The Treasury yield curve demonstrates the level of interest rates on U.S. government bonds of varying maturities. Normally, the yield curve is upward sloping, meaning that longer-term bonds have higher yields than shorter-term ones. This reflects the fact that investors demand higher returns for locking up their money for longer periods of time, during which the cumulative inflation is unknown. However, the yield curve is currently inverted, which means shorter-term bonds offer higher yields than longer-term bonds. This is making some investors that have historically had strategic preferences for intermediate or long-bonds consider reallocating to shorter-term bonds.

Expectations of a falling yield curve

Many investors are predicting that the yield curve is likely to fall. Due to its current inverted shape many also expect shorter-term yields to fall by a greater amount than longer-term yields. This is leading those investors to ask – if shorter-term yields fall by a greater amount than longer-term yields, should I reallocate my portfolio to short bonds given that bonds experience positive returns when interest rates fall?

For the typical investor who is building a portfolio without leverage, it is important to remember that a bond’s term to maturity impacts not only its yield but also its sensitivity to changes in interest rates. Although an investor may expect shorter-term yields to fall a lot, the price gain on shorter-term bonds will be impacted by their lower sensitivity to changes in interest rates. The following demonstrates the extent to which interest rates on 5-, 10- and 20-year bonds would need to fall to have the same positive price gain as a two-year bond experiencing a 2% fall in interest rates.1

| 2 years x 2.0% = + 4.0% price return |

| 5 years x 0.8% = + 4.0% price return |

| 10 years x 0.4% = + 4.0% price return |

| 20 years x 0.2% = + 4.0% price return |

The above shows that for an investor who is basing their desired tactical positioning on an expectation that interest rates will fall and that the short-end of the yield curve will fall by more than the long-end, for that investor to prefer two-year bonds over five-year bonds it needs to expect the two-year yield will fall by 2.5x more than the five-year yield. Similarly, it must expect 2-year yields to fall by 5.0x more than 10-year yields or 10.0x more than 20-year yields to maintain its preference for two-year bonds based on the expectation of a downwards shock to interest rates.

