Over the last couple of weeks, we have been discussing the market’s advance from the lows and why retesting old highs was quite probable. To wit:

“The markets are close to registering a ‘golden cross.’ This is some of that technical ‘voodoo’ where the 50-day moving average (dma) crosses above the longer-term 200-dma. This ‘cross’ provides substantial support for stocks at that level and limits downside risk to some degree in the short-term.”

As I penned on Monday for our RIA PRO subscribers:

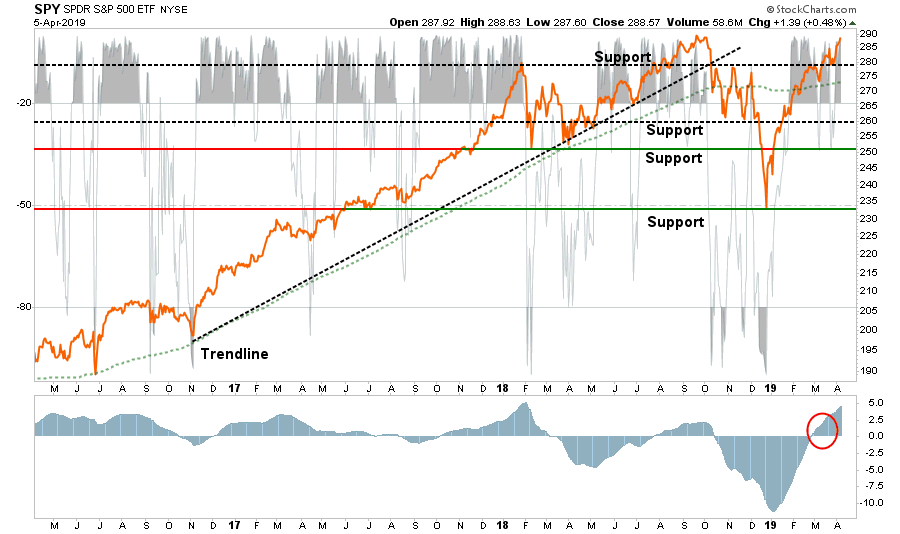

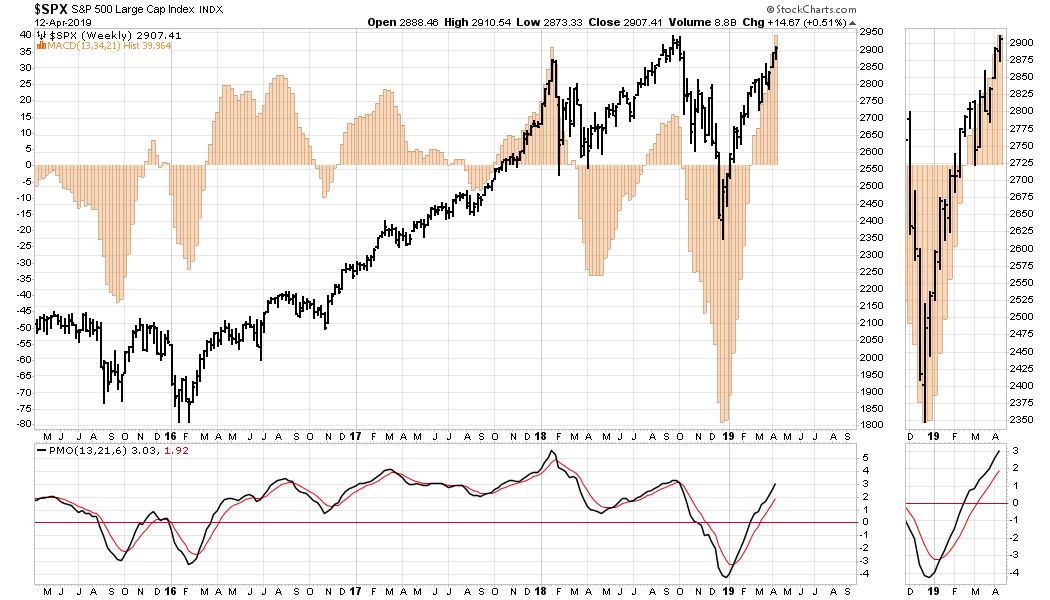

“As we discussed last week, the rally above, and retest of support at 280 sets up a test of all-time highs. I expect that will occur early next week. SPY is extremely overbought, so a test and failure at the highs will not be surprising.

- Short-Term Positioning: Bullish

- Last Week: Previously increased sizing to full weight.

- This Week: Hold

- Stop-loss moved up to $280″

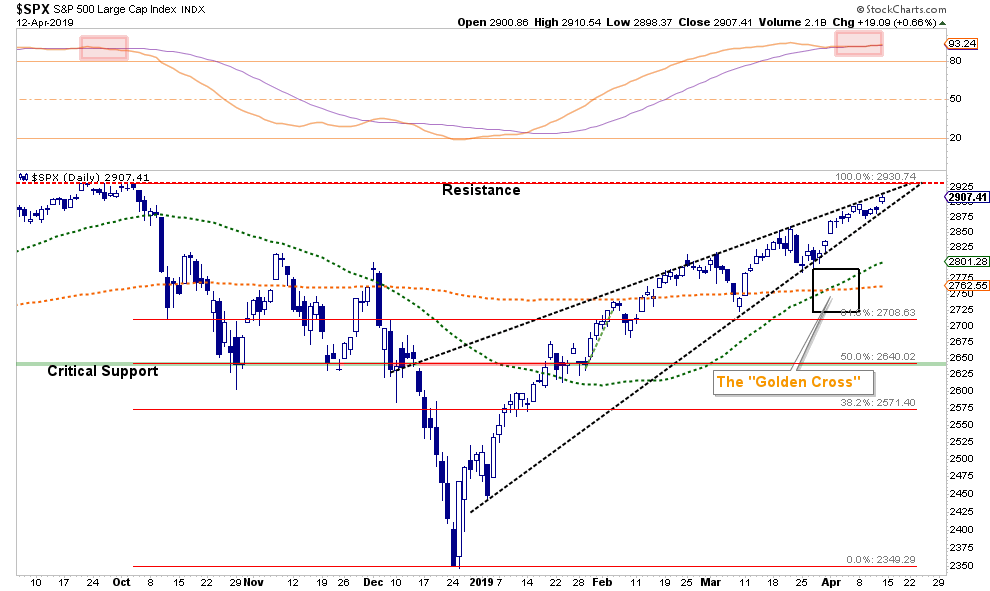

More importantly, on Friday, the markets broke above short-term resistance and the psychological barrier of 2900. This will likely get the bulls all excited over the weekend to make an attempt for all-time highs.

While the bullish bias is definitely behind investors currently, there are concerns relative to the current risk/reward backdrop.

