Image Source: Pexels

Over the last few days, we have seen a small selection of the best scenarios currently on the table. We have already summarized some of them in the issue «Welcome to 2026, expect the unexpected!» However, the newly emerging nervousness is now being explained by a unusually large number of theories – apparently, everyone is allowed to have a go. So let’s take a closer look at a few of them.

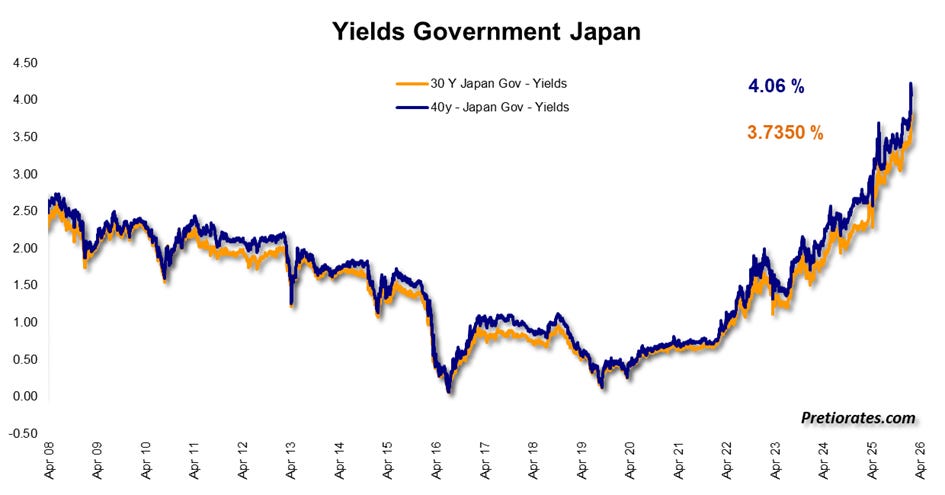

The long-missed volatility in the bond markets has finally made itself felt – and not shyly. The rising yields in the Japanese bond market should now be flashing on the radar screens of every investor worldwide.

(Click on image to enlarge)

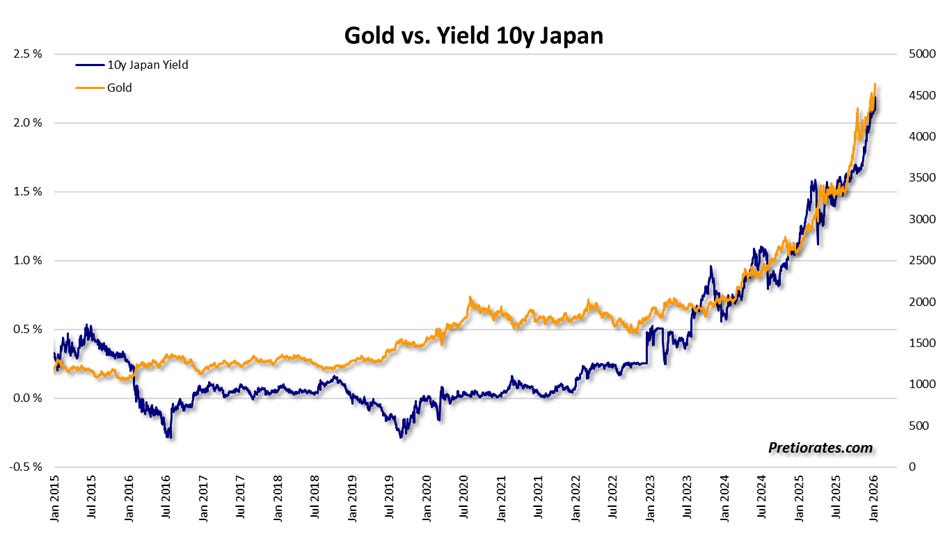

Good news for gold investors: Japanese market yields also show a high correlation with the price of gold.

