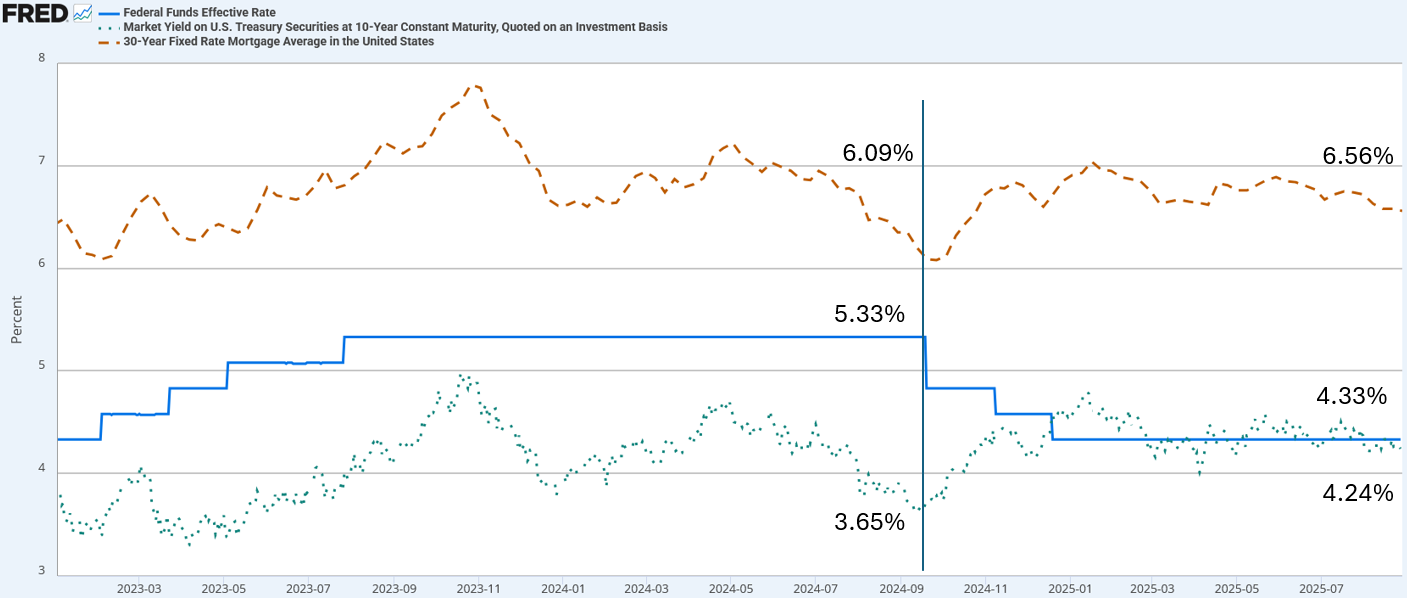

The Fed has cut the Fed Funds rate by 1% since late 2024, and the presumption from many market participants is that the Fed has made policy less restrictive. Technically, they are somewhat correct. Banks and other financial institutions that borrow over very short periods have seen their borrowing costs decline due to the Fed’s actions. However, the Fed has indirectly made policy more restrictive for the vast majority of borrowers.

The graph below shows that despite the overnight Fed Funds rate falling from 5.33% to 4.33%, mortgage rates and the yield on the ten-year US Treasury have risen about half a percent. Bear in mind that corporate and auto loans, as well as almost all other bank lending rates, are tied to the 10-year Treasury yield. Thus, these rates, too, have become more restrictive. Although not shown, the 5-year Treasury yield, which serves as a benchmark for shorter-term loans, is approximately 30 basis points higher than it was before the Fed began cutting rates.

Since the Fed cut rates, the economy and payroll growth have slowed appreciably. Inflation remains above the Fed’s 2% target but is near the same levels as when they started cutting rates. The critical takeaway is that, despite weaker economic growth and a pronounced slowing in the labor market, interest rates have become more restrictive. Instead of assuming that monetary policy is easier today than in 2024, the Fed and investors should consider that policy is actually more stringent for the vast majority of borrowers.

