Image Source: Pixabay

Roger Federer, the tennis champion, recently made a commencement speech that held a lot of wisdom in other areas of life. He noted that out of 1,526 singles matches in his professional career, he won 80% of them. However, out of all the points he played, he won only 54% of them.

In other words, even one of the greatest tennis players of all time won little over half the points he played. But that small advantage added up over the course of a match and even more so over the course of a career.

It is much the same way in investing: each individual investment may win or lose, but the benefits of a sound decision making process accumulate over time. Even the greatest investors rarely have much more than 50% of their investments outperform. But the small advantage they have accumulates over time. They tend win over time both by having slightly higher odds and by having winners that do very while limiting the losses on losers.

Contrast this to a common flaw among investors: Monday morning quarterbacking. In other words, just looking at whatever has performed well or poorly recently.

By the time you know the outcome, it is too late.

The fact is, there is a lot of uncertainty and risk in the market. Many people look for some guru with a crystal ball, but the reality is many of those “gurus” are either charlatans or have been lucky in a particular market cycle and the risks in their strategy have not been uncovered yet.

It is tempting to look at a particular stock or fund that has done very well over the past year or so, but usually, there is an enormous amount of risk as well. And this risk is not always obvious.

The quote above about pilots applies to investors as well: there are old investors and there are bold investors, but there are few old, bold investors. By taking bold risks, you might be lucky enough times in a row to become wealthy, but all it takes is one bold risk gone wrong to wipe you out.

A better way for most people is to take prudent, moderately diversified risks that balance growth potential with less exposure to catastrophe. Focusing on a sound decision making process and accumulated benefits is not sexy like looking for the big score, but most people would be better off with such an approach.

The Tax Benefits of Roth Conversions

Roth IRAs are attractive vehicles that allow for tax free growth and tax free withdrawals. One thing that can benefit many people is converting their IRAs or 401Ks into Roths after retirement. There are two primary benefits.

- Tax rate arbitrage. If you contribute to a 401k during your high earning years, you reduce your income that is taxed at a high tax bracket. After retirement, your tax bracket will likely decrease. However, after your required minimum distributions kick in at 73, your tax bracket may increase. These years between retirement and your required minimum distribution offer an attractive opportunity to convert traditional IRA and 401k money into Roth money.

- Tax free compounding. While traditional IRAs and 401Ks offer deferred tax compounding, you or your heirs must eventually pay ordinary income taxes on the growth. However, you never need to pay taxes on growth in a Roth IRA. This allows the tax savings from the difference in tax rates to grow tax free over time. Also, if you use regular assets to pay the taxes on the Roth conversion, it is equivalent to a large new contribution to your Roth, allowing growth that would have otherwise been taxed to grow tax free.

Figuring out the right path requires careful planning. We have experience with other investors and advanced modeling software that can help you figure out the pros and cons of a conversion plan.

Unless certain criteria are met, Roth IRA owners must be 59½ or older and have held the IRA for five years before tax-free withdrawals are permitted. Additionally, each converted amount may be subject to its own five-year holding period. Converting a traditional IRA into a Roth IRA has tax implications. Investors should consult a tax advisor before deciding to do a conversion.

Key Wealth Principles

- A foundation of good habits is more important than fancy techniques

- Invest in quality businesses at an attractive price

- Build a portfolio of good businesses in different industries

- Maintain appropriate reserves and income sources

- Consider your financial circumstances, liquidity and timing needs, goals, tax considerations, and risk exposure

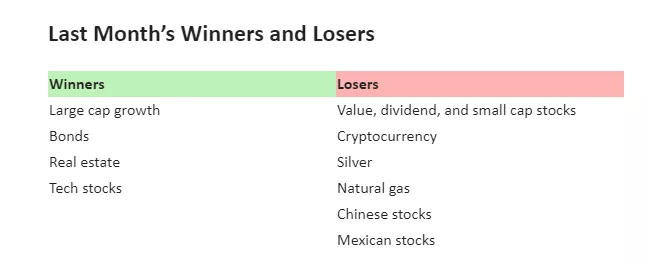

Last Month’s Winners and Losers

Large cap growth and tech stocks continued their outperformance this year vs. other stocks, which have only been up a little. Bonds and real estate also performed well on falling long term interest rates.

Losers for the month were a mixed bag of commodities (cryptocurrency, silver, natural gas), Chinese stocks, and Mexican stocks.

Stocks

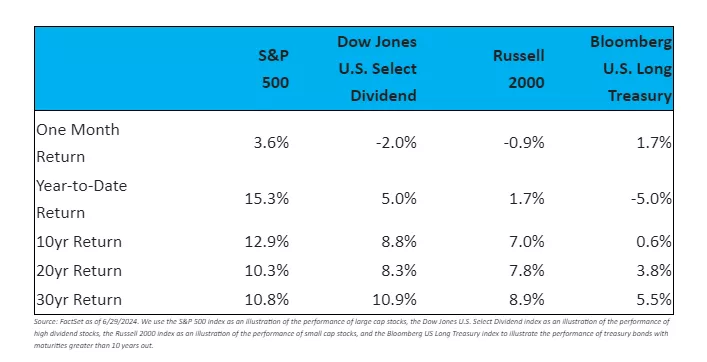

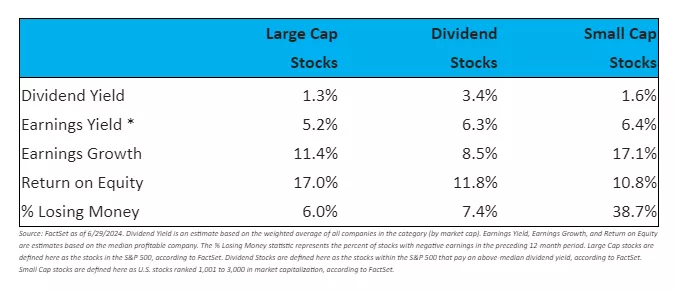

Value, dividend, and small cap stocks underperformed compared to large growth stocks, particularly artificial intelligence (AI). While it can be hard to sit out of the AI party, we all know what happens when the party’s over. So moderation is the key, even if you want some exposure.

