Stocks eked out paltry gains and consolidated within a technically overbought market condition.

Quote of the day: “When things fall apart, things fall together. Keep the faith.”

— Clintonian Maximus

Commentary

Stocks eked out paltry gains and consolidated within a technically overbought market condition. Hyperbolic trends can make markets vulnerable to near-term corrections. The macro-narrative has not changed in that inflation is still a concern and evidence of contracting global growth such as witnessed in China, the world’s second-largest economy, could hinder any efforts to stabilize and stimulate domestic growth in the U.S. Tomorrow’s economic and earnings calendars will be light and allow traders a pause to synthesize the current week’s data before the weekend.

With respect to energy commodities, Oil and Gasoline prices have been extremely volatile but are trending downward against a resilient and rising dollar. Fundamentally, there is still the chance of Iran consenting to a nuclear deal with the U.S. and E.U. If successful, it would remove sanctions and allow Iran to resume oil exports (and help Europe mitigate economic and geopolitical risks of supply shortages posed by Russia’s potential response to sanctions against its “special military operation” in Ukraine). Closing such a deal could lead WTI Crude Oil prices to retrace towards $70 or $65 per bbl over the next 6-9 months. Imagine that!!!

Until tomorrow with more insights, I shall sign off...

Bullish Events

Economy / Business Conditions:

Philly Fed Mfg Index for Aug-2022 @ 6.2 vs estimates @ -5.0 and prior @ -12.3.

Philly Fed Employment @ 24.1 vs prior @ 19.4.

Economy / Weekly Unemployment:

Initial Jobless Claims @ 250k vs estimates @ 265k and prior @ 252k.

4-week moving average @ 246.75k vs 249.5k.

Earnings / Technology:

CSCO reported better than expected results after yesterday’s close. Q4 revenue was @ $13.1b vs estimates @ $12.73b. while forecasting 2023 revenue growth @ +4% to +6% vs expectations @ +3.3%.

KEYS reported Q3 revenues @ $1.41b vs estimates @ $1.35b with forecast for Q4 revenue @ $1.38b to $1.4b vs estimates @ $1.38bn.

Neutral Events

n/a

Bearish Events

Economy / Growth: Leading Economic Indicators (LEI) for July-2022 @ -0.4% vs estimates @ -0.05% and prior @ -0.8%.

Real Estate / Residential for Jul-2022:

Existing Home Sales @ 4.81m vs estimates @ 4.89m and prior @ 5.11m.

Existing Home Sales (m/m) @ -5.9% vs prior @ -5.5%.

Commodities / Energy: Weekly inventories for Natural Gas @ 18 bcf vs prior @ 44 bcf.

Central Banks / U.S. Monetary Policy: San Francisco Fed President Daly issued hawkish comments that its central bank could “go above” a neutral rate of 3% in order to reverse inflation, thus confirming 50 bps to 75 bps remains under consideration.

Analyst Downgrades / Industrials: Bernstein downgraded URI to underperform from market performance.

Asia / Economic Outlook: Goldman Sachs and Nomura Securities respectively reduced the 2022 GDP outlook for China (the world’s 2nd largest economy) to 3.0% from 3.3% and to 2.8% from 3.3%. Bellwether Chinese stocks declined in sympathy: NTES; BIDU; JD; and PDD.it

Technically Speaking

Here’s a 30-year snapshot of the US Dollar Index. Why look at the dollar when this report primarily focuses on equities? For starters, strength or weakness is an important variable when it comes to trade balances and economic growth. In addition to this, commodities are priced in U.S. dollars, and as the dollar rises commodity prices fall lower. They are inversely correlated.

Given the above, along with the fact that inflation is the biggest headwind on the path toward resumption of economic growth and that energy and food prices are the main contributors to consumer inflation, it behooves one to monitor the market direction for the dollar. Below is a monthly chart that shows a bullish primary (long-term cyclical) trend for the dollar. Support for the dollar is @ $101 to $103 levels, but it is converging towards resistance @ $110. Currently, stochastics (see the lower pane of the chart below) indicate a technically overbought dollar.