What To Watch Today

Earnings

(Click on image to enlarge)

Economy

(Click on image to enlarge)

Market Trading Update

Yesterday, we discussed that the market remains bullish as the 20-DMA support remains intact. One area of the market we haven’t touched on lately is bonds. The iShares 20-Year Treasury Bond ETF (TLT) has been basing for quite some time. Notably, there is a considerable volume at current levels where buyers and sellers are evenly matched. One thing to watch is the price compression that is currently occurring. If TLT breaks above this consolidation range, we could see a sharp move higher. While many argue that “interest rates must go higher,” the reality is likely the opposite. With economic growth slowing and inflation falling, we are likely to see rates lower in the future. That is also what the current price compression is telling us as well.

(Click on image to enlarge)

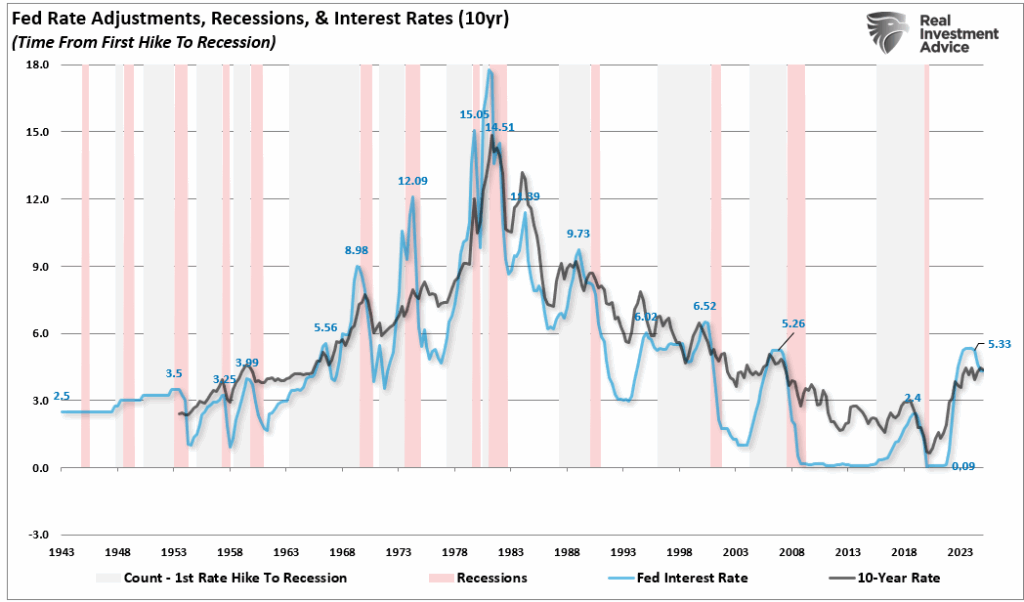

Furthermore, the potential for a rate decline increases when considering that the Federal Reserve is about to start lowering rates again. Historically, whenever the Fed has hiked rates, the eventual outcome was a recession. While that outcome was not immediate, it eventually occurred. That recessionary pressure caused long-term rates to fall. As noted, with employment weakening and economic data slowing, the risk of a recession from current growth levels is not a far-fetched idea.

Bonds have been dead money for investors from a capital appreciation perspective. However, bonds in a portfolio have continued to provide a hedge against market volatility and a decent income stream to supplement portfolio returns while protecting capital. The current technical setup is improving and looks like it will provide a better appreciation opportunity in the future for those who can be patient and wait.