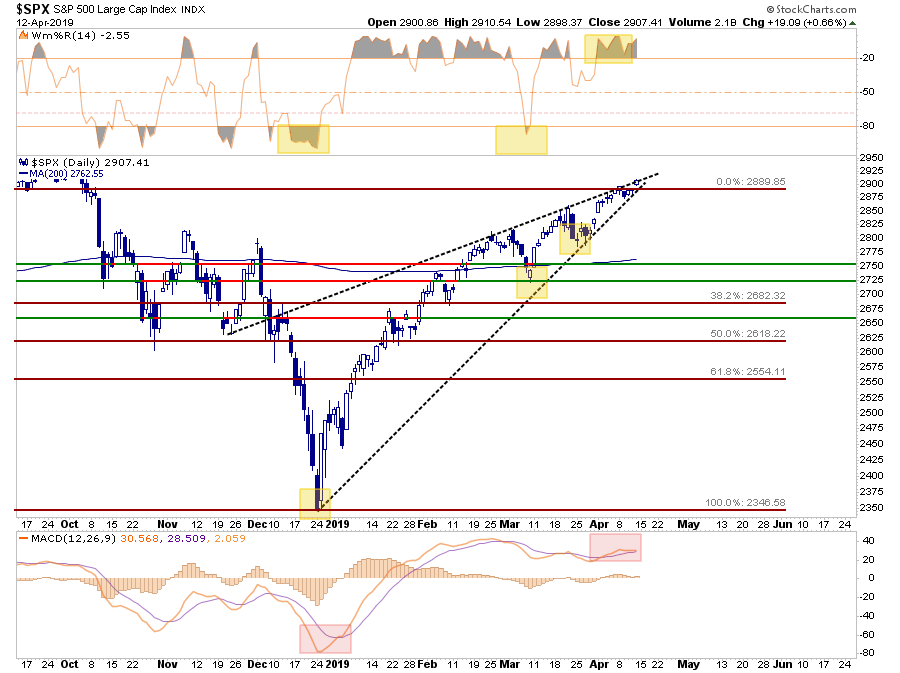

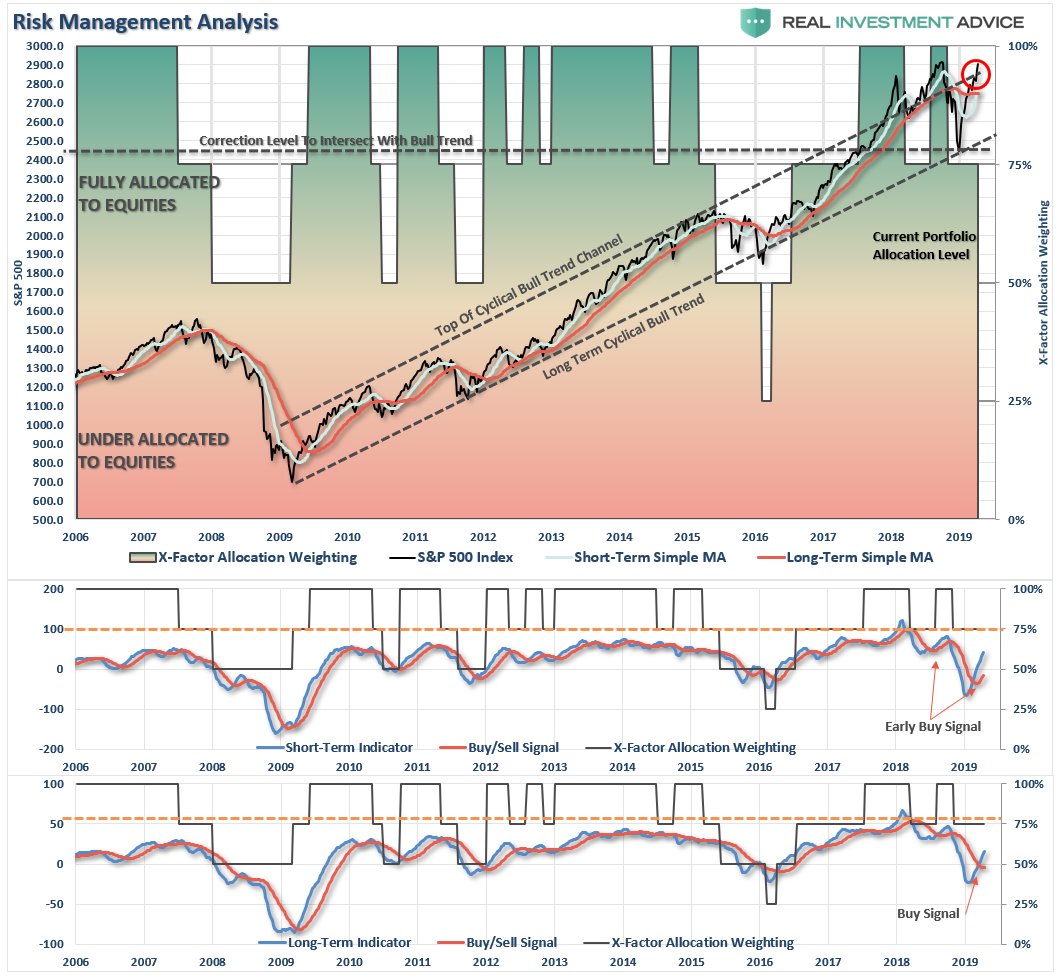

As shown in the chart above, the market is not only back to more extreme overbought levels, it is also close to registering a short-term sell signal. With prices now compressed into a very tight range, the risk of a downside break has risen. Drew Zimmerman from Polar Futures Group also made some very astute observations on Friday.

“Is it the middle of April or the middle of August? The weekly trading volume of shares on the US indices and the number of futures contracts that traded this week was the lowest since last summer and among the lowest weekly levels of the past several years. This low volume has reduced price volatility with the VIX index trading back to down to levelsnot seen since the beginning of October last year before the equity price decline started. Even the volatility in the G7 currencies is the lowest it has been since the middle of 2014!

So, it’s quiet out there….what does that mean? Equity markets are only a couple of percentage points from all-time highs, things must be good! The central banks have done their job, they have all gone back to accommodative policy stances, and China easing more aggressively. We have gone from worries of a global slowdown to not worrying at all because the central banks have our back, and in that environment taking more risk pays. The central banks must know what is best right?

However, when we see broad markets get this quiet, it usually means we are about to get a rude surprise. When things coil up, it is common to see some explosive moves. Given the very low level of volatility, it may be an opportune time to buy some protection.”

We agree with the last statement. This is supported by the extreme level of the current “buy” signal as shown in the shaded orange bar graph in the chart below. These rare extreme extensions occur at extremes of sell-offs and rallies.