Aside from artificial intelligence, I believe there are plenty of attractive, growing companies that trade at a reasonable valuation.

Income Investing

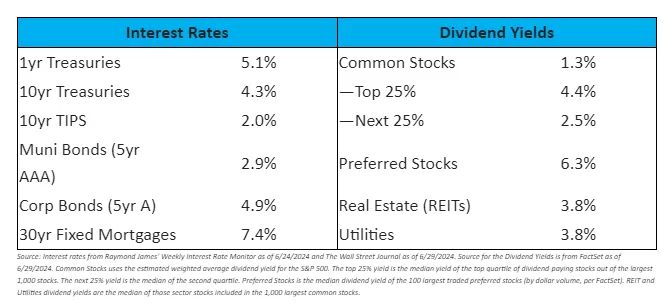

I continue to believe that short-term rates are attractive, but long-term interest rates are not particularly attractive given the risks of ongoing inflation, budget deficits, and overall debt load in the economy. I am keeping my eye on short term instruments of less than one year maturity and dividend stocks that have the potential to increase dividends faster than inflation over time.

Although commodities may offer a hedge, I prefer assets that produce independent sources of value, such as earnings, dividends, and interest, rather than betting on a particular economic outcome.

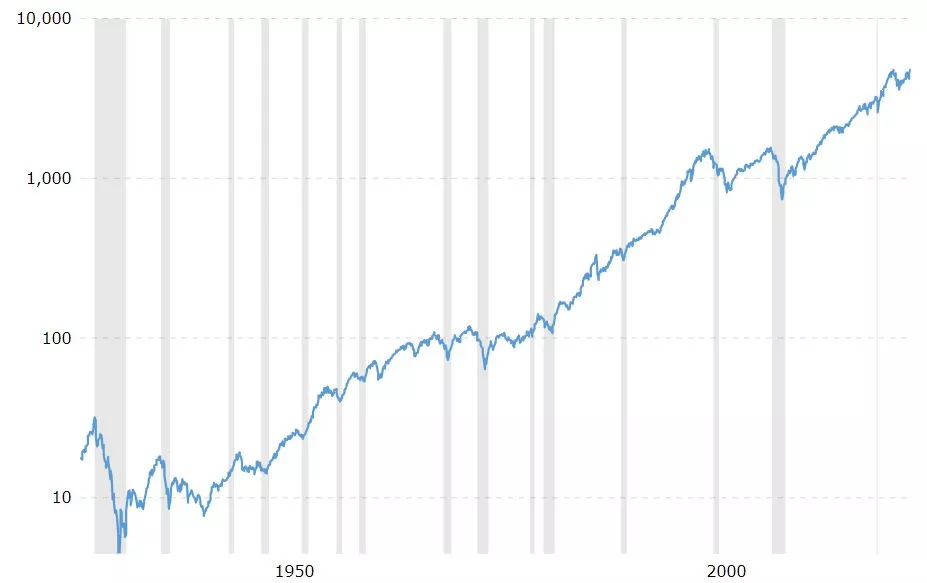

The Long View

S&P 500, Jan. 1928 to Dec. 2023

Source: MacroTrends.net

For the last 20, 30, and 100 years, stocks have averaged around an 8-10% return, driven by dividend yield, reinvestment of earnings, and earnings growth. Long-term bonds have yielded about 5% on average over the last century while inflation has been about 3%.

Throughout this period, there have been major upheavals, such as the Great Depression, World War II, The Korean War, The Vietnam War, dropping the gold standard, 1970s high inflation, 1987’s Black Monday Crash, the Dot.com bust, the 9/11 terror attacks, the Global Financial Crisis, and the Covid Crash, among others.

These events led to severe market downturns about once every decade, with a median price decline of 33% and a median time to recover back to the previous high of 3.5 years. If we were to include dividends, the recovery to previous highs is actually a little faster. *

Meanwhile, a 3% inflation rate results in a 59% decline in the value of a dollar over 30 years. Meaning that people who retire at 60 years old on a fixed income face a high risk of a lower quality of life as they get further into retirement.

The Price of Market Returns: Significant Volatility

_638556022325791810.webp)

S&P 500 Yearly Returns, 1928 to 2023. Source: MacroTrends.net

* Source: Morningstar Direct via cfainstitute.org, FactSet. Past performance is not necessarily indicative of future performance. Depreciation of the dollar: $1 / (1 + 3%)^30 = $0.41 real value 30 years later.

Market Outlook

Now I’ll put on my “Nostradamus Hat” and make some predictions, for whatever they’re worth:

- Inflation will average 2-5% over the next 10 years.

- Interest rates will fall in the 3-6% range for 10yr Treasuries over the next several years, in line with inflation and historical experience.

- The economy will grow 2-3% in real terms over the next several years.

- Stocks will average an 8-10% return over the next 10+ years. After subtracting inflation, this will translate into about a 5% real return. There is likely to be at least one big decline every decade or so.

From the standpoint of where you and your family will be in 30 years, none of this matters. What matters is finding good quality investments that are likely to grow over the decades. For this reason, I largely ignore my own general market forecast and invest whenever I find a business that I am confident in and that trades at an attractive valuation.

More By This Author:

Finding Good Quality Investments

Opportunities In Stocks And Bonds

The Perils Of A Narrow Market

Comments

Log in or sign up to join the conversation.