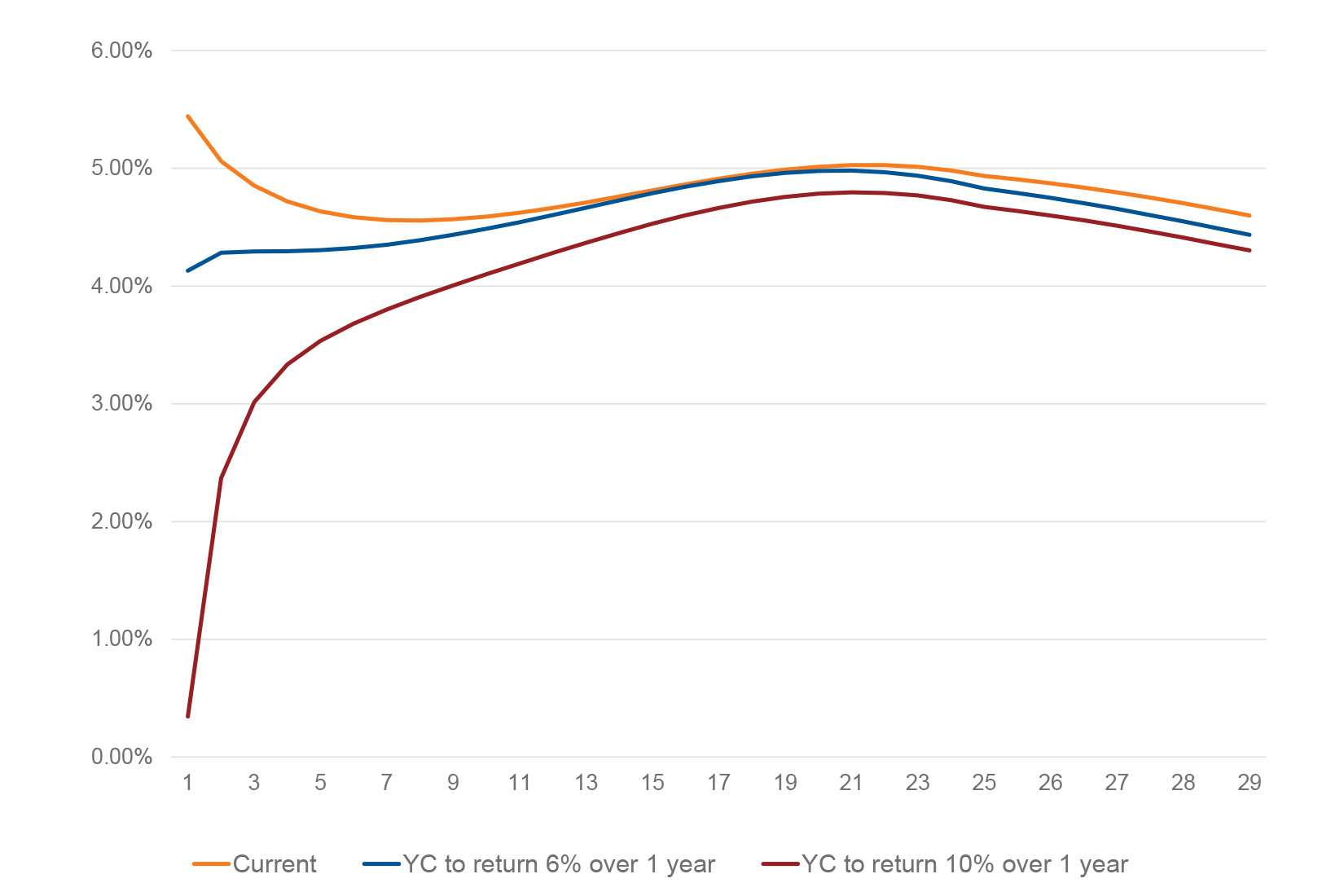

The below exhibit shows the current yield curve, and the yield curve required in one year for all Treasury bonds to achieve returns of 6.0% and 10.0%2 over the next year. The implication of this exhibit is that for an investor making tactical decisions based on the expectation that interest rates will fall, to prefer shorter-term bonds over longer-term bonds, the investor needs to expect that the differential in the extent that shorter term yields fall more than longer term yields is greater than in the exhibit.3

Yield curves required for returns of 6% or 10% over one year

(Click on image to enlarge)

Source: ICE data

Given we do not expect the differential between the fall in shorter-term and intermediate- and longer-term yields to be higher than demonstrated, we still prefer intermediate and longer-term bonds over shorter-term bonds if positioning for a fall in interest rates – even if we do expect shorter-term yields to fall more than longer-term yields.

Why might an investor still prefer short-term bonds?

An investor still might prefer shorter-term bonds. Some common reasons, both strategic and tactical, for a preference for short-term bonds are:

- Very low risk investment portfolio seeking to minimize return volatility through time

- Invested assets with the purpose of being available for potential near-term cashflow needs

- Tactical expectation that interest rates will rise

- Expectation that interest rates will remain steady in the current interest rate environment4

There are many reasons why an investor might prefer shorter-term bonds, however, we do not believe that that preference should be based off the expectation that shorter-term yields will merely fall by more than longer-term yields.

Should defined benefit pension plan sponsors be concerned?

Many defined benefit plans hedge the interest rate risk in their liabilities by investing in longer-term bonds. Plans that are implementing overlays are able to increase the hedge ratio relatively uniformly across the yield curve. This is because they are able to use leverage to increase their exposure to interest-rate sensitive investments beyond what they can accomplish with physical bond purchases. If an LDI overlay is implemented and the plan is able to construct a relatively consistent hedge ratio across the yield curve, this is not a concern.

However, many plans either choose not to or cannot access leverage, and if the plan is underfunded and/or maintains a growth portfolio, without leverage the plan will be unable to fully hedge its interest rate risk. In those cases, to increase the interest rate hedge ratio while having less money in fixed income than the value of the liabilities, we advise that they concentrate the fixed income portfolio in longer-term bonds. This allows them to hedge as much of the total interest rate risk as possible, because the longer-dated liabilities have greater interest rate sensitivity for dollar of value. It does, however, create an interest rate hedge that is uneven across the yield curve, typically with lower hedge ratios to shorter-term yields.

This is leading some to be concerned it could be problematic for the plan if short-term yields fall more than longer-term yields, given that they have higher hedge ratios on the long-term yields than the short-term yields. Due to the relationship illustrated above. focusing the hedge on the longer-term yields should still be beneficial if interest rates fall, as long as the fall in the two-year yield is less than 10.0x the fall in the 20-year yield. A significant decline in interest rates is typically a negative event for a pension plan, and maintaining the longer-term bonds to maximize the interest rate sensitivity in the fixed income portfolio would provide the greatest funded status protection in that event, even if shorter-term yields fall by double the amount as long-term yields. And if interest rates do rise, although the plan would be theoretically better off if it reduced its total hedging, its funded status would likely also rise—meaning that the pension plan should still be comfortable with its overall position.

The bottom line

Despite the shape of the yield curve, we believe that for most investors it is appropriate to maintain fixed income exposure in line with their strategic preferred positioning. For investors that have strategic reasons for preferring intermediate or longer-term bonds, we do not believe there is a compelling tactical reason to deviate from that despite the current yield curve inversion.

1 This analysis looks at the impact of an immediate shock to the yield curve and therefore does not include the impact of carry and roll on bond returns.

2 Assuming all nominal treasury yields remain positive, a 10% return cannot be achieved on the 1.5-year bond over a one-year horizon. Since this analysis is over a one-year horizon it includes the impact of carry and roll on bond returns.

3 Based on ICE US zero coupon treasury yield curve data as of 9/29/2023 and Russell calculations.

4 In most market environments the expectation that interest rates will remain steady would not lead to a preference for short-term bonds, but with the current inverted yield curve it would.

More By This Author:

Making A Trade In Q4? Key Dates To Consider AvoidingUnlisted Infrastructure – Highway To Diversification

Inflation Surprises: Consumer Prices Rise In Canada, Ease In The UK

Comments

Log in or sign up to join the conversation.