Municipal Bonds: Supply & Demand, Taxes & Infrastructure

In 2021, inflows to municipal bond funds have been strong (demand has been exceptionally high), outstripping supply. This disconnect has forced large municipal bond fund managers to be less selective in their credit selection process to keep up with demand. This is concerning because selectivity is key within the municipal bond market, especially for high-yield municipal bond funds.

This lack of selectivity is forcing some funds to increase positions in lower-rated credit. If the markets go awry, this is an area that could magnify drawdowns if not managed appropriately.

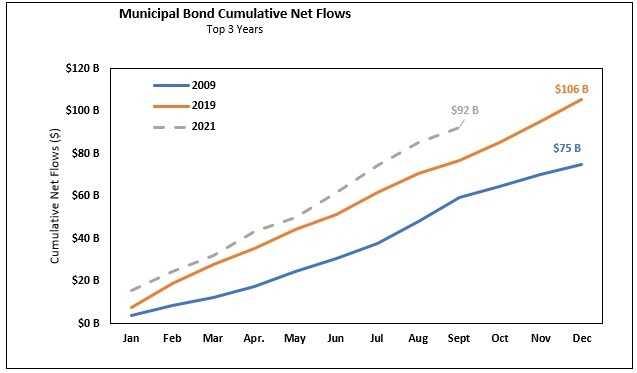

Municipal market demand - 2021

For perspective, as of the end of September, Morningstar data show that municipal bond funds boasted $92 billion of net inflows, currently the largest year-to-date net inflow on record and potentially on track to beat the 2019 full-year record of $106 billion.

Source: Morningstar Direct. As of Sept. 30, 2021.

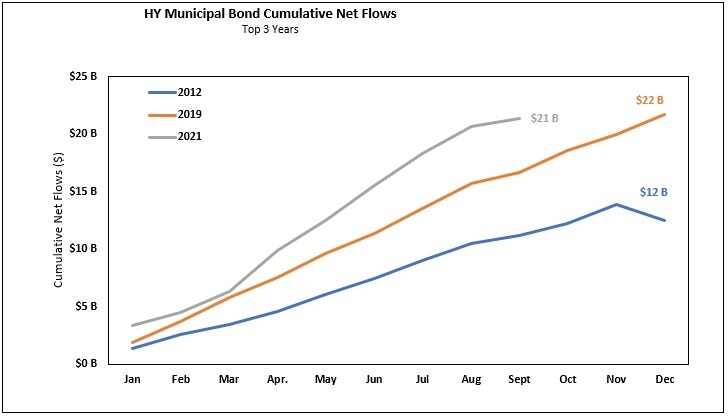

A much smaller segment of the municipal bond fund market is high yield (or sub-investment grade). This segment has pulled in $21 billion of net inflows year-to-date and is also the largest year-to-date net inflow on record. It also is likely to best the 2019 full-year record, which was $22 billion.

Source: Morningstar Direct. As of Sept. 30, 2021.

2021 demand drivers

As in 2019, this influx of flows can be largely explained by strong technical demand, which is driven by the following:

- Strong tax revenues and federal aid: From March 2020 to March 2021, tax revenues jumped a massive 19%1 as the economy reopened, improving the credit fundamentals of municipal bond issuers. This is further bolstered by the unprecedented $150 billion in federal aid to state and local governments from the 2020 CARES Act and more than $350 billion from the 2021 American Rescue Plan.

- Potential policy change: Municipal bonds are extremely sensitive to policy changes, especially tax increases such as the proposal President Biden released in March 2021. The potential for taxes to go up drove municipal bond demand higher as individuals looked toward investments that receive more favorable tax treatment.

Policy-driven supply and demand outlook

While there is no agreement yet on infrastructure policy and attendant tax changes, several proposals could affect issuance and demand:

Supply improvement - Bipartisan infrastructure deal

- The administration has put a strong focus on passing an infrastructure bill that is aimed at rejuvenating transportation systems, water, electric, broadband and facility (buildings, schools, childcare) projects. This would call for additional funding from two main areas, namely tax increases (discussed below) and new municipal bond initiatives. Here we highlight three initiatives that would favor and promote bond issuance, which could adversely impact municipal bond prices.

Source: Barclays: An Early Start to Tax Season.

