Image Source: Unsplash

Over the winter holiday, I read Richistan: A Journey Through the American Wealth Boom and the Lives of the New Rich, by Robert Frank, who wrote the book just before the Great Financial Crisis of 2007-09.

One person featured was a man named Pete Musser, an entrepreneur and venture capitalist who briefly became a billionaire at the height of the Dot.com boom of the late 1990s to 2000.

Pete had an ability to adapt and find winning businesses in different industries over the decades, from industrials in the 1960s to real estate in the 1970s to personal computers in the 1980s and to Internet stocks in the 1990s. Some of his early investments include QVC, Comcast, and Novell.

Despite the wide array of businesses, Pete built his wealth on, by 2000 most of his wealth was in Internet stocks. Not only did he not set aside some of his wealth in safer assets, he doubled down and margined his existing wealth to buy more Internet stocks.

When the crash came and Internet stocks fell by 90%, he lost everything and defaulted on his debt.

Decades of wealth are gone in a few years.

There are many lessons from Pete’s story about avoiding margin debt, keeping an emergency fund, diversifying among industries, and getting caught up in fads and manias. The one I want to focus on is concentration.

While he may have been invested in dozens of companies through his shares in his venture capital company, this was not true diversification since they were mainly of the same type: Internet companies. Although the trends seemed good at the time and, in fact, the Internet has revolutionized business, this does not necessarily translate into investor profits. And when the market fell off a cliff, so did all the companies.

We may think of this lesson when we look at the narrow market of last year, with just seven Big Tech stocks contributing over half the S&P 500’s return. While concentration may be exhilarating on the way up, one bad year can destroy decades of good returns.

The key, like most things in life, is moderation. It’s ok if we invest a portion of our money in promising new technologies or a handful of companies we believe in. But we should also not overextend ourselves and over-concentrate in one sector, no matter how attractive it appears. Human knowledge is limited and, as much we hate to admit it, even the smartest people are wrong a good portion of the time.

Key Wealth Principles

- A foundation of good habits is more important than fancy techniques

- Invest in quality businesses at an attractive price

- Build a portfolio of good businesses in different industries

- Maintain appropriate reserves and income sources

- Consider your financial circumstances, goals, and risk exposure

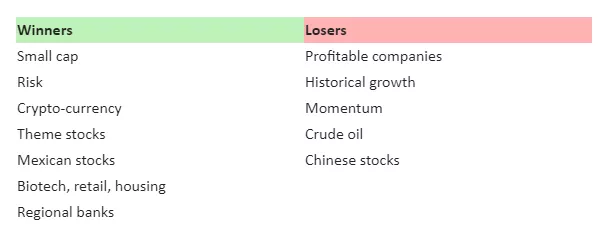

Last Month’s Winners and Losers

The year ended with a big move toward risky assets, such as small cap stocks, theme stocks, biotech, regional banks, and crypto-currency. Companies with strong profitability and historical growth underperformed, as did crude oil and Chinese stocks.

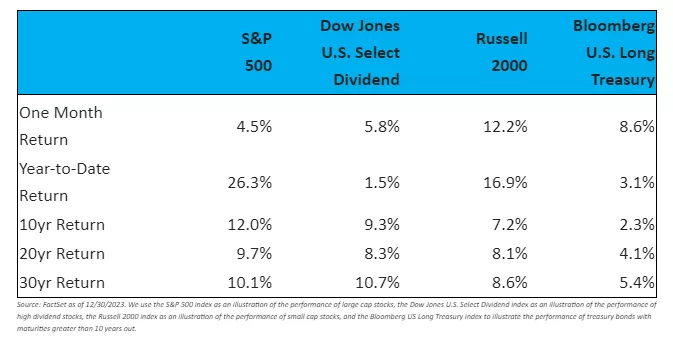

For the year, it was similar. Risky assets did very poorly in 2022 but bounced back in 2023. This was especially notable among Big Tech stocks and theme stocks. The only areas that were negative in the U.S. were highly interest-sensitive assets like long-term bonds and utilities. Chinese stocks were also negative for the year.

Stocks

The S&P 500 had a strong recovery last year from its losses in 2022. But over half of its return came from a mere seven stocks, all of which are Big Tech stocks. These stocks trade at high valuation multiples and comprise close to 30% of the index’s weight.

While things look promising with the development of artificial intelligence and other growth avenues, there is always a risk in concentrating your wealth in a sector that is expensive and moves together.

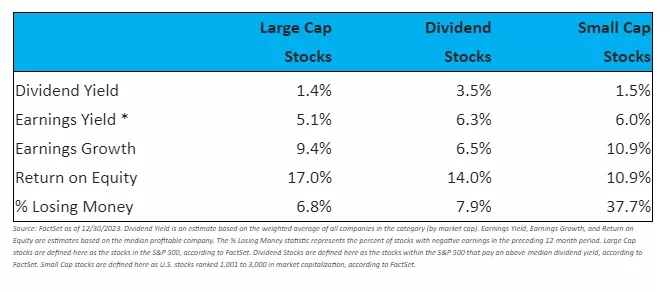

Looking at the characteristics of different equity markets, they seem appealing to long-term investors. Earnings yields average around 5-6%, depending on which segment of the market you’re looking at, and earnings growth expectations range from 6% to 11%, depending on the segment. When I look at individual stocks, I do not have a problem finding ones I think are appealing from a value perspective.