As stated, we definitely agree and as such are maintaining our current equity exposure, with an overweight positioning in cash and fixed income. While this allocation structure is currently providing some performance drag, it is also greatly reducing overall portfolio volatility which we think we will be well rewarded for over the next four to six months.

This is generally where someone with a reading disability sends me an email:

“But you are always bearish”

“The market has not been this oversold at any point in the last 20-years, on a monthly basis, as shown in the chart below.

The other bit of good cheer for the bulls is that unlike the previous two starts to more protracted bear markets, the long-term monthly uptrend has not been broken, yet. As noted above, the market is sitting on that uptrend support line which began in 2009.

At this point, the risk/reward for traders is clearly sided to the bulls…for now.”

So, for the reading impaired:

We are carrying reduced equity long positions, we are overweight cash, and fixed income because the deeply oversold condition which previously existed has been entirely reversed. This has occurred at a time where the earnings and economic backdrop are deteriorating, not improving.

Simply, the risk/reward setup is no longer as favorable as it was in December.

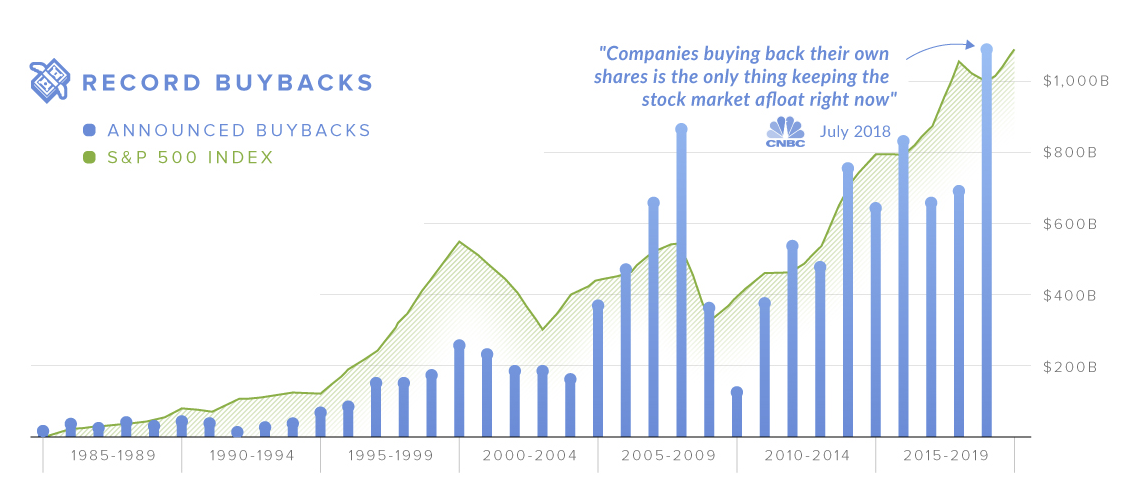

Make Stock Buybacks Illegal?

“Few topics prompt as powerful (and violent) a response from financial professionals as what the role of financial buybacks is in determining stock prices.

One group, largely those bulls who after a decade of central bank manipulation still believe that markets are efficient and unrigged, argue that stock buybacks have no impact on stock prices.

The other group, those who actually understand that if there is a trillion dollars in price indiscriminate stock bids is the single most effective way to boost stock prices, know that corporate buybacks, which until not too long ago were banned, and which over the past decade emerged as the single biggest source of stock purchases, are one of the two most important factors behind the all time highs in the stock market (the other being the Fed, whose policies have allowed companies to issue debt with record low yields, allowing them to fund these trillions in buybacks).” – Zerohedge, April 4, 2019

It is an interesting debate.

What makes this debate particularly notable, and as noted above, most people don’t remember that share repurchases were banned for decades prior to President Reagan in 1982.

So, why were they banned in the first place? Via Vox:

“Buybacks were illegal throughout most of the 20th century because they were considered a form of stock market manipulation. But in 1982, the Securities and Exchange Commission passed rule 10b-18, which created a legal process for buybacks and opened the floodgates for companies to start repurchasing their stock en masse.”

This isn’t the first time we have reversed policy previously put into place to avert Wall Street from taking advantage of the market to fill their own coffers.

The Crash of 1929

Leading up to the crash of 1929, banks, which were entrusted with people’s life savings, were on both sides of the investment game. They loaned money to investors to speculate with, and they were speculating in the markets themselves. What could possibly go wrong?

“Stocks are now at a permanently high plateau” – Dr. Irving Fisher, 1929

Following the crash, the SEC was formed to “police” the financial markets and protect investors from the predatory practices of Wall Street and the Banks. Part of that process was the passage of the Glass-Steagall act in 1933 to separate banking and brokerage activities in order to build a wall between the source of funds (bank deposits) and the use of funds (speculative investment.)

For nearly 70-years the markets functioned properly. However, in 1999, Congress repealed Glass-Steagall under tremendous pressure from the major banks who lobbied heavily to gain access to the massive revenue being generated from the “dot.com” mania.

It didn’t take long.

Just seven short years later, the world came apart in the biggest crisis/recession since the “Great Depression.” Not surprisingly, at the very center of the financial and economic destruction, were the major banks taking advantage of the investing public once again.

Coincidence?

“History may not repeat, but it often rhymes.” – Mark Twain

As noted, for decades stock buybacks were banned due to the problem of potential market manipulation. It is important to remember that regulations are NEVER passed in ADVANCE of a problem, they are always imposed in RESPONSE to a problem.

What Are We Talking About?