(Click on image to enlarge)

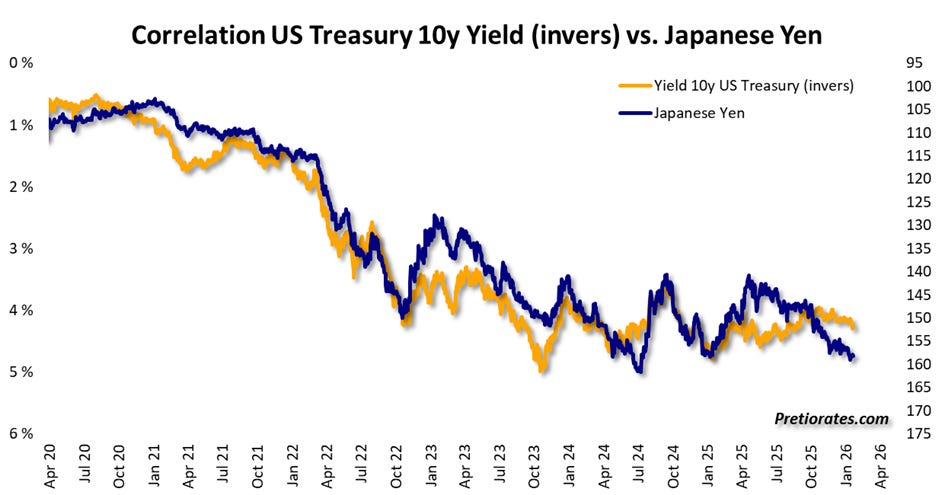

To many, Japan seems like a distant island somewhere in the Pacific. In global finance, however, the Land of the Rising Sun is a heavyweight. Over the past 30 years, yen carry trades have been used to take out enormous loans in yen at extremely favorable terms in order to park this capital in US Treasuries or stocks, among other things, with higher yields. And since we are not talking about a few billions, but trillions of US dollars, it is hardly surprising that US market yields and the Japanese yen have a very close relationship.

(Click on image to enlarge)

These yen carry trades led to market yields being depressed by massive purchases of US bonds, while US equities benefited from abundant cheap liquidity.

But the days of cheap yen are over. The trades are no longer being extended, which should logically have the opposite effect: rising US yields and selling pressure on US stocks. We saw the first taste of this yesterday, and not just on Wall Street. Sentiment has been fairly neutral recently – in other words, ripe for being pushed in either direction.

(Click on image to enlarge)

The media now believes that US President Donald Trump’s desire to annex Greenland is responsible for the sell-off in stocks and bonds. Let’s take a closer look, because the Greenland story is not as simple as it is portrayed in the media:

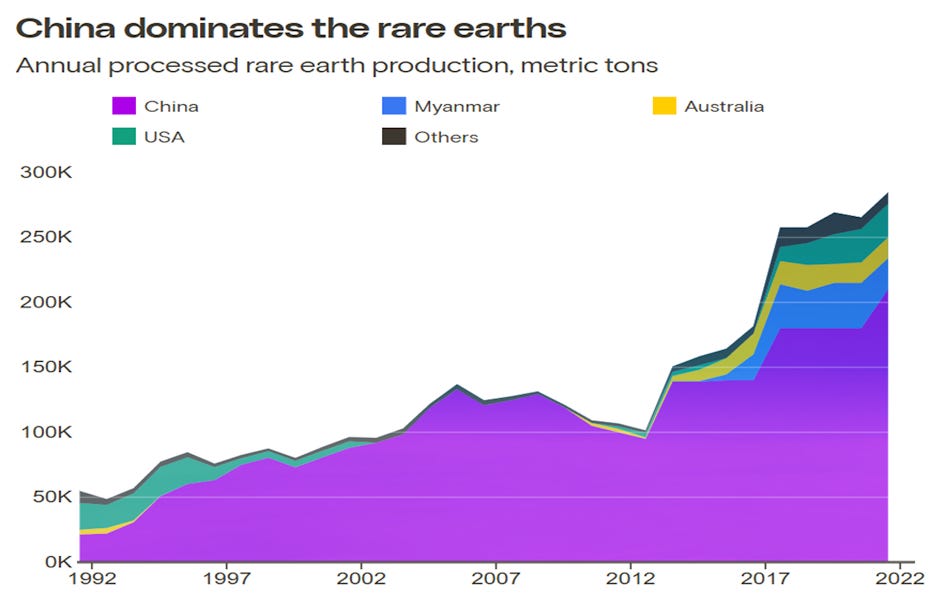

Geologists suspect that Greenland has significant deposits of rare earths. These are indispensable for modern electronics – and around 90% of them are currently refined in China.

(Click on image to enlarge)

As we have mentioned several times before, we are on the threshold of a new era in which artificial intelligence and the computing power of quantum computers will converge.

This is precisely why the big high-tech companies are investing so aggressively – they know exactly what lies ahead. Data centers are only the first step. The combination of AI and quantum computing will change our world so dramatically over the next five years that the winner of this race will effectively gain global power. It is therefore less a race between companies and more a race between governments. That is why the investment sums involved are almost irrelevant.

If the US is denied access to the necessary metals, it risks losing this race. This cannot be allowed to happen, because nothing can be expected from Europe, and the only alternative would be for China to set the economic and political pace for decades to come.

Not every investor may be aware of this, but the market seems to have understood it very well – just look at the movements of individual (sub-)sectors in recent months and years. The market apparently assumes that the US government will ultimately be satisfied with an increased military presence and mining rights in Greenland. In principle, the US has already controlled the large island since its invasion in 1940.

(Click on image to enlarge)

Has the pulse of the financial markets now increased because of Greenland or because of new threatened import tariffs? In recent years, Europe has largely withdrawn from world politics. The national debt of many countries has exploded, economic flexibility has shrunk, while socialist regulations have increased significantly. Added to this is political disagreement. After Japan, Europe is therefore also one of the regions with an increased risk of turmoil in the bond markets. And import tariffs? These are no longer a real specter for the market. More on this later...

We recognize that cheap capital from Japan is drying up – and that sooner or later, capital from Europe will also be looking for a new home. Realistically, the US dollar is really the only option. The much-cited Armageddon scenario of a dying US dollar should therefore be treated with caution. Perhaps it is simply the last fiat currency to be laid to rest.