* “Earnings yield” is an investor’s share of earnings for every dollar invested (i.e., earnings per share / price per share). It’s the same as the more famous Price / Earnings (P/E) ratio, but expressed as a yield rather than as a multiple. I use it to compare stocks more clearly with bonds and other asset classes.“Equity Risk Premium” equals the Earnings Yield minus the 10-year Treasury Inflation Protected Securities yield.

Income Investing

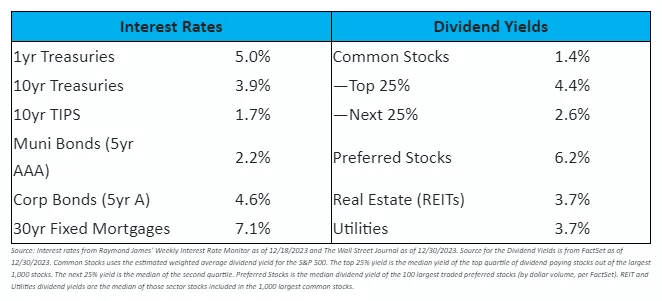

Long-term interest rates continued to fall last month while short-term interest rates held steady. This has been driven by market expectations of the Federal Reserve cutting rates over the next year, assuming inflation keeps dropping. The market expects around 2.3% average inflation over the next 10 years.*

I can see that happening, but I would caution that the monthly core inflation reports have stayed pretty steadily in the 3-4% range over the last year and there have not been signs so far of this dropping to the Federal Reserve’s target of 2% inflation. So if inflation stays in this range, rates may stay in this range too.

I would consider long-term bonds to be somewhat overvalued as current rates do not compensate for the risk of inflation coming in worse than expected and of ongoing federal budget deficits requiring continuous bond issuances.

* Implied inflation expectations are derived from taking the 10-Year Treasury rate and subtracting the 10-Year Treasury Inflation Protected Securities (TIPS) rate. For example, if the yield on 10-year treasuries is 2.8% and the yield on 10-year TIPS is 0.4%, they are roughly equivalent investments if inflation comes in at the difference (2.8% - 0.4% = 2.4%).

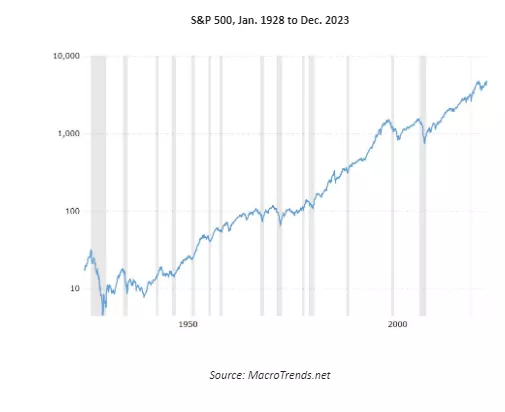

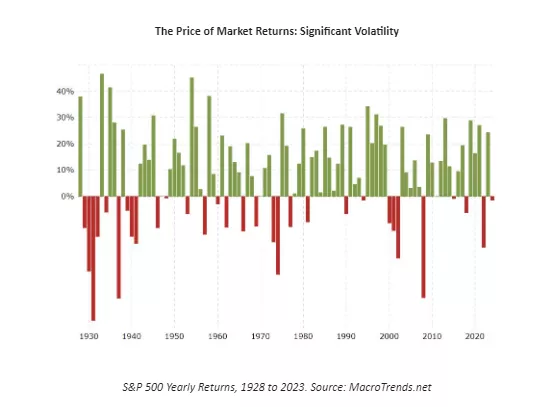

The Long View

For the last 20, 30, and 100 years, stocks have averaged around an 8-10% return, driven by dividend yield, reinvestment of earnings, and earnings growth. Long-term bonds have yielded about 5% on average over the last century while inflation has been about 3%.

Throughout this period, there have been major upheavals, such as the Great Depression, World War II, The Korean War, The Vietnam War, dropping the gold standard, 1970s high inflation, 1987’s Black Monday Crash, the Dot.com bust, the 9/11 terror attacks, the Global Financial Crisis, and the Covid Crash, among others.

These events led to severe market downturns about once every decade, with a median price decline of 33% and a median time to recover back to the previous high of 3.5 years. If we were to include dividends, the recovery to previous highs is actually a little faster. *

Meanwhile, a 3% inflation rate results in a 59% decline in the value of a dollar over 30 years. This means that people who retire at 60 years old on a fixed income face a high risk of a lower quality of life as they get further into retirement. *

* Source: Morningstar Direct via cfainstitute.org, FactSet. Past performance is not necessarily indicative of future performance. Depreciation of the dollar: $1 / (1 + 3%)^30 = $0.41 real value 30 years later.

Market Outlook

Now I’ll put on my “Nostradamus Hat” and make some predictions, for whatever they’re worth:

- Inflation will average 2-4% over the next 10 years.

- Interest rates will fall in the 3-6% range for 10yr Treasuries over the next several years, in line with inflation and historical experience.

- The economy will grow 2-3% in real terms over the next several years, though we will probably slip into a recession this year.

- Stocks will average an 8-10% return over the next 10+ years. After subtracting inflation, this will translate into about a 5% real return. There is likely to be at least one big decline every decade or so.

From the standpoint of where you and your family will be in 30 years, none of this matters. What matters is finding good quality investments that are likely to grow over the decades. For this reason, I largely ignore my own general market forecast and invest whenever I find a business that I am confident in and that trades at an attractive valuation.

More By This Author:

Creating A Legacy: Intergenerational WealthIs A Hard Rain A-Gonna Fall?

When The Unexpected Happens

Comments

Log in or sign up to join the conversation.