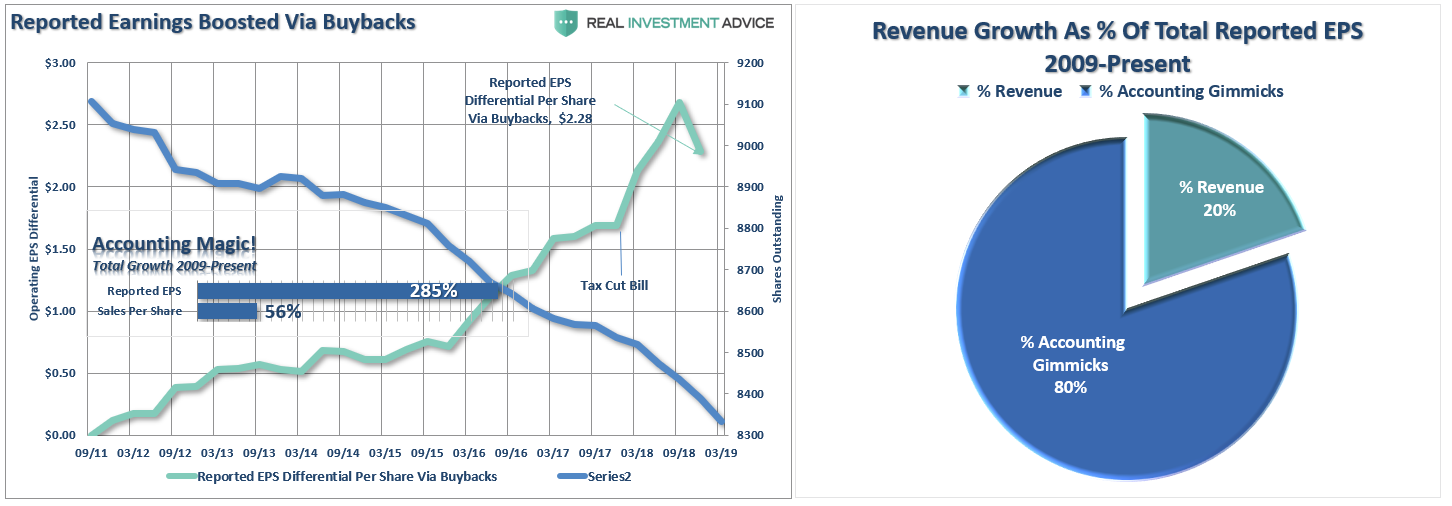

Like stock splits, share repurchases in and of themselves are not necessarily a bad thing, they are just the least best use of cash. Instead of using cash to expand production, increase sales, acquire competitors, or buy into new products or services, the cash is used to reduce the outstanding share count and artificially inflate earnings per share. Here is a simple example:

- Company A earns $1 / share and there are 10 / shares outstanding.

- Earnings Per Share (EPS) = $0.10/share.

- Company A uses all of its cash to buy back 5 shares of stock.

- Next year, Company A earns $0.20/share ($1 / 5 shares)

- Stock price rises because EPS jumped by 100%.

- However, since the company used all of its cash to buy back the shares, they had nothing left to grow their business.

- The next year Company A still earns $1/share and EPS remains at $0.20/share.

- Stock price falls because of 0% growth over the year.

This is a bit of an extreme example but shows the point that share repurchases have a limited, one-time effect, on the company. This is why once a company engages in share repurchases they are inevitably trapped into continuing to repurchase shares to keep asset prices elevated. Share repurchases divert ever-increasing amounts of cash from productive investments and takes away from longer-term profit and growth.

As we just discussed last week, since the recessionary lows, much of the rise in “profitability” has come from a variety of cost-cutting measures and accounting gimmicks rather than actual increases in top-line revenue. While tax cuts certainly provided the capital for a surge in buybacks, revenue growth, which is directly connected to a consumption-based economy, has remained muted.

The reality is that stock buybacks create an illusion of profitability. Such activities do not spur economic growth or generate real wealth for shareholders, but it does provide the basis for with which to keep Wall Street satisfied and stock option compensated executives happy.

Don’t believe me?

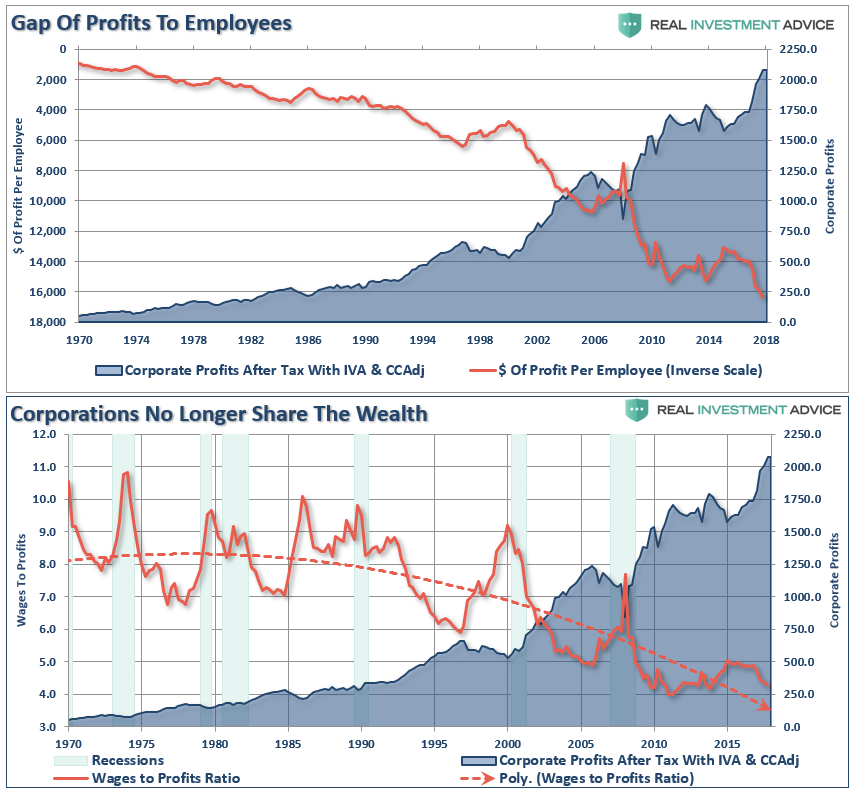

In 1982, according to the Economic Policy Institute, the average CEO earned 50 times the average production worker. Today, the CEO Pay Ratio’s increased to 144 times the average worker with most of the gains a result of stock options and awards.

As shown in the chart below, clearly profits aren’t being shared with “working class stiffs.”

Tax Cuts For Corporations

As I wrote in early 2018. while it was widely believed that tax cuts would lead to rising capital investment, higher wages, and economic growth, it went exactly where we said it would. To wit:

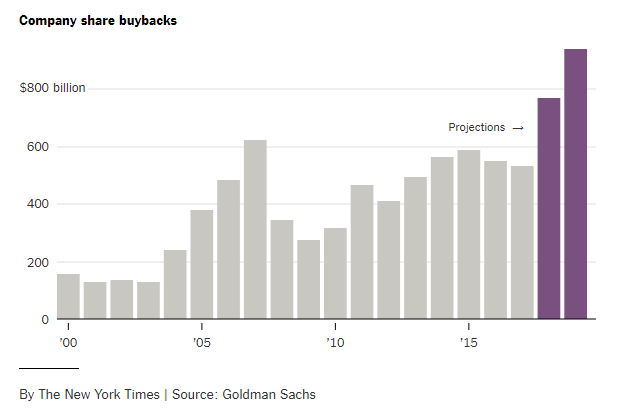

“Not surprisingly, our guess that corporations would utilize the benefits of ‘tax cuts’ to boost bottom line earnings rather than increase wages has turned out to be true. As noted by Axios, in just the first two months of this year companies have already announced over $173 BILLION in stock buybacks. This is ‘financial engineering gone mad'”

Share buybacks are expected to hit another new record by the end of 2019.

Let’s clear up a myth used to support the benefit of stock buybacks:

“Share repurchases aren’t bad. It is simply the company returning money to shareholders.”