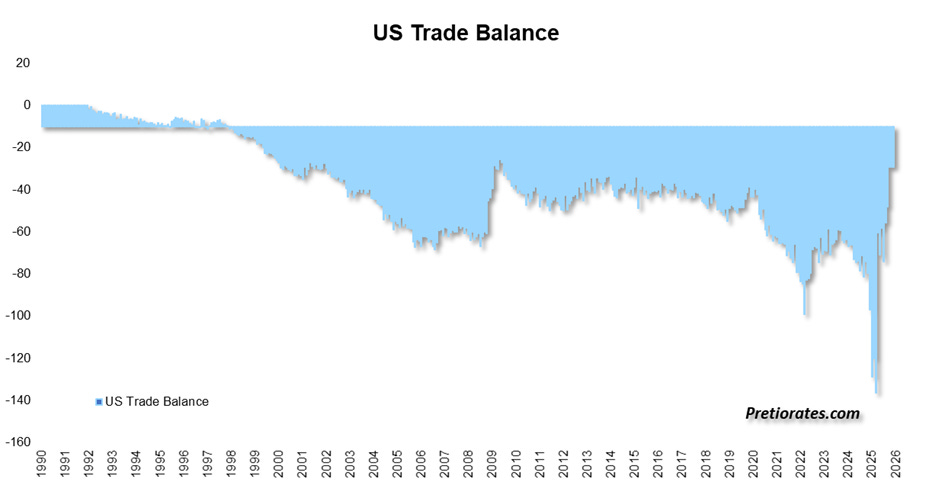

Also interesting is the assessment of a large independent research firm, which classifies Trump’s Greenland initiative as a mere distraction. In the coming days and weeks, the US Supreme Court (SCOTUS) is expected to rule on import tariffs. Analysts believe that the ruling could potentially go against the US government. However, tariffs have not only become a political and economic weapon for the president, but also a pillar of support for the US stock market. After initial nervousness, they have even calmed the US bond market. They reduce the trade deficit – a welcome calming pill in terms of debt.

(Click on image to enlarge)

If the Supreme Court does indeed rule against import tariffs, it would not only be a political slap in the face for the president, but would also likely cause headaches for the US stock and bond markets. The reputation of US government bonds as a safe haven would suffer further – a circumstance from which gold is likely to benefit once again.

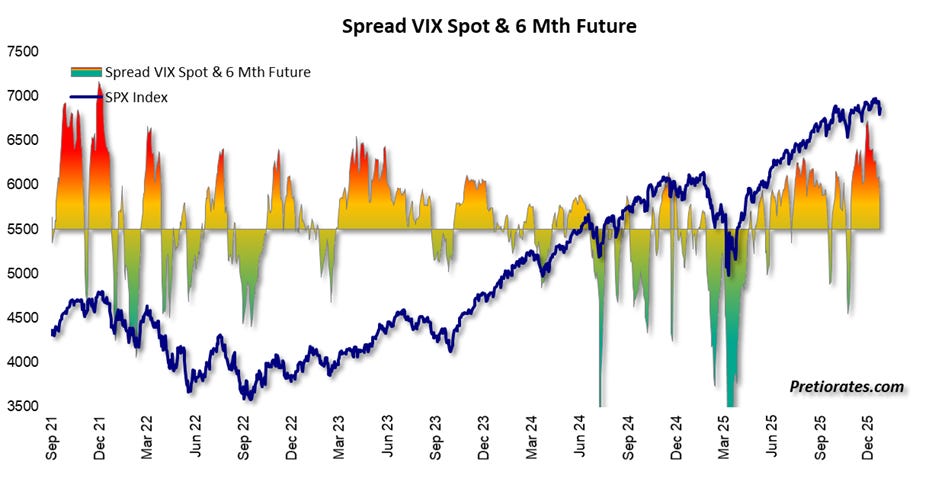

In the end, it is almost secondary whether the Japanese bond market, Greenland, or SCOTUS with its tariff decision is responsible for the increased nervousness. The market itself is already clearly signaling that it is no longer entirely satisfied. Whenever the volatility future is trading significantly above the spot price for six months, trouble is brewing. This situation arises when large investors use futures to hedge against rising volatility – i.e., nervousness.

(Click on image to enlarge)