Demand improvement – Tax increases

- Relative to President Biden’s initial tax policy proposal in March 2021, Democrats released a less progressive proposal in August 2021. Nonetheless, it comes with a slew of changes, most notably increases to individual and corporate tax rates. If passed, these changes would continue to support high demand for municipal bonds as individuals and institutions will become more motivated to reduce their tax bill.

- Another popular topic is potential changes to the state and local tax (SALT) deduction. Currently, the SALT deduction permits taxpayers who itemize when filing federal taxes to deduct certain taxes paid to state and local government (up to $10,000). If the SALT deduction cap was removed or increased, this could reduce municipal bond demand and negatively impact tax revenues seen by municipalities. While there was no mention of a change in the recent proposal, it is unclear if these changes would be included in the final bill.

Source: taxfoundation.org

While the policy changes could be favorable for the municipal bond market, especially for long-term fundamentals, they are far from finalized, so issuers could take a wait-and-see approach before bringing any new issues to market. In the short term, this could cause issuance to be subdued.

What to watch for?

By design, high yield municipal bond funds carry larger allocations to credit risk relative to investment-grade municipal bond funds. Over the last five years, strong demand and limited supply has forced most large high yield bond funds to take lofty positions in a riskier and illiquid area of the municipal market: non-rated (NR) securities. While exposure to NR securities is warranted, having the ability to be selective and maintain a lower level helps protect the downside. Given the policy-driven technical outlook and downside risk associated with NR securities, some of the larger funds are turning away new investors in an attempt to not expose their funds to more risk than they have already been forced to take.

To understand how large funds are affected by exposure to non-rated securities, as of the end of September, we measured the five largest funds (display group) within the US Fund High Yield Municipal Bond universe (peer group) that have been active since 2008 and have the highest non-rated credit (securities) exposure. Currently, the display group averages 43% exposure to NR credit, relative to the 27% peer group average. Since Sept. 30, 2016 (five years ago), this exposure has increased by 1.6x for the display group and 1.2x for the peer group. Further, this same display group has struggled during market stress and tends to only outperform the peer group marginally over a longer time period.

Source: Morningstar Direct

Source: Morningstar Direct. Coronavirus Pandemic*: 2/20/2020 – 3/23/2020, Global Financial Crisis**: 1/1/2008-12/31/2008. Peer Group: US Fund High Yield Municipal Bond.

In addition to having higher levels of risk relative to the peer group, the five largest funds underperformed by 2% during the coronavirus pandemic and 5% during the Global Financial Crisis (GFC) of 2008-09 and only outperformed by 0.7% in the last five years.

What’s the solution?

For many investors, today’s low interest rate environment highlights the need to consider a wider opportunity set of funds to meet yield requirements. For taxable investors—even those who aren’t in the top tax bracket—municipal bond vehicles may help them achieve their desired outcomes.

At Russell Investments, we believe advisors and investors alike should consider nimbler alternatives that are discerning with bond selection and maintain lower non-rated exposure. These alternatives typically come in the form of funds with relatively lower asset sizes. Smaller asset sizes mean the portfolio manager can pick and choose which bonds they want for their strategy, and don’t have to feel compelled to buy riskier, less-than-desirable credits to fill the demand from a very large fund.

For investors with higher risk tolerance and in higher tax brackets, we recommend investing in high yield (sub-investment grade) tax-exempt fixed income funds. It’s important to note that non-rated securities typically carry sub-investment grade risk and are therefore found in high yield municipal funds. However, the foregoing point still stands, and investors should look for relatively smaller funds with relatively lower percentages of non-rated securities.

The bottom line

During periods of limited supply and strong inflows, larger municipal bond funds have historically struggled to be discerning when it comes to credit selection. This challenge may intensify this year as we wait for closure around potential policy changes. Although high yield municipal bond funds may warrant a place in an investor’s tax efficient portfolio, be mindful of outsized funds that have increased their positions in lower rated and—more importantly—non-rated issues that could magnify drawdowns if the markets become unhinged.

While high yield municipals certainly do have great long-run potential, we believe investors may want to consider smaller municipal funds that have the capacity and latitude to be very selective when adding NR securities, keeping the overall exposure at a more manageable level.

1 Bureau of Economic Analysis, U.S. Department of Commerce: National Income and Product Accounts https://apps.bea.gov/iTable/iTable.cfm?reqid=19&step=3&isuri=1&1921=survey&1903=86

Disclosures:

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. The information, analysis, and opinions ...

more