring.

But sometimes, “doing nothing” is the better course of action than “doing something” that turns out to be wrong.

Current 401-k Allocation Model

The 401k plan allocation plan below follows the K.I.S.S. principle. By keeping the allocation extremely simplified it allows for better control of the allocation and a closer tracking to the benchmark objective over time. (If you want to make it more complicated you can, however, statistics show that simply adding more funds does not increase performance to any great degree.)

401k Choice Matching List

The list below shows sample 401k plan funds for each major category. In reality, the majority of funds all track their indices fairly closely. Therefore, if you don’t see your exact fund listed, look for a fund that is similar in nature.

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Real Investment Advice is expressly disclaims all liability in ...

more

Thanks for the article, so watch out for a break out around $274? if it doesn't break we should revisit 200mda?

Yep.