Here is the issue:

Share buybacks only return money to those individuals who sell their stock. This is an open market transaction. For example, when Apple (AAPL) buys back some of their outstanding stock, the only people who receive any capital from the buyback are those who sold their shares.

So, who are the ones mostly selling their shares?

As noted above, it’s the insiders, of course, as changes in compensation structures since the turn of the century has become heavily dependent on stock issuance. Insiders regularly liquidate shares which were “given” to them as part of their overall compensation structure to convert them into actual wealth. As the Financial Times recently penned:

“Corporate executives give several reasons for stock buybacks but none of them has close to the explanatory power of this simple truth: Stock-based instruments make up the majority of their pay and in the short-term buybacks drive up stock prices.”

A recent report on a study by the Securities & Exchange Commission found the same:

- SEC research found that many corporate executives sell significant amounts of their own shares after their companies announce stock buybacks, Yahoo Finance reports.

What is clear, is that the misuse and abuse of share buybacks to manipulate earnings and reward insiders has become problematic. As John Authers recently pointed out:

“For much of the last decade, companies buying their own shares have accounted for all net purchases. The total amount of stock bought back by companies since the 2008 crisis even exceeds the Federal Reserve’s spending on buying bonds over the same period as part of quantitative easing. Both pushed up asset prices.”

In other words, between the Federal Reserve injecting a massive amount of liquidity into the financial markets, and corporations buying back their own shares, there have been effectively no other real buyers in the market.

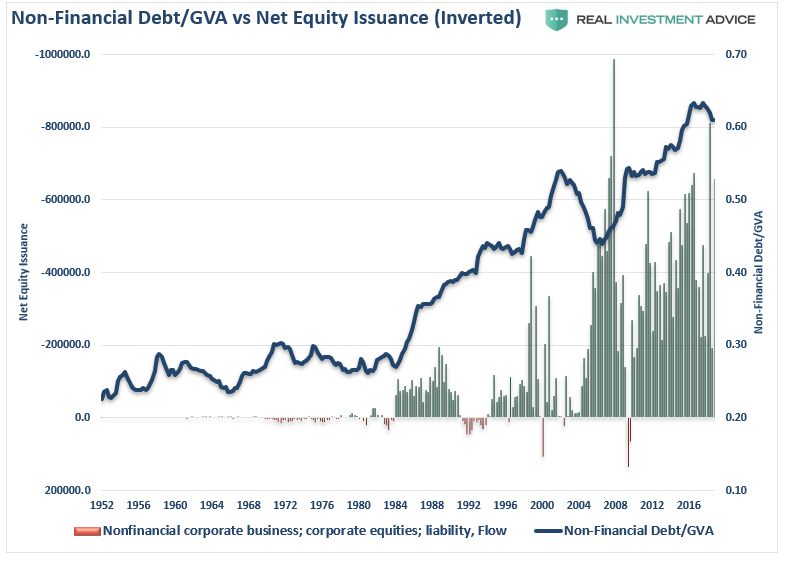

Don’t Have Cash, Use Debt

The other problem with the share repurchases is that is has increasingly been done with the use of leverage. The ongoing suppression of interest rates by the Federal Reserve led to an explosion of debt issued by corporations. Much of the debt was not used for mergers, acquisitions or capital expenditures but for the funding of share repurchases and dividend issuance.

Furthermore, with 62% of investment grade debt maturing over the next five years, there are a lot of companies that are going to wish they didn’t buy back so much stock. This debt load will become problematic if rates rise markedly, further deterioration in credit quality locks companies out of refinancing, or if there is a recessionary drag which forces liquidation of debt. This is something Dallas Fed President Robert Kaplan warned about:

U.S. nonfinancial corporate debt consists mostly of bonds and loans. This category of debt, as a percentage of gross domestic product, is now higher than in the prior peak reached at the end of 2008.

A number of studies have concluded this level of credit could ‘potentially amplify the severity of a recession,’

The lowest level of investment-grade debt, BBB bonds, has grown from $800 million to $2.7 trillion by year-end 2018. High-yield debt has grown from $700 million to $1.1 trillion over the same period. This trend has been accompanied by more relaxed bond and loan covenants, he added.

This was recently noted by the Bank of International Settlements.

“If, on the heels of economic weakness, enough issuers were abruptly downgraded from BBB to junk status, mutual funds and, more broadly, other market participants with investment grade mandates could be forced to offload large amounts of bonds quickly. While attractive to investors that seek a targeted risk exposure, rating-based investment mandates can lead to fire sales.”

Make Stock Buybacks Illegal?

Now that you understand the background, and who share buybacks actually benefit, you can understand the reasoning behind wanting to ban them once again.

While share repurchases by themselves may indeed seem somewhat harmless, it is when they are coupled with accounting gimmicks, and massive levels of debt to fund them, in which they become problematic. This issue was noted by Michael Lebowitz:

“While the financial media cheers buybacks and the SEC, the enabler of such abuse idly watches, we continue to harp on the topic. It is vital, not only for investors but the public-at-large, to understand the tremendous harm already caused by buybacks and the potential for further harm down the road.”

However, there are significant consequences in resetting the system.

“Eliminating buybacks would immediately force firms to shift corporate cash spending priorities, impact stock market fundamentals, and alter the supply/demand balance for shares… The potential restriction on buybacks would likely have five implications for the US equity market: (1) slow EPS growth; (2) boost cash spending on dividends, M&A, and debt paydown; (3) widen trading ranges; (4) reduce demand for shares; and (5) lower company valuations.” – David Kostin, Goldman Sachs

If you are a short-term stock market bull, you will probably not want that. However, as my friend Doug Kass notes there are long-term benefits to reforming the system and putting corporations back onto a more“economically friendly” level:

My plan is simple.

Make buybacks illegal.

Allow companies to dividend out cash tax-free, like a buyback. This keeps companies out of the market and prevents them from manipulating their own stock, which often benefits company insiders who are selling.

Then the decision of what to do with corporate cash becomes more pure.

It no longer will be a choice of trying to prop up a stock versus spending it on the business.

Companies will still be left to do with their own cash what they want.

This is the other big problem, the fact that dividends are taxed, but buybacks are not.

That doesn’t make too much sense to me.”

In the end, the SEC will move to once again ban stock buybacks as they did once before.

Unfortunately, it will be in response to (not to mention the pressure of public outrage) the next financial crisis that devastates a vast majority of the U.S. economy.

But that is just the way the system works.