Corporate Bond Spreads – The Latest From SimpleVisor

We just added corporate bond spread analysis to SimpleVisor. The screenshot below allows us to walk through what the new page tells us. For starters, all the data on the page represents the difference in yield between the various credit ratings of the BofA Corporate Bond Index and a similar-maturity US Treasury security. We highlight in red the data for BBB-rated bonds. On the top left, we can see that currently, BBB bonds yield 1.03% more than US Treasuries. The table to the right of that spread informs us the spread is historically tight. For example, over the last 20 years, the spread has only been lower than it is today 0.99% of the time. The graph to the right shows this as well.

The bottom two tables help us appreciate spreads between different-rated corporate bonds and how they have changed over the prior four weeks. Currently, BBB bonds yield 0.70% more than AAA-rated bonds. That spread is unchanged over the last four weeks.

Similar to sentiment in the stock market, this table indicates that sentiment in the corporate bond market is extremely bullish. As a result, spreads are well below average, leaving corporate bondholders, especially those in lower-rated bonds, vulnerable to a significant loss if spreads revert to their historical averages.

(Click on image to enlarge)

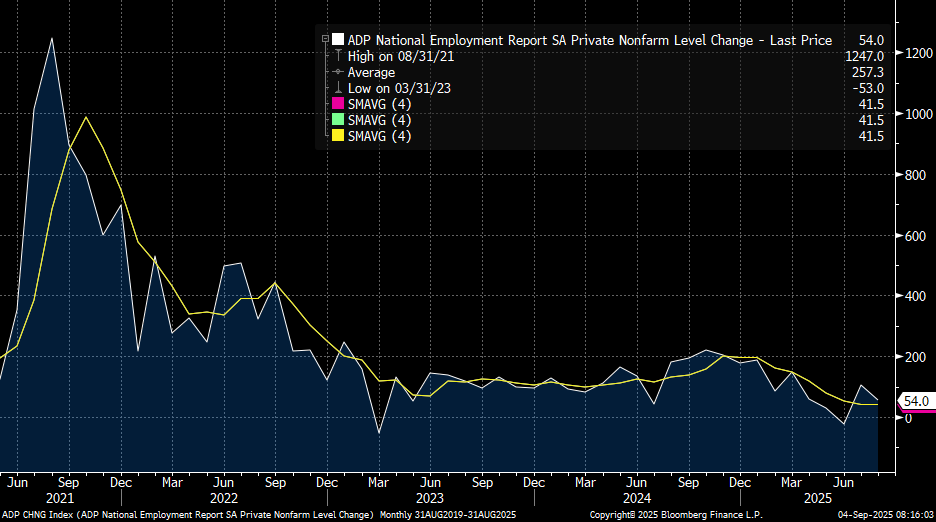

ADP Is Worse Than It Seems

ADP has proven to be a prescient indicator of the labor market. Over the past six months, ADP has shown a pronounced slowing of job growth. Until the BLS significantly revised its job growth figures lower last month, the BLS was pointing to a healthy jobs market. With the revisions, ADP and the BLS are back in sync. As we gear up for today’s BLS labor report, we should consider that yesterday, ADP reported the jobs grew by 54k. Such is below the 150k-250k run rate of the prior few years. More importantly, and often overlooked, the labor force grows by approximately 150k people per month on average. Thus, the recent average growth rate of 50k by the ADP and the BLS indicates that job growth is not keeping pace with the growth of the labor force.

The second graph below helps partially explain why the unemployment rate has remained stable despite job growth that is below the rate of labor force growth. The graph, courtesy of Trading Economics, shows that the participation rate has fallen by 0.4% over the last four months. This tells us that 0.4% of the population has left the workforce. Some people exit for legitimate reasons, such as retirement. Yet, others can’t find a job and stop looking. The point is that the unemployment rate is likely higher than the BLS claims would be if not for the declining participation rate. We may learn this in months and years from now as the BLS revises its data.

Tweet of the Day

More By This Author:

Why Keynes’ Economic Theories Failed In Reality

Robots Are Tesla’s Future: EVs No Longer The Value Proposition

Monthly Market Trends: Do They Matter?

Comments

Log in or sign up to join the conversation.