Assuming this uptrend continues amongst currencies as supply chain bottlenecks due to Covid are alleviated and the fiscally unsustainable war between Russia and Ukraine inevitably concludes, then energy and food commodity prices should decline. Bear in mind (no pun intended), that I am not forecasting that “we shall live happily ever after”. However, the global and domestic economic situation should improve. Besides one would be well advised to remember: "Don’t fight the trend because it is your friend."

Performance: DJ Real Estate Index @ 393.70 (-0.74%); DJ Home Construction @ 1259.91 (+0.06%)

Comments: Existing U.S. home sales have declined 6 consecutive months. Mortgage rates peaked in June-2022 @ 6% but have since stabilized to @ 5% and could ignite more buying as inventory has risen @ 4.8% to 1.31m units.

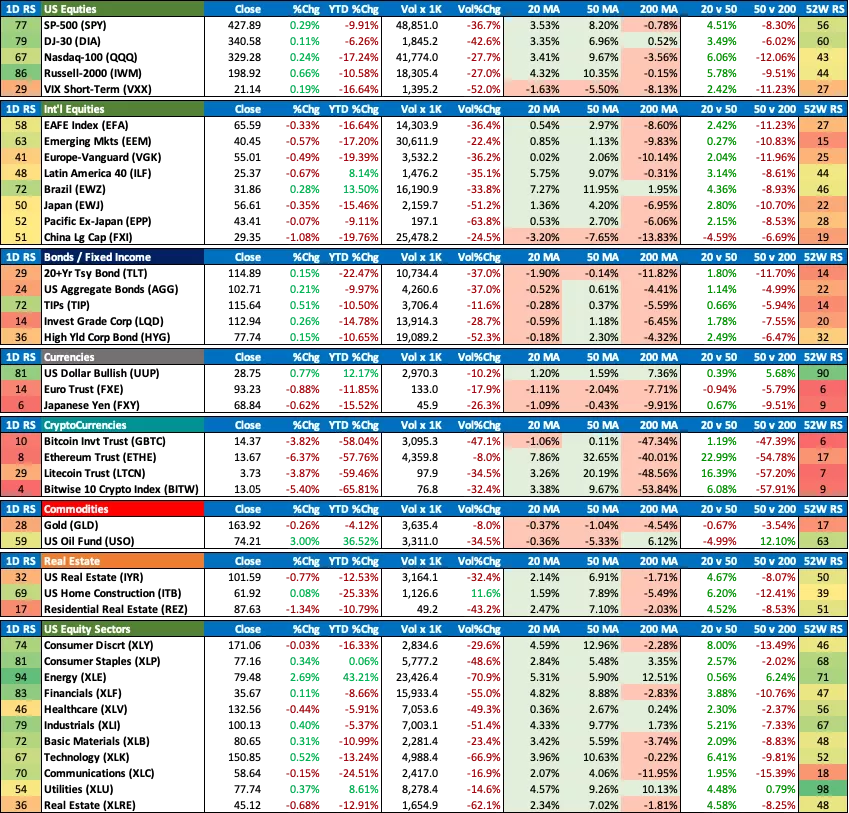

Daily ETF Performance Monitor

(Click on image to enlarge)

Market Diary

(Click on image to enlarge)

Earnings

Sector

Positive Surprise

Meeting Expectations

Negative Surprise

Consumer Staples

TPR

Consumer Staples

EL

Technology

NTES

*Earnings reported After-market hours

Market SWOT Analysis

Strengths (happening now)

Weaknesses (happening now)

Energy Production Capacity Growing: Decline in WTI Crude Oil rapidly accelerating and the mantra that higher prices correct higher prices is being realized. Even more significant is the contraction in RBOB Gasoline futures, which ultimately translates into relief at the gas pumps for American consumers.