Market & Sector Analysis

Data Analysis Of The Market & Sectors For Traders

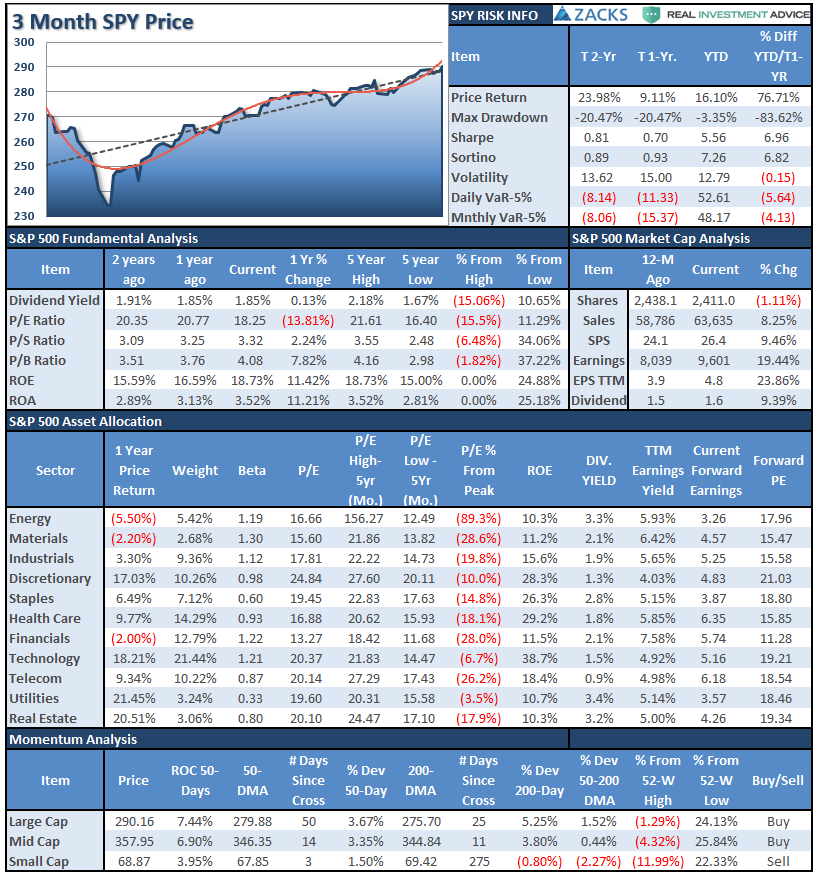

S&P 500 Tear Sheet

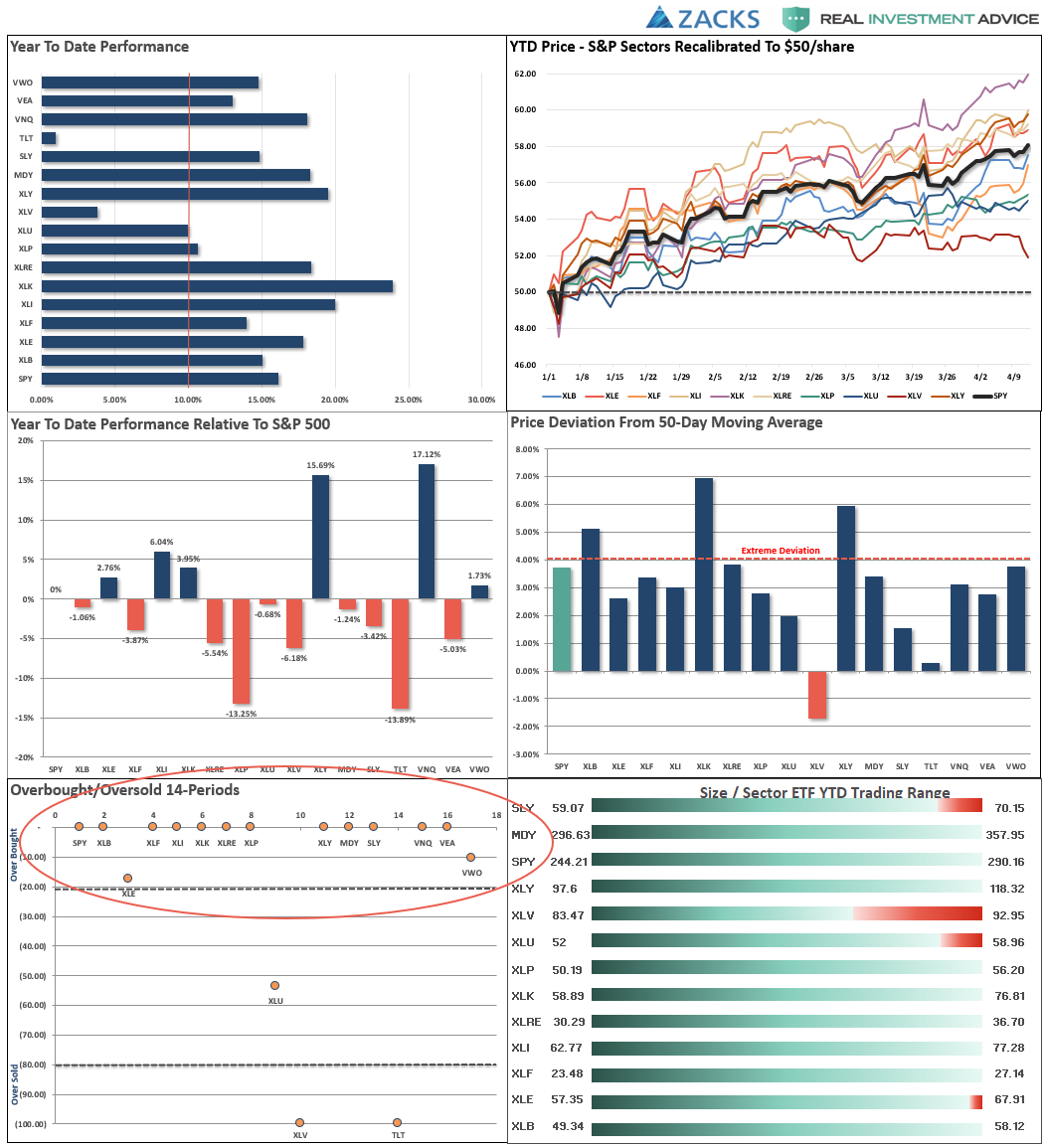

Performance Analysis

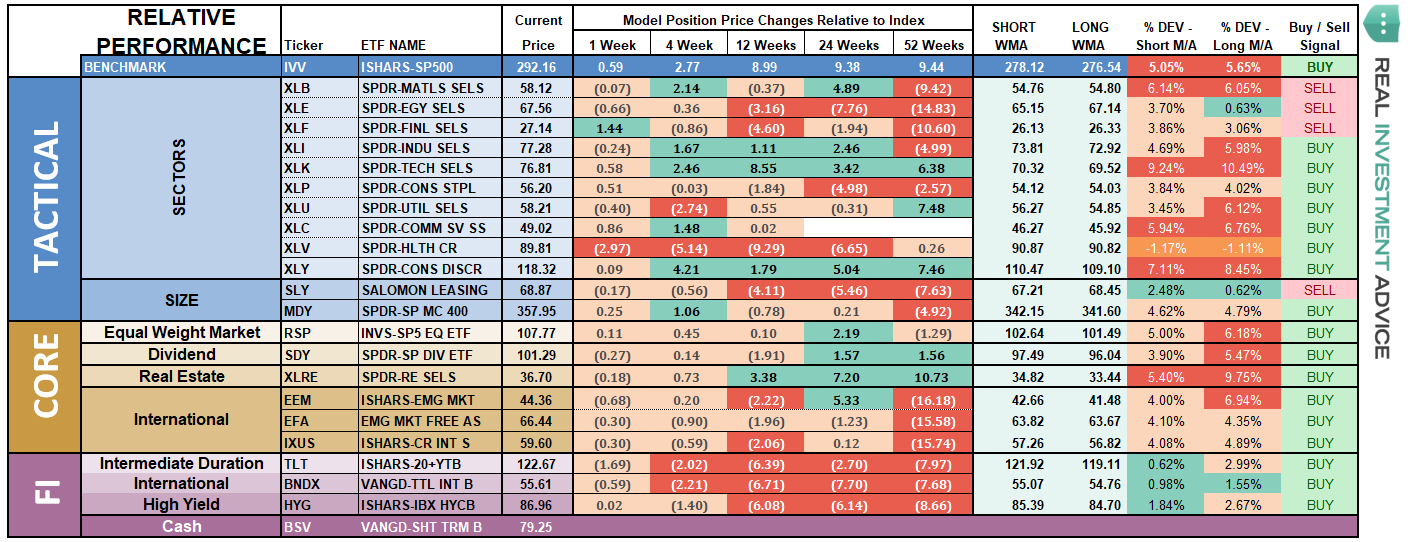

ETF Model Relative Performance Analysis

Sector & Market Analysis:

Be sure and catch our updates on Major Markets (Monday) and Major Sectors (Tuesday) with updated buy/stop/sell levels

Sector-by-Sector

Looking at sectors on a “relative performance” basis to the S&P 500 we have seen some rotations in leadership over the last week.

Improving – Energy, Materials

With the pick up in oil prices, the Energy sector has performed better as of late. Last week, energy finally broke above its 200-dma but is still lagging many other sectors of the market. Current, with oil prices very overbought, look for a pullback in energy shares soon. Take profits for now, and if the sector can hold support we can increase our holdings accordingly. Materials have surged over the last couple of weeks on hopes of a “trade war” resolution. With the sector extremely overbought, take profits, rebalance risk, and tighten up stops.

Current Positions: 1/2 Position in XLE, XLB

Outperforming – Technology, Industrials, Discretionary

Discretionary and Technology broke out to new all-time highs last week, and continue to push higher this past week as well. While participation continues to become more concentrated in a smaller number of sectors, the bullish bias persists for now with 50-dma’s above 200-dma’s and momentum trending positively. These sectors are all overbought, so take some profits, rebalance portfolios, raise stops but remain long for now

Current Positions: XLI, XLY, XLK – Stops moved from 200 to 50-dma’s.

Weakening – Real Estate, Utilities, Communications

Despite the “bullish” bias, the more defensive sectors of the markets, namely Utilities and Real Estate, have continued to attract buyers. While Utilities recently corrected a small bit, Real Estate has not. Both sectors remain very extended and overbought. Communications has become much more bullishly biased as of late after successfully testing its 200-dma and the 50-dma crossing above the 200-dma. With the sector extremely overbought look for a correction which does not violate support to add to portfolios.