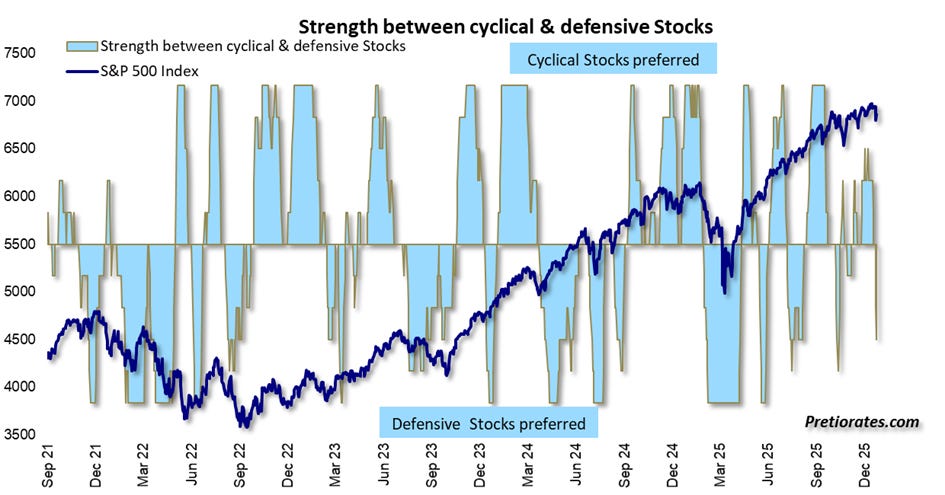

We have also observed that US investors have recently been increasingly betting on defensive stocks. This is another clear indication that the very strong bullish sentiment is currently weakening.

(Click on image to enlarge)

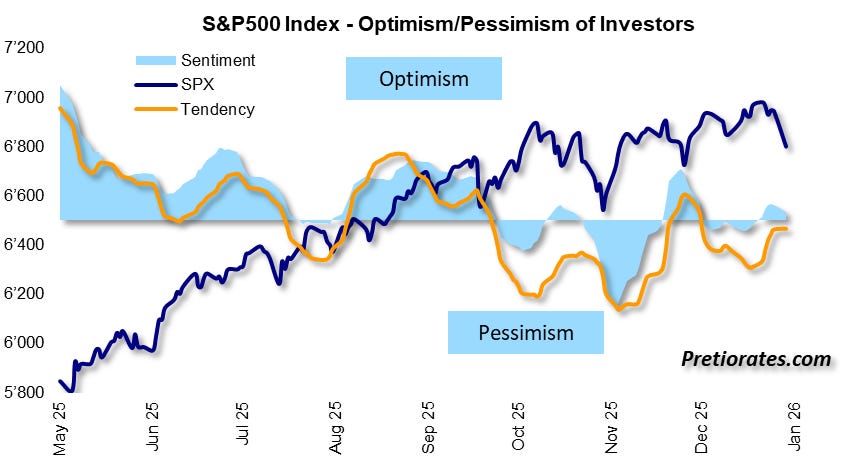

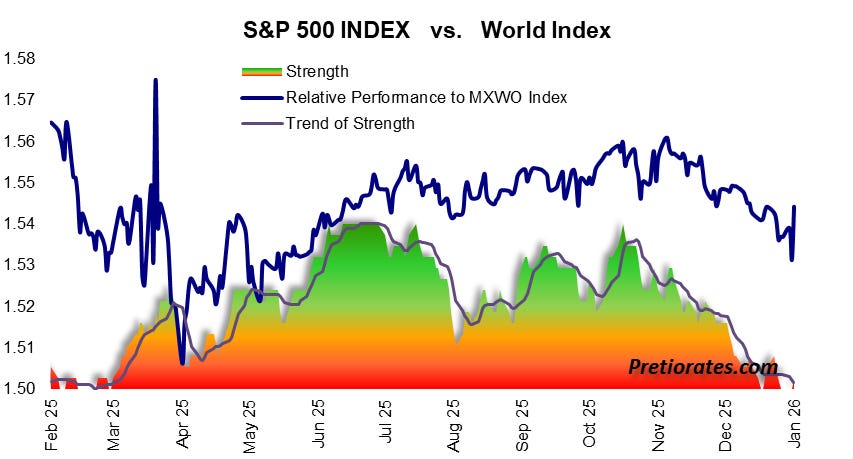

Many investors still have the impression that the US stock market has performed excellently in recent months. In reality, however, it has been weakening since November. In relative terms, the S&P 500 has not been able to keep pace with the global world index for three months. We would therefore not be surprised if the bears slowly emerge from hibernation in the coming days and weeks.

(Click on image to enlarge)

More By This Author:

Silver, Spreads, And Beads Of SweatWelcome To 2026, Expect The Unexpected

Silver Delta Hedge

Comments

Log in or sign up to join the conversation.