Strong Employment Situation: The July-2022 employment report indicated a 528k increase of new jobs vs June-2022’s already robust gain of 398k. The unemployment rate is ticked lower to 3.5% vs prior @ 3.6%. It’s a tight labor market and therefore wage inflation should be expected. However, if the Fed is able to reign in high fuel and food prices by raising rates, then this creates a situation for a strong recovery in consumer activity.

Cryptocurrencies: Bitcoin and Ethereum are proxies of investor sentiment toward risk and appear to have found support and are initiating new uptrends. If so, this could have bullish implications for equity markets.

Untamed Inflation: Consumer prices (CPI data), which are closely monitored by the Fed, have been trending above 8%+ with the potential for double-digit inflation. The June 2022 report to be released in July 2022 could trigger more aggressive rate hikes.

Geopolitical Risk in Greater China: House Speaker Nancy Pelosi’s visit to Taiwan has clearly upset China and emboldened it to step up its military exercises and threaten invasion of the island. The risk of confrontation with the U.S. must be balanced and taken into consideration.

Continued Disruptions in China Supply Chain: Covid infection rates are increasing and prompting Chinese officials to once again shut down its economy, thus exacerbating supply chain bottlenecks.

Opportunities (could happen)

Threats (could happen)

Lower Energy Prices: The Federal Reserve’s resolve to combat inflation with aggressive rate hikes will have the collateral effect of creating a stronger dollar and, if a soft landing is achieved, a mild recession will contribute to demand destruction for energy and lower prices for consumers. A decline in energy prices could reignite consumer demand and confidence, especially if the labor market remains stable.

Cutting a deal with Iran: The U.S. and Iran are currently negotiating to end sanctions and bring Iranian oil back online if certain parameters for nuclear testing and development can be accomplished. If so, this would immediately alleviate any supply imbalance in the energy markets as Iran has the capability to restart production almost immediately. A successful outcome for these negotiations could happen instantaneously and presents a legitimate risk for anyone committed to long exposure to crude oil futures or the actual product itself.

EU negotiations with Iran: More than 15 months have been invested between the U.S. and Iran to revive the 2015 nuclear deal. It is reported that EU officials have submitted a final text for Tehran to sign. In the event this actually happens, it would have the same aforementioned bearish implications for Oil prices.

EU Winter Energy Supply: Russia could weaponize its energy supplies to EU countries for the upcoming winter in response to sanctions imposed against it as well as the military and financial aid it is providing Ukraine to thwart its invasion. If so, energy prices could explode higher.

Analysts Downgrades and Revisions: As the Fed continues to tighten, another wave of negative earnings revisions would require recalibration of equity market valuations.

Global Food Inflation and Famine: Russia vs Ukraine conflict has the potential to destabilize food supplies and create a domino effect of food inflation and famine in LDCs as well as more developed countries.

Mid-term elections: The outcome of the upcoming election in November is uncertain and given the divided state of the US, it could bring about more uncertainty and exacerbate the gridlock for which Washington DC is notorious.

This report is not distributed for the purpose of providing individualized market advice. The information published in it regards securities in which it is believed that readers may have interest and this report only reflects sincere opinions on the investment markets and events or news impacting them. Nevertheless, this report is not intended to be personalized recommendations to buy, hold, or sell securities. Investments in the securities markets, and especially in options or futures, are speculative and involve substantial risk. Each individual investor should determine their respective appropriate level of risk. It is recommended that you seek personal advice from your professional investment advisor and conduct further independent due diligence research before acting on any information published in this report. Most of the content contained herein is derived directly from information published by the companies mentioned in this report and/or from other sources deemed to be reliable, but without independent verification of such. Therefore, no assurance of the completeness or accuracy of information contained within is guaranteed and in no manner warrants or guarantees the success of any action which you take in reliance on its statements and opinions.

Comments

Log in or sign up to join the conversation.