Current Position: XLU

Lagging – Healthcare, Staples, Financials

Staples recently had a very small correction which was not enough to resolve its overbought condition. However, Staples are testing previous highs as money continues to chase defensive sectors of the market. Financials, which has been struggling as of late due to the inversion of the yield curve, perked up this past week and finally broke out of its consolidation with better than expected earnings from JPM on Friday. With the performance of Financials is improving, it may attract more buyers over the next couple of weeks as it has underperformed the bulk of the rally from the December lows. Healthcare continues to struggle with repeated calls from political candidates for “Government sponsored health care.” This is very unlikely to happen, and Healthcare is likely setting up to gain from a rotation from offense to defense in the market. This is the only sector that oversold and currently sitting on support.

Current Positions: XLF, XLV, XLP

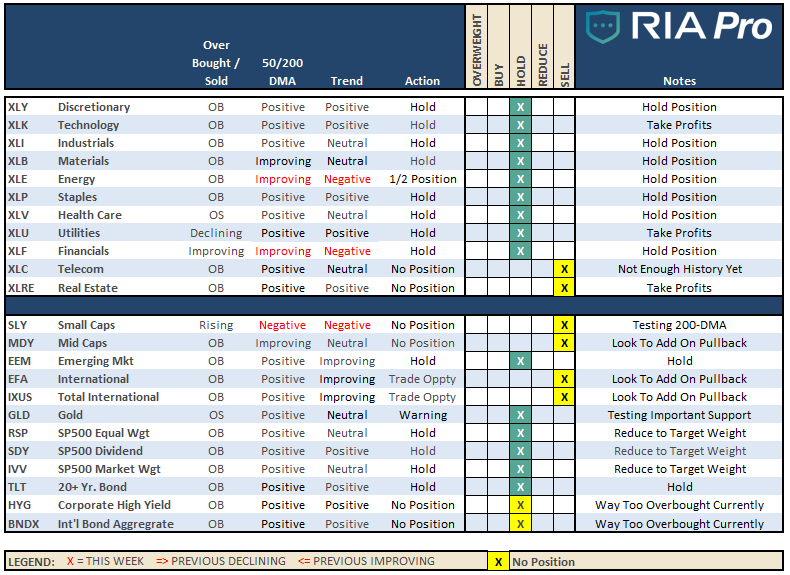

Market By Market

Small-Cap and Mid Cap – Small Cap stocks continue to lag the rest of the market and remain confined within the context of a broader downtrend. While small caps are challenging their 200-dma, a break above that level will make small-caps are more compelling play. Conversely, Mid-Caps are performing much better as of late and have broken out of its consolidation over the last couple of months. With the 50-dma crossing above the 200-dma, look for a pullback towards the 50-dma to increase exposure to Mid-caps.

Current Position: None

Emerging, International & Total International Markets

Emerging Markets continue to perform better as of late but are extremely overbought in the short-term. We are looking for a pullback which holds support to increase our holdings in that market.

Major International & Total International shares also are performing much better despite global economic weakness. This is probably misplaced optimism but nonetheless the technical backdrop has improved enough to warrant adding a position on a pullback that holds support and works off some of the extreme overbought condition.

Stops should remain tight at the running 50-dma which is also previous support.

Current Position: 1/2 position in EEM

Dividends, Market, and Equal Weight – These positions are our long-term“core” positions for the portfolio given that over the long-term markets do rise with respect to economic growth and inflation. Currently, the short-term bullish trend is positive and our core positions are providing the“base” around which we overweight/underweight our allocations based on our outlook.

Core holdings remain currently at target portfolio weights but all three of our core positions are grossly overbought. A correction is coming, it is now just a function of time.

Current Position: RSP, VYM, IVV

Gold – Gold continues to perform poorly despite concerns over the Fed, policy, and monetary policy. With gold building a bearish wedge below the 50-dma, the critical support level of $121 must be honored. Gold is very oversold in the short-term so any market sell-off in the next week will likely see gold bounce. Gold must get above $123.50 to make an attempt at higher levels.

Current Position: GDX (Gold Miners), IAU (Gold)

Bonds

The 10-year treasury popped up to 2.54% on Friday on rising inflationary pressures in recent reports. This is going to put the Fed into a very uncomfortable position of not raising the Fed Funds rate if prices and wages continue to advance. However, rates are simply bouncing back from a very oversold condition after the plunge from last November. This is setting up a very nice entry point to add additional bond exposure in the months ahead as we move into the summer months. Look for rates to touch 2.6% as a point to begin adding exposure to portfolios. There is a potential for rates to climb as high as 2.85%, but that move is quite unlikely in the current economic environment.

Current Positions: DBLTX, SHY, TFLO, GSY

High Yield Bonds, representative of the “risk on” chase for the markets, have continued to rally this past week and are now egregiously overbought. Take profits and rebalance risk accordingly. International bonds, which are also high credit risk, have been consolidating over the last couple of weeks, but remain very overbought currently which doesn’t over a high reward/risk entry point.

The table below shows thoughts on specific actions related to the current market environment.

(These are not recommendations or solicitations to take any action. This is for informational purposes only related to market extremes and contrarian positioning within portfolios. Use at your own risk and peril.)

Portfolio/Client Update:

No actions this past week were needed.

As we noted last week, there is currently little concern about the markets despite economic weakness popping up just about everywhere. For now, the market remains glued to headlines on trade, China stimulus, and the Fed. This will turn out to be ill-advised in the months ahead, but for now it remains “Party on Garth.”

With our near term buy signals in place, we continue to let our equity holdings ride the wave of the market and are looking to opportunistically take on opportunities as they present themselves. With earnings season now underway there will be bid under stocks as companies “beat” drastically lowered “expectations.”

So, for now, we are patient.

- New clients: We continue to onboard clients and move into specified models accordingly.

- Equity Model: We rebalanced all positions in the portfolio, with the exception of Boeing (BA), reducing overweight positions and adding to underweight positions.

- ETF Model: No changes. – Reviewing for rebalancing as needed.

Note for new clients:

It is important to understand that when we add to our equity allocations, ALL purchases are initially “trades” that can, and will, be closed out quickly if they fail to work as anticipated. This is why we “step” into positions initially. Once a “trade” begins to work as anticipated, it is then brought to the appropriate portfolio weight and becomes a long-term investment. We will unwind these actions either by reducing, selling, or hedging, if the market environment changes for the worse.

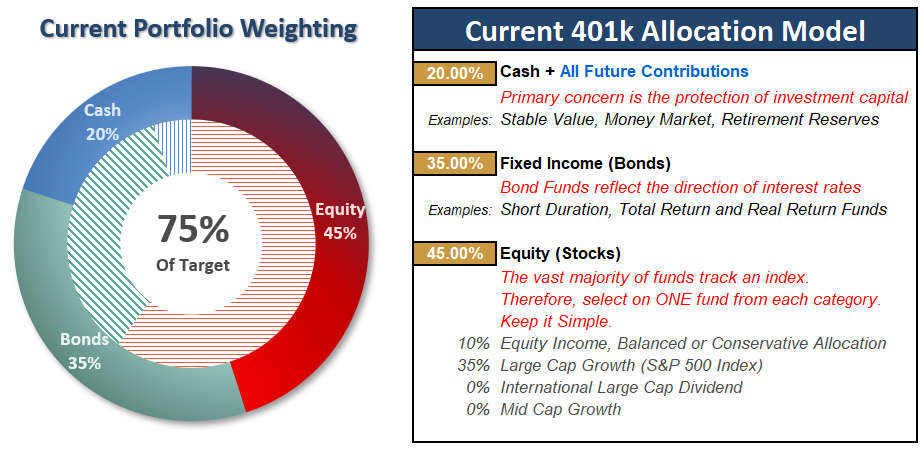

THE REAL 401k PLAN MANAGER

A Conservative Strategy For Long-Term Investors

There are 4-steps to allocation changes based on 25% reduction increments. As noted in the chart above a 100% allocation level is equal to 60% stocks. I never advocate being 100% out of the market as it is far too difficult to reverse course when the market changes from a negative to a positive trend. Emotions keep us from taking the correct action.

Don’t Let Your Emotions Take Control Of You

Bull markets have a tendency to suck the most investors in at the point to inflict the most possible pain.

That is the point we are currently at in the markets today. After a recovery rally from the lows many investors are now back to where they were in January of last year. The rally also tends to make investors forget the pain the endured during the previous decline.

If you feel like you “must get back into the market now,” you are probably allowing your emotions to get the better of you. This is why most investors tend to repeatedly buy tops and sell bottoms.

This market rally will stall. It will correct, and it will provide you a much better risk-reward entry point to increase equity exposure. Don’t allow short-term market movements to deviate you from your long-term investing goals.

Chasing performance is the absolute best way to destroy your investing outcome.

As noted last week, we now have both “buy” signals now in place which suggests that target allocations move to 100% equity exposure. However, with the market EXTREMELY overbought on a short-term basis and pushing up against longer-term trend lines, it will require patience to wait for a correction to increase exposure into.

In the meantime, we can prepare for this opportunity by continuing our actions we have recommended over the last several weeks.

- If you are overweight equities – take some profits and reduce portfolio risk on the equity side of the allocation. However, hold the bulk of your positions for now and let them run with the market.

- If you are underweight equities or at target – remain where you are until the market gives us a better opportunity to increase exposure to target levels.

Current 401-k Allocation Model

The 401k plan allocation plan below follows the K.I.S.S. principle. By keeping the allocation extremely simplified it allows for better control of the allocation and a closer tracking to the benchmark objective over time. (If you want to make it more complicated you can, however, statistics show that simply adding more funds does not increase performance to any great degree.)

401k Choice Matching List

The list below shows sample 401k plan funds for each major category. In reality, the majority of funds all track their indices fairly closely. Therefore, if you don’t see your exact fund listed, look for a fund that is similar in nature.

Comments

Log in or sign up to